Buy Godrej Properties Ltd for Target Rs. 2,096 by Geojit Investments Ltd

Strong pipeline supports growth

Godrej Properties Ltd (GPL), a subsidiary of Godrej Industries Ltd, is a real estate company, with total saleable area of 238mn sq ft across India.

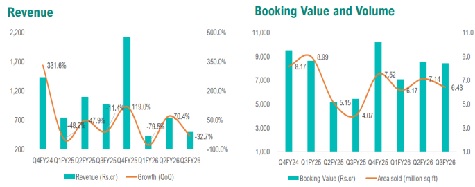

* In Q3FY26, booking value increased 54.6% YoY, supported by 3,973 home sales covering 6.43mn sq ft, marking a 57.9% YoY rise in volumes.

* Customer collections rose 39.5% YoY to Rs. 4,282cr and delivered projects aggregated ~1.7mn sq ft in three cities during the quarter. • Also, three new projects were added to the portfolio, covering ~7.3mn sq ft of saleable area and a potential booking value of ~Rs. 8,400cr.

* The Mumbai's Metropolitan Region accounted for Rs. 3,239cr of the booking value, supported primarily by the launch of Godrej Trilogy at Worli, which contributed Rs. 1,742cr to the booking value.

* EBITDA was negative Rs. 197cr on account of increases in material cost (+39.8% YoY), employee expense (+13.9%) and other expense (+13.4%).

* Reported profit after tax rose 22.5% YoY to Rs. 194cr, driven by a 97.5% YoY increase in other income

Outlook & Valuation

Godrej Properties’ 9MFY26 performance was weak due to higher construction spending and timing of deliveries, but the company is set for a strong Q4 with multiple launches and a large batch of OCs. Additionally, a robust launch pipeline and steady pace of deliveries are driving growth, whereas focus on high-demand micro-markets ensures steady sales velocity. Looking ahead, the company is consolidating its joint ventures positioning GPL for stronger growth, contributing to revenue, EBITDA and net profit. Coupled with resilient demand across core markets and a robust multicity project pipeline, the medium-term outlook remains healthy despite near-term volatility in recognition. Hence, we upgrade our rating on the stock to BUY, with a rolled forward target price of Rs. 2,096, based on 2.1x FY28E book value per share

Key Concall highlights

* GPL achieved its best-ever performance in calendar year 2025 in the latest quarter. The company's notable milestones included a 19% YoY rise in bookings to Rs. 34,171cr, 28% YoY increase in collections to Rs. 18,979cr, 20% YoY increase in operating cash flow to Rs. 7,246cr, and 20% YoY growth in earnings to Rs. 1,582cr. The growth rates were achieved despite a high base in the corresponding period of calendar year 2024.

* The company also added 12 new projects with an estimated saleable area of 22.36mn sq ft and estimated booking value of nearly Rs. 24,650cr in the first nine months.

* The company is also highly confident of meeting and potentially exceeding its FY26 presales guidance, with 9MFY26 at ~74% of the annual target; it sees strong visibility for presales growth into FY27.

* Several new launches are planned, including in the Sigma sector of Greater Noida and a residential cluster in Godrej Golf Links, Greater Noida.

* Inventory rose by Rs. 19,000cr in the 9-month period, with construction cash flow of Rs. 5,000cr and land acquisition of Rs. 5,400cr.

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034