Buy Godrej Agrovet Ltd for the Target Rs.690 by Motilal Oswal Financial Services Ltd

Near-term weakness with recovery underway

Operating performance misses due to weaker-than-expected gross margins

* Godrej Agrovet Limited (GOAGRO) reported a subdued operating performance in 4QFY26, with EBIT declining 10% YoY. The weakness was primarily driven by a sharp contraction in the Crop Protection standalone / Vegetable Oil/ Dairy segments, where EBIT declined by 42%/12%/ 76% YoY. This was partially offset by strong performance in the Animal Feed and Poultry segments, which delivered EBIT growth of ~2.0x and 3.1x YoY, respectively.

* While growth trajectory remains structurally robust, supported by its strategic pivot towards a higher share of value-added offerings across key business segments, the evolution of the animal feed business towards ‘animal nutrition’ and a strong pipeline of new product launches in crop protection. The short-term outlook remains uncertain due to the evolving impact of El Niño, continued elevated milk procurement prices, and excess inventory levels in the crop care segment.

* Hence, we cut our FY27 EBITDA estimates by 9%, while broadly maintaining our FY28 EBITDA estimates. We reiterate our BUY rating on the stock with an SOTP-based TP of INR690.

Operational performance impacted by input cost pressures

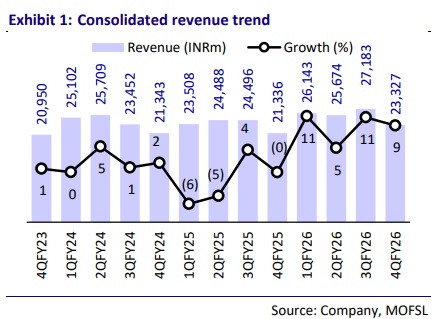

* Consolidated revenue stood at INR23.3b, up 9% YoY (est. in line). EBITDA margin contracted 90bp YoY to 6% (est. 7.2%), led by gross margins contraction by 240bp YoY to 23.4% and an increase in employee cost (stood at 6.2% vs 6.1% in 4QFY25). EBITDA stood at INR1.4b, down 5% YoY (est.INR1.7b). Adjusted PAT grew ~48% YoY to INR1b (est. of INR814m).

* AF: Revenue grew 11% YoY at INR12.7b, while margins expanded 460bp to 10.4%. Volumes grew ~15% YoY, which was partially offset by a 4% dip in realizations (product mix change).

* Palm Oil: Revenue declined 5% YoY to INR2.3b, driven by lower realizations in crude palm oil (CPO), which declined ~5% YoY. EBIT margin contracted 50pp YoY to 7%. EBIT declined ~12% YoY to INR162m.

* CP: Consolidated CP revenue grew 16% YoY to ~INR3.1b, with standalone CP revenue/Astec growing 10%/35% YoY. Astec’s revenue grew on account of robust volume growth in both the enterprise and CDMO categories. Consolidated CP EBIT declined 42% YoY to INR265m, with standalone CP EBIT declining 50% YoY to INR270m.

* The Dairy business revenue grew 4% YoY to ~INR4b, while EBIT declined ~76% YoY to INR16m, driven by elevated procurement costs. The Poultry and Processed Food business’srevenue stood at INR1.8b (+2.5% YoY), while EBIT wasINR126m (up 3.1x YoY) and EBIT margin stood at ~6.8% in 4QFY26, compared to 2.3% YoY to 4QFY25.

* For FY26, GOAGRO’s revenue/EBITDA/adj. PAT grew 9%/6%/15% to INR102.3b/INR8.6b/INR5b.

* CFO stood at INR1.3b, as against INR969m in Mar’25. Further, gross debt stood at INR15.7b, as against INR13.7b in Mar’25

Highlights from the management commentary

* Guidance/Outlook: Management has guided for an early double-digit revenue growth and mid-teens PBT growth, underpinned by: i) sustained double-digit growth in animal nutrition, ii) a recovery in crop care from 2QFY27, driven by channel inventory normalization, iii) continued momentum in the oil palm business, and iv) moderation in milk procurement prices from 2QFY27 expected to support dairy margins.

* Astec: The business has reached a pivotal stage, achieving EBITDA break-even in FY26, with a sharp reduction in losses. It is positioned for sustained growth, driven by improved volumes, realizations, and capacity utilisation across both Enterprise and CDMO segments; management guides for 15-20% topline growth, with stable-to-improving margins going forward.

* Crop protection: The crop protection business is undergoing a strategic diversification from its earlier concentration in cotton herbicides and chillifocused products towards a multi-crop portfolio, with FY27 marking the scale-up of new products-Ashitaka (maize herbicide) and Takai (rice-led insecticide), with contribution expected to increase from ~3% in FY26 to ~16-18%.

Valuation and view

* GOAGRO’s outlook remains constructive, supported by strategic portfolio realignment initiatives, including: i) exit from live-bird trading, ii) targeted geographic expansion in animal nutrition, iii) increased focus on R&D, iv) the transition of the animal feed business towards an ‘animal nutrition’ model, v) diversification of the crop protection portfolio, and vi) allocation of ~75–80% of planned capex towards growth initiatives.

* Further, improvement in volumes, realizations, and capacity utilization across both Enterprise and CDMO in Astec positions the business for sustained recovery and profitable growth in the coming years.

* We have built in Revenue/EBITDA/Adj. PAT CAGR of 6%/12%/12% over the FY26-FY28E. We reiterate our BUY rating on the stock with an SOTP-based TP of INR690.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412