Buy Container Corporation Ltd for the Target Rs 560 by Motilal Oswal Financial Services Ltd

Weak 4Q; realizations and margins remain under pressure

* Container Corporation (CCRI)’s revenue dipped 1% YoY to INR22.5b in 4QFY26 (6% below our estimate). Total volumes grew 6% YoY to 1.4m TEUs, with EXIM/Domestic volumes at 0.107m/0.36m TEUs (+2%/+19% YoY). Blended realization declined ~7% YoY to INR15,803/TEU. EXIM/Domestic realization stood at INR14,015/INR21,112 per TEU (-2%/-19% YoY).

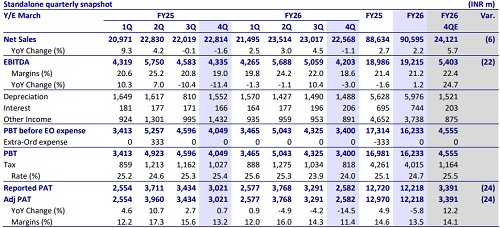

* EBITDA margin came in at 18.6% (vs. our estimate of 22.4%). EBITDA dipped 3% YoY to INR4.2b and was 22% below our estimate. In line with the weak operating performance, APAT declined 15% YoY to INR2.5b (24% below our estimate). Land license fee for FY26 stood at INR3.95b. The Board declared a dividend of INR1 per equity share amounting to INR761m.

* In FY26, CCRI’s revenue/EBITDA grew ~2%/1%, while APAT dipped 6% YoY.

* CCRI posted a weak set of performance in 4QFY26, as the West Asia crisis hit volumes, which ultimately weighed on margins. In addition, realizations across both the EXIM and domestic segments remained under pressure due to lower lead distance. Growth was further affected by heightened competitive intensity, where the company continues to avoid low-margin business, impacting market share.

* We cut our EBITDA estimates for FY27 and FY28 by 5-7%, factoring in lower volume growth, weaker realization in EXIM/domestic business amid heightened competition intensity, and continued margin pressure. We remain watchful of how DFC connectivity translates to incremental volume growth for CCRI. We expect its revenue/EBITDA to clock a CAGR of 9%/12% over FY26-FY28. We reiterate our BUY rating on the stock with a revised TP of INR560 (based on 14x EV/EBITDA on FY28E).

Key highlights from the management commentary

* The company faced operational disruptions due to ongoing geopolitical tensions, which impacted volumes during 4QFY26 as well as in Apr’26. However, management remains optimistic about a recovery in volumes from May’26 onward, supported by improving demand conditions and normalization in trade activity.

* For FY27, CCRI has guided for 9.5% growth in total volume, with 8%/15% growth in EXIM/domestic volumes.

* The domestic margin was hit during the quarter due to higher empty running, lower lead distance, and loss of tile volumes due to the closure of the tile factory in Morbi.

* Management expects the commissioning of the DFC by Jun’26 to notably improve rail-linked volumes at JNPT. The rail coefficient at JNPT, currently at ~15%, is likely to increase to 18–19% in FY27 and further rise to ~30% over the next three years, which is likely to drive strong growth in rail volumes.

* The originating volume for EXIM/Domestic stood at 0.55m/0.13m TEUs.

Valuation and view

* CCRI posted a weak set of performance in 4QFY26, as the West Asia crisis hit volumes, which ultimately weighed on margins. In addition, realizations across both the EXIM and domestic segments remained under pressure due to lower lead distance. Growth was further affected by heightened competitive intensity, where the company continues to avoid low-margin business, impacting market share.

* We cut our EBITDA estimates for FY27 and FY28 by 5-7%, factoring in lower volume growth, weaker realization in EXIM/domestic business amid heightened competition intensity, and continued margin pressure. We expect its revenue/EBITDA to clock a CAGR of 9%/12% over FY26-FY28. We reiterate our BUY rating on the stock with a revised TP of INR560 (based on 14x EV/EBITDA on FY28E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412