Buy Century Plyboards Ltd for the Target Rs 907 by Motilal Oswal Financial Services Ltd

Channel stocking drives strong volume growth 4QFY26 – a healthy in-line performance

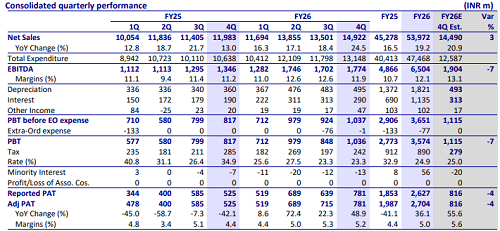

* Revenue/EBITDA/adj. PAT grew 25%/32%/49% YoY (broadly in line).

* Strong revenue growth was driven by all key segments.

* EBITDA margin improved 66bp YoY to 11.9%. Strong plywood margins partly offset weaker margins in other segments.

* Capacity utilization of plywood and MDF plants was near optimal levels.

* Gross debt stood at INR15.3b, with debt-to-equity ratio at 0.62x in FY26.

* Capacity utilization stood at 99% for Plywood and 85% for MDF segment.

Plywood and MDF to undergo large capex program

* Capex in FY27 is budgeted at INR4.14b. Capex over the next two years will be mainly in Plywood and MDF segments at Hoshiarpur (Punjab).

* Major capex programs beyond FY28 are not frozen yet.

* Greenfield expansion of MDF/Laminates/PVC board facility in Andhra Pradesh to entail investments of INR260m/INR419m/INR606m in FY27.

* It will spend INR865m on expansion at plywood plant in Punjab. Additional INR2b is earmarked for other expansions.

* Land is acquired in Uttar Pradesh for manufacturing plywood, and MDF is still in process.

* The plans to set up a facility in Odisha for Plywood and Particle Board are still in early stages and will start after two years.

Valuation and view

* After a broadly in-line 4Q result, we cut our earnings estimates by 2-5% owing to lower margins assumptions.

* We now expect CPBI to clock a 16%/30%/53% CAGR in revenue/EBITDA/ APAT over FY26-28. RoE/RoCE (17.4%/16.9% in FY28) will remain muted for the next few years due to the ongoing heavy capex programs.

* Given CPBI’s leadership position in its key building product segments and high earnings growth expectations, we reiterate our BUY rating on CPBI with a TP of INR907, based on 32x FY28E P/E (similar to its 1-year forward 10-year average multiple).

* Please refer our sector initiation report for our detailed view on CPBI.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412