Buy CEAT Ltd for the Target Rs 4,228 by Motilal Oswal Financial Services Ltd

Margins to remain under pressure in the near term

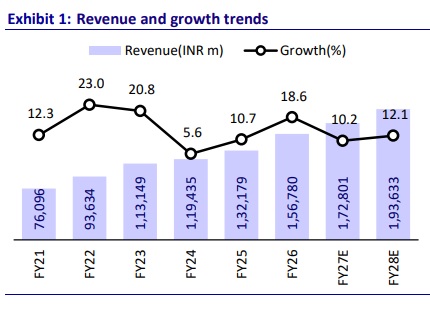

Camso integration roadmap disclosed We met with the CEAT management at the annual RPG Conference on 26th May’26. The company outlined a roadmap for Camso integration, highlighting key growth drivers and the potential for the business to achieve 20-25% EBITDA margin over the coming years. In India, while demand across segments remains healthy currently, it is likely to moderate in the near term following sharp price hikes expected to offset rising input costs. Further, replacement demand for TBR is expected to grow in single digits, PCR at 3-5%, and scooters in high single digits in FY27. Raw material prices are expected to witness a sharp 15-20% QoQ increase in 1Q. While CEAT has already taken a 5% price hike, under-recovery remains at 5%, which is expected to keep near-term margins under pressure. We expect CEAT to clock a CAGR of ~11%/12%/13% in revenue/EBITDA/PAT over FY26-28. Overall, long-term integration benefits disclosed from Camso are likely to offset near-term concerns on margin pressure. We reiterate our BUY rating on the stock with a TP of INR4,228 (based on ~18x FY28E EPS). Following are the key takeaways from our interaction:

Camso to be a USD1b opportunity post brand migration in 1HFY28

* Camso represents an overall ~USD1b business, currently split between CEAT and Michelin. CEAT has acquired the ~USD150m compact construction tracks business through its Sri Lanka operations, which will continue to operate under the Camso brand, while Michelin will retain the remaining ~USD850m business under the Michelin brand. The transaction effectively opens up ~USD850m addressable market opportunity for CEAT, where it will directly compete with Michelin.

* The first phase of the acquisition has been completed, with integration activities currently underway. The next phase, extending through 2HFY27, will focus on complete value chain integration (mixer calendar installation will result in a 100% manufacturing control). The Camso brand’s transition to CEAT is expected to be completed by 1HFY28, followed by the scale-up of operations in 2HFY28. Management plans to double capacity by FY28, with margin accretion from the OHT business expected from FY28-FY29 onwards. Management has guided that, once operations at Camso stabilize post 2028, margins are expected to be in the 20-25% range.

* Beyond the immediate market opportunity from Michelin, management highlighted multiple incremental growth avenues from FY28 onwards to achieve the USD1b target, including:

* Scaling the OTR business (which currently stands at ~USD250-260m in revenue) to USD500m,

* ~USD100m opportunity in agricultural tracks,

* ~USD50–100m opportunity across solids, material handling, and export segments, and

* USD150m opportunity from the Camso radial portfolio.

* Management indicated that Michelin currently has no meaningful presence in the agricultural tracks business, positioning Camso favorably to capitalize on this opportunity and gain market share. This aligns with management’s vision of regaining market share to ~40% over the next 4-5 years in the compact construction tracks segment. Camso’s market share has declined to ~20% from earlier levels of ~45%.

* Camso will remain a predominantly international business, with a strategic focus on the US and Europe markets, and selective exposure to Latin America. Domestic market participation is expected to remain limited.

* Camso generated revenue of ~USD125m in CY25. However, under the Michelin ownership, aggressive price increases that were not matched by competitors led to volume declines. Additionally, Michelin had curtailed new OEM programs due to its intention to divest the business, resulting in a lower share of business. Management believes revenues from Camso’s Sri Lanka operations alone could scale up to ~USD275-300m if utilization levels increase to ~95-100%.

* The company is currently engaging with two OEMs for agricultural radial tyres, although no order wins have been secured so far.

* Management clarified that it does not intend to pursue a dual-brand strategy, wherein CEAT would fill the gaps vacated by Camso. Instead, the company plans to carefully evaluate cross-selling opportunities while avoiding any potential brand dilution.

* Camso's operations saw some temporary production disruptions in 4QFY26 due to fuel shortages in Sri Lanka.

* On US tariffs, management highlighted that tyres are subject to a 10% tariff, metals to 25%, and tracks to 50%. The benefit of lower tariffs translating into higher demand is not yet visible, as the company is not directly handling customers at this stage. Complete customer transition from Michelin is expected to conclude by Oct’26.

Commodity headwinds to result in margin pressure in the near term

* Key input costs have risen sharply recently: Crude price has increased from around USD65 at the start of the quarter to nearly USD100 by early March; international natural rubber increased from around USD1,700/ton in 3Q to USD1,800/ton in 4Q and is currently at USD2,050–2,100/ton. Further, domestic natural rubber prices increased from around INR190/kg at the beginning of 4Q to nearly INR245/kg currently. The company is also likely to be impacted by INR depreciation.

* Raw material prices remained stable QoQ in 4Q but are expected to increase by around 15-20% QoQ in 1Q. Management indicated that a 10% price increase in the replacement market would be required to pass on this impact. So far, the company has implemented a 5% price hike by the end of April and may require an additional 5% increase. However, subsequent price hikes would depend on competitive dynamics.

* The company has already implemented a low single-digit price hike in the OE segment, while a further hike due to indexation is scheduled to take effect from July’26. Overall, management expects cumulative price increases of ~10-12%, which could weigh on demand during 2QFY27. However, raw material inflation is expected to normalize by 2Q.

* Industry-wide price increases appear to be underway, with most players having implemented hikes during March and April, although some may have delayed the rollout in select segments. Despite competitors undertaking price hikes, the company did not observe any significant change in market share dynamics.

* The benefit of low-cost inventory supported margins in 4Q, while the impact of rising input costs is expected to be reflected in 1QFY27. Management expects margins in 1QFY27 and 2QFY27 to remain under pressure. The company has deferred certain costs into subsequent quarters to provide near-term relief and has also initiated a zero-based costing exercise to improve operational efficiencies and lower costs.

* International business continues to remain a key strategic focus, with management targeting one-third of consolidated turnover from overseas markets versus ~19% currently. The company is implementing price hikes in stages, cumulatively amounting to around 10%. However, as orders have already been booked for the next 30 days at lower prices, the full benefit of these hikes is expected to flow through with a lag of around 30-45 days. The US has levied a 44% tariff on imports from Sri Lanka. However, negotiations are ongoing, and CEAT does not expect a 44% tariff.

Domestic demand likely to moderate in the near term due to price hikes

* The current demand continues to be healthy, largely across all segments. However, given the sharp input cost inflation that is likely to be passed on soon and given the ongoing West Asia conflict, demand is likely to moderate in the coming months, especially for the CV segment.

* Replacement demand for TBR in FY27 is expected to grow in the single digit, driven by economic activity, positive seasonality, and an aging fleet. The pace of growth is expected to moderate due to the expected price hikes, but the management is confident that it will not decline. PCR growth is expected to increase from the usual 1-2% to 3-5%. Even the scooters segment is expected to witness high single-digit growth in FY27.

* In the OE segment, the MHCV segment continues to experience strong doubledigit growth, and PV is expected to witness healthy single-digit growth coming largely from the SUV and MPV segments. LCV growth is also expected to remain strong.

* In the international business, the company expects demand recovery in multiple segments, especially in the MHCV in the US and the EU. PV demand in the EU is also recovering for CEAT. The Middle East accounts for 15% of CEAT’s exports and is impacted due to the ongoing tensions. Exports to the Middle East completely dried up in 4QFY26.

Updates on capacity expansion

* Total capex for FY26 was INR10.8b, and the company plans to spend INR2–2.5b in mandatory capex in Q1FY27, with a total capex requirement of INR13–14b for FY27 in the India business. Further, the company would look to spend USD30m in Camso for upstream capacity, 75% of which would be incurred in FY27.

* Gross debt increased QoQ by INR800m to INR30b. The company would look to maintain these debt levels in 1Q on account of margin pressure, while it might

increase in later quarters in order to fund the growth capex outlined for FY27 once the RM environment normalizes.

* Return ratios are expected to improve over the coming years, supported by faster utilization ramp-up of recent capex investments. Current utilization levels across manufacturing locations are averaging ~90%, with management remaining confident on ROCE expansion.

Valuation and view

* Focus on improving brand equity helps drive market share gains: CEAT has placed a strong emphasis on effective marketing and branding (~2.0-2.5% of sales) for its products. To position its products competitively, it has developed creative advertising campaigns based on research and consumer insights and has invested in innovative marketing programs. Since the 2W and Passenger Car segments are consumer-facing, factors such as brand loyalty, visibility, and recall play a significant role in creating replacement demand and improving market share. This has helped the company establish a strong brand across segments. For instance, it is now the market leader in the 2W segment with ~31% share. In PVs, it is now the third-largest player with ~17% share. Further, with a gradual ramp-up in the TBR segment, it is now hitting ~10% market share in this segment.

* GST 2.0 has been a boon for the industry: Auto demand has seen a marked revival across segments post GST 2.0. For the tyre industry, this has led to a pickup in both replacement and OE demand, as well as across all key segments.

* Sharp rise in input costs to drive near-term margin pressure: The cost of key raw materials, including crude and rubber, has spiked in recent months, with the raw material basket expected to rise almost 15-20% on a QoQ basis in 1QFY27. While CEAT has taken a 5% price hike in recent months, it intends to take a similar hike in the next couple of months to pass on the entire impact. This sharp surge in input costs is likely to hurt margins in the near term. Overall, we expect CEAT to clock a revenue/EBITDA/PAT CAGR of ~11%/12%/13% over FY26-28, with growth expected to be largely back-ended.

* Valuation and view: The GST rate cut has supported growth in the tyre demand, both in replacement and OEM segments. However, the recent surge in input costs is likely to exert near-term margin pressure, as the industry may require a couple of quarters to pass on the entire impact. Further, while the recent Camso acquisition is expected to take time to normalize, we remain positive on the long-term benefits that this acquisition can deliver for the group. Hence, we reiterate our BUY rating on the stock with a TP of INR4,228 (based on ~18x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412