Buy Campus Activewear Ltd for the Target Rs 325 by Motilal Oswal Financial Services Ltd

Robust 4Q; price hikes to cushion margins against RM inflation

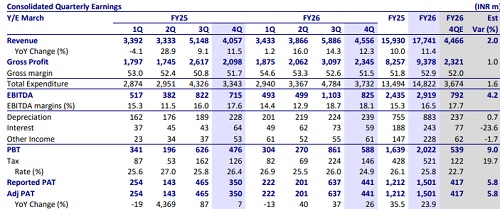

* Campus Activewear (CAMPUS) ended FY26 on a robust note, with ~12%/15% YoY revenue/EBITDA growth, led by ~10% YoY volume growth and ~50bp EBITDA margin expansion in 4Q.

* For FY26, CAMPUS delivered ~11% YoY revenue growth, with ~115bp YoY EBITDA margin expansion, resulting in ~20% reported EBITDA growth.

* The growth was driven by strong performance in D2C channels, aided by strong traction in the sneakers portfolio, which also led to margin expansion.

* The company has implemented calibrated price hikes across the portfolio, which should cushion the impact from RM inflation in the near term and drive margin expansion over the medium term (as RM prices ease).

* CAMPUS continues to strengthen its positioning through faster product launches, expansion of in-house sneaker capacities, and improved marketplace execution, supporting market share gains amid rising competitive intensity.

* We fine-tune our FY27-28 estimates and now model ~13%/18%/21% FY26- 28E CAGR in revenue/reported EBITDA/PAT, with EBITDA margin expanding 155bp to ~18% by FY28.

* Reiterate BUY rating with a revised TP of INR325, based on 45x FY28E EPS.

Robust growth and reported margin expansion in FY26

* Revenue grew ~11% YoY to INR17.7b, driven by 4% YoY growth in volume, while ASP rose ~7% YoY to INR683.

* D2C offline led with ~17% YoY growth, followed by 11% YoY growth in D2C online (despite accounting change) and ~10% YoY in trade distribution.

* Gross profit grew ~14% YoY to INR9.4b, aided by ~105bp gross margin expansion to 52.9%.

* Reported EBITDA rose 20% YoY to INR2.9b, led by ~115bp margin expansion.

Valuation and view

* CAMPUS is expanding beyond its core category of sports shoes into sneakers, women’s, and kids’ categories. Sharper segmentation, affordability-led positioning, and ongoing operational initiatives are supporting stronger execution and an improving product mix. Channel feedback on execution remains stronger vs. peers.

* We fine-tune our estimates and build in revenue CAGR of 13% over FY26-28, driven by ~8% ASP growth and 5% volume growth. Improving product mix, price hikes, and recent launches are likely to support stronger ASP growth, while the focus remains on volume growth, as the company has linked distributors’ incentives to volume growth rather than value growth for FY27.

* We build in ~155bp EBITDA margin expansion over FY26-28E, with gross margin expansion contributing ~65bp, led by premiumization and mix improvements. The recent price hike is expected to cushion margins against near-term headwinds from raw material inflation. Accordingly, we model EBITDA/PAT CAGR of 18%/21% over FY26-28E.

* Reiterate BUY rating with a revised TP of INR325 (earlier INR305), based on 45x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412