Buy Billionbrains Garage Ventures Ltd for the Target Rs.235 by Motilal Oswal Financial Services Ltd

PAT jumps ~2x YoY, backed by strong broking activity

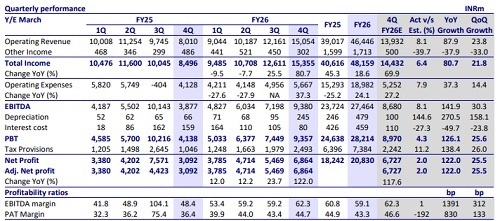

* Billionbrains Garage Ventures (GROWW) reported an operating revenue of INR15.1b in 4QFY26, up 88% YoY (8% beat). For FY26, the operating revenue grew 19% YoY to INR46.5b.

* Operating expenses were up 37% YoY in 4QFY26 to INR5.7b (8% higher than est.) with employee expenses up 44% YoY and other expenses up 16% YoY. However, strong revenue growth led to 142% YoY growth in EBITDA to INR9.4b, resulting in an EBITDA margin of 62.3% (vs. 48.4% in 4QFY25). For FY26, EBITDA margin stood at 59.1% (vs. 60.8% in FY25).

* PAT for the quarter came in at INR6.9b (in-line), growing 122% YoY (up 26% QoQ). For FY26, PAT was at ~INR20.8b, growing 14% YoY.

* Management expects operating costs to increase owing to 1) AI investments, 2) building new brands such as W, 915, Prime, etc., and 3) higher marketing intensity. However, margins are expected to maintain an expanding trajectory, considering 15%+ revenue growth.

* We have largely maintained our estimates considering revenue growth on the back of (1) continued growth in order run rate, (2) MTF book expansion, and (3) rising contribution of LAS to the credit segment, offset by rising operational costs. We reiterate our BUY rating with a revised TP of INR235 (premised on 35x FY28E EPS).

Growth reported across segments; derivative activity heightened

* Broking revenue rose 78% YoY to INR11.5b, driven by 64% YoY growth in orders to 587.4m as well as an increase in revenue per order to INR19.6 (INR18 in 4QFY25).

* Derivatives revenue grew 74% YoY/26% QoQ to ~INR8.5b, benefiting from high market volatility due to the ongoing geopolitical tension. GROWW’s retail option premium ADTO market share was 10.6%, up from 6.8% in 4QFY25.

* Cash revenue grew 52% YoY/8% QoQ to ~INR2.5b, with ADTO market share at 15.7% (12.1% in 4QFY25).

* Commodity derivatives also benefited from market volatility, with revenue growing 39% QoQ and contributing 4% to GROWW’s total operating revenue. Launched in 3QFY26, commodity derivatives currently have 393,000 active users, implying an attach rate of 2.4% in overall active users.

* MTF revenue grew 42% QoQ to INR1.1b (INR170m in 4QFY25), with MTF book scaling to INR28.1b at the end of 4QFY26 (INR23.1b in 3QFY26). The industry MTF book contracted sequentially, but GROWW’s MTF book increased, resulting in a market share rise to 2.7%.

* Credit segment revenue rose 13% YoY/1% QoQ to INR768m. Disbursement by partners as well as Groww Creditserv increased sequentially to INR3.9b each. During the quarter, the credit business contributed 4.1% in consolidated PAT and is expected to strengthen over time.

* The AMC’s AUM has reached INR40b, and it is expected to be profitable as the AUM scales 5-6x over the next few years. The AMC reported an operating loss of INR214m.

* The wealth management business (Fisdom) reported an operating loss of INR102m in 4QFY26 and is expected to be profitable in FY28.

* Customer acquisition cost (CAC) was largely stable at ~INR1,000 with a transacting user base reaching 21.6m at the end of 4QFY26. The volatile market led to a moderation in new user acquisition and a dip in inflows of customer assets on the platform.

* Operating expenses grew 37% YoY/14% QoQ due to 1) risk-related costs because of the higher volatility in 4Q, and 2) higher spending towards CSR as well as M&A due diligence costs. Employee costs are expected to continue growing YoY in line with salary appraisals.

Highlights from the management commentary

* The customer acquisition funnel has evolved over the past year, given weaker equity market performance, with increased acquisition through mutual funds and ETFs.

* Depreciation cost increased during the quarter due to the Fisdom acquisition, while employee costs rose due to investments across multiple functions, including AMC, wealth, and AI initiatives. Headcount stands at ~1,800.

* Risk-related costs within operating expenses increased due to volatility in commodities (Feb’26) and equities (Mar’26), including provisioning for negative client balances. Going forward, operating costs are expected to rise in 1Q (due to appraisal cycle) and stabilize thereafter. Continued investments in AMC and Fisdom will keep consolidated costs elevated.

Valuation and view

* GROWW continues to report strong revenue growth, backed by rising user adoption of products as well as robust user activation. Its brokerage business is gaining market share across segments, with recent product launches, such as MTF and commodities, fueling further growth. The rising number of affluent customers unlocks wealth management opportunities for the company, with the Fisdom acquisition giving a further boost.

* We expect the overall order run-rate in the broking segment for FY27 to largely maintain the 4QFY26 order run-rate backed by market share expansion. MTF segment, LAS, and wealth management are expected to provide a further boost to the top-line. However, this will be offset by a rise in costs, considering investments in AMC and wealth management business, as well as the enhancement of tech capabilities. * We have largely maintained our estimates considering revenue growth on the back of (1) continued growth in order run rate, (2) MTF book expansion, and (3) rising contribution of LAS to the credit segment, offset by rising operational costs. We reiterate our BUY rating with a revised TP of INR235 (premised on 35x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412