Buy Aurobindo Pharma Ltd for the Target Rs 1,680 by Motilal Oswal Financial Services Ltd

In-line quarter; record gross margin in nine years US pipeline, EU penetration, and biologics underpin the next growth leg

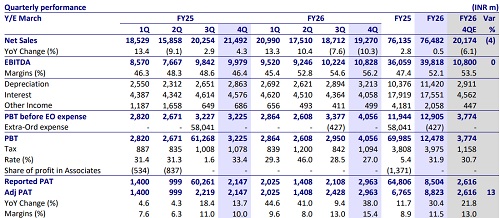

* Aurobindo Pharma (ARBP) posted largely in-line revenue and EBITDA for the quarter. Adj. PAT was slightly below expectations because of higher depreciation, interest costs, and lower other income for 4QFY26. ARBP achieved the highest quarterly gross margin over the past 36 quarters.

* ARBP delivered the highest YoY growth in revenue from the EU segment, led by superior execution and partly supported by favorable currency movement. It has improved the profitability of this segment to at least the company-level EBITDA margin, with scope for further improvement.

* The US sales were muted for the quarter at USD387m, partly due to the high base of the past year and weak seasonality. ARBP aspires to achieve an annual sales run rate of USD2b in the US segment, led by new launches and the Lannett acquisition.

* ARBP is in the process of building a sizeable presence in the global biosimilar as well as biologics contract manufacturing space through building a product pipeline, investing in manufacturing facilities, and subsequent regulatory approval. In addition to 60kl capacity to be commissioned by end-CY26, ARBP would be investing USD150-175m in an additional unit to cater to increased requirements from its customers.

* We largely maintain our estimates for FY26/FY27. We value ARBP at 18x 12M forward earnings to arrive at our TP of INR1,680.

* We expect a 15%/16%/22% CAGR in revenue/EBITDA/PAT for ARBP over FY26-28, led by

1) an enhanced product pipeline in the US

2) increased penetration and additional offerings in the EU market

3) the increase in in-house manufacturing/external sales of PEN-g/6-APA

4) the addition of the Lannett acquisition. Reiterate BUY.

Europe drives performance; product mix benefits offset by higher opex

* Aurobindo's (ARBP) 4QFY26 sales grew 5.6% YoY to INR88.5b (our estimate: INR86.8b), driven by strong Europe performance.

* Gross margin (GM) expanded 190bp YoY to 61.3% due to an improved business mix.

* EBITDA margin contracted 190bp YoY to 20.3% (our estimate: 21.1%).

* EBITDA decreased 3.3% YoY to INR18b (our estimate: INR18.3b).

* Adj. for the same, PAT grew 1.3% to INR9.5b (our est.: INR10.1b).

* Revenue/EBITDA grew 6.1%/1.6% YoY, while PAT was stable YoY in FY26

EU outperformance cushions a soft US quarter

* Overall formulation sales grew 4.6% YoY to INR76.5b.

* US formulations revenue decreased ~13% YoY to INR35.4b (CC: -17.7% YoY to USD387m; ~40% of sales). Europe formulation sales grew ~30% YoY to INR27.9b (11% YoY in CC terms; ~32% of sales). Growth market sales grew 24.7% YoY to INR9.8b (~11% of sales).

* ARV revenue grew ~6.5% YoY to INR3.3b (~4% of sales).

* API sales grew ~13% YoY to INR12.1b (~14% of sales).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412