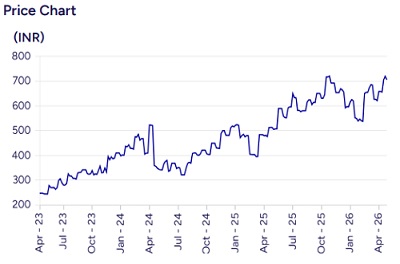

Buy Aster DM Healthcare Ltd For Target Rs. 800 by Prabhudas Liladhar Capital Ltd

Strong growth across clusters

ASTER DM Healthcare’s (ASTERDM) Q4 consolidated EBITDA grew 26% YoY to Rs2.34bn, 12% above our estimates; aided by strong performance across clusters. The QCIL ramp up has been on track with 23% YoY EBIDTA growth for Q4 and 24% YoY for FY26. ASTERDM’s board has recently approved merger with Quality Care (QCIL), making it the third largest healthcare chain by revenue and bed capacity in India. We remain positive on ATSERDM given the rising visibility on post-merger synergies, occupancy improvement, margin expansion and upcoming bed additions. Our FY27E EBITDA stands increased by 3% for combined entity while FY28E broadly remain unchanged. We estimate combined entity post Ind As EBITDA to grow at 22%+ CAGR over FY26-28E to Rs29bn. The combined entity is trading at 26x EV/EBITDA on FY28E (adjusted for minority stake and rental). We maintain our ‘BUY’ rating with revised TP of Rs800/share, valuing 30x EV/EBITDA for the combined entity on FY28E

Strong EBITDA beat aided by healthy growth across clusters:

ASTERDM’s EBITDA (post-Ind AS) grew 26% YoY (declined 10% QoQ) to Rs2.34bn, vs our estimates of Rs2.1bn. OPM improved by 130bps YoY and 190bps QoQ to 19.8%. Pre-Ind AS EBITDA was at Rs2.03bn (up 28% YoY) with OPM of 17.2%. Hospital EBITDA grew by 32% YoY to Rs2.7bn with OPM of 23.2%, up ~240bps YoY. Cluster wise, AP & Telangana cluster reported EBITDA growth of 115% YoY while Kerala and Karnataka cluster reported EBITDA growth of 28% and 26% YoY, respectively. During the quarter newly commercialised greenfield unit in Kasargod reported EBITDA loss of INR 80mn vs INR 130mn in Q3. Pharmacy business reported negative EBITDA of INR 5mn while Labs reported EBITDA of INR 60mn.

Strong ARPOB; occupancy dip QoQ on Kerala nurse’s strike impact:

Consolidated revenue improved 18% YoY (flat QoQ) to Rs11.8bn. ARPOB continues to improve 14% YoY (4% QoQ) to Rs54.3k per day aided by better case mix. Occupancy declined by 200 bps QoQ at 59% due to nurse strike and seasonality impact. IP volumes were up by 7% YoY. ALOS was steady at 3.1 days. Net cash stood at INR 6.3bn as of Q4FY26.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271