Buy Ashok Leyland Ltd For Target Rs. 188 Motilal Oswal Financial services Ltd

In-line earnings CV demand uncertainty to weigh on investor sentiment in near term

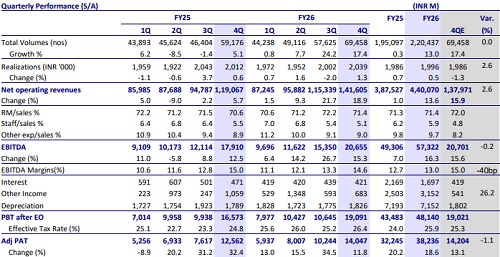

* Ashok Leyland’s (AL) 4QFY26 PAT at INR14b was in line with our estimate. EBITDA margin fell 40bp YoY to 14.6% due to high commodity costs, though still in line with our expectations.

* While the ongoing geopolitical uncertainty is likely to hurt CV demand as well as margins, the impact is likely to be transient, and both demand and margins should normalize from 2H onward. We now factor in AL to post a CAGR of 10%/12%/15% in revenue/EBITDA/PAT over FY26-28E. Its continued emphasis on margin expansion and prudent capex control should help improve returns in the long run. Further, a net cash position will enable AL to invest in growth avenues in the coming years. We reiterate our BUY rating with a TP of INR188 (based on 13x FY28E EV/EBITDA + ~INR10/sh for NBFC).

Earnings in line with estimates

* Standalone revenue grew ~19% YoY to INR141.6b (in line), aided by volume growth of 17.4% to 69.5k units and realization growth of 1.3% to INR2m.

* Commodity inflation led to gross margins reducing 80bp YoY to 28.6% (up 80bp sequentially).

* EBITDA margins contracted 40bp YoY to 14.6% (in line). EBITDA grew 15.3% YoY to INR20.6b (in line).

* Adj. PAT grew ~12% YoY to INR14b, in line with our estimates.

* The board announced a second interim dividend of INR2.5, taking the total FY26 dividend to INR3.5 (vs. INR3.1 in FY25).

* FY26 revenue/EBITDA/PAT grew 14%/16%/19% to INR440b/INR57b/ INR38b.

* OCF/FCF for the year stood at INR48b/INR37b.

* Net cash increased to INR58.9b in 4QFY26, from INR26.2b in 3QFY26 and INR42.4b in 4QY25.

Valuation and view

While the ongoing geopolitical uncertainty is likely to hurt CV demand and margins, the impact is likely to be transient, and both demand and margins should normalize from 2H onward. We now factor in AL to post a CAGR of 10%/12%/15% in revenue/ EBITDA/PAT over FY26-28E. Further, over the years, AL has effectively reduced its business cyclicality by focusing on non-truck segments. Its continued emphasis on margin expansion and prudent capex control should help to improve returns in the long run. Further, a net cash position will enable AL to invest in growth avenues in the coming years. We reiterate our BUY rating with a TP of INR188 (based on 13x FY28E EV/EBITDA + ~INR10/sh for NBFC).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041