Buy Apollo Hospitals Ltd for the Target Rs 9,590 by Motilal Oswal Financial Services Ltd

A broad-based beat; margins hold despite a drag from newer hospitals In the process of adding beds and stores, and improving GMV

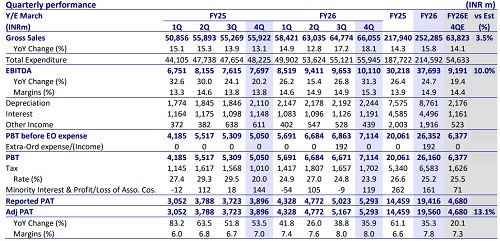

* Apollo Hospitals (APHS) recorded a better-than-expected 4Q performance with a 3.5%/10%/13% beat on revenue/EBITDA/PAT. The company delivered superior operational performance across the three segments – healthcare services, Healthco, and AHLL.

* The healthcare services segment not only delivered robust revenue growth (backed by volume and realization) but also exhibited consistent operating margins. In fact, the company’s 4QFY26 EBITDA margin of 23.9% was recorded after considering operating losses related to newer hospitals.

* The online pharma transactions grew 15% YoY in 4Q. Additionally, APHS has been implementing efforts to rationalize its operating costs in the online pharmacy segment. While the overall store addition has been healthy at 668 in FY26, with 176 being added in 4QFY26. The offline pharmacy margins have been steady at 7.7%, driving 21% YoY growth in offline pharmacy EBITDA.

* The diagnostic business within AHLL has shown strong improvement in financial performance with 41%/54% YoY growth in revenue/EBITDA for FY26.

* We raise our earnings estimate by 4%/6% for FY27/FY28, factoring in

1) improving realization per patient in the healthcare services business

2) optimization of case mix

3) faster reduction in operating losses in Healthco

4) a robust scale-up of the diagnostic business.

* We value APHS on an SoTP basis (30x EV/EBITDA for the hospital business, 25x EV/EBITDA for offline pharmacy, 24x EV/EBITDA for AHLL, and 2x EV/sales for Apollo 24/7) to arrive at our TP of INR9,590.

Highest YoY revenue growth/EBITDA margin in the last eight quarters

* APHS’s 4QFY26 revenue grew 18.1% YoY to INR66.1b (our est: INR63.8b).

* EBITDA margin expanded 155bp YoY to 15.3%.

* EBITDA grew 31.3% YoY to INR10.1b (our est: INR9.2b).

* Adj. PAT grew 36% YoY to INR5.3b (our est: INR4.7b).

* Revenue/EBITDA/PAT grew 16%/25%/35% YoY to INR252b/INR37.7b/ INR19.6b in FY26

All the verticals continue to deliver double-digit YoY growth

* Healthcare services revenue grew 15.8% YoY to INR32.7b, driven by growth in both inpatient volume (+7%), price (+4%), and case mix (5%).

* Healthco revenue grew 20% YoY to INR28.5b.

* AHLL's revenue grew 24.1% YoY to INR4.9b, primarily driven by growth in diagnostics.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412