Buy Apl Apollo Tubes Ltd For Target Rs. 2,250 by Motilal Oswal Financial Services Ltd

Better brand strategy drives margin expansion

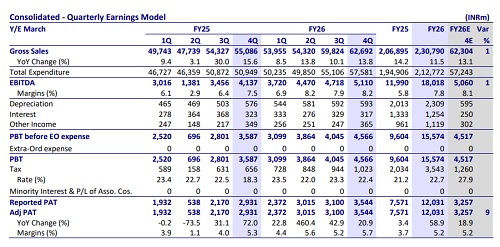

Operating performance in line

* APL Apollo Tubes (APAT) reported a healthy operating performance in 4QFY26 despite geopolitical headwinds (strong performance in Jan and Feb partially offset by a subdued performance in Mar). Its EBITDA grew 24% YoY (up 8% QoQ), fueled by a 9% YoY volume growth and a 14% YoY jump in EBITDA/MT to INR5,525. This growth was led by the company’s strategy of leveraging its brand portfolio across both the premium (APL Apollo) and value (SG) price segments.

* Amid the volatile geopolitical environment, the management has downgraded its FY27 volume growth guidance to 15-20% (vs earlier guidance of 20%) with EBITDA/PAT growth guidance of 20-25%/25-30%. Further, management has raised its EBITDA per MT guidance from INR5,000 to INR5,500.

* We largely retain our FY27/FY28 earnings estimates and value the stock at 35x FY28E EPS to arrive at our TP of INR2,250. Reiterate BUY.

Healthy volume and better gross margin boost profitability

* Consol. revenue grew 14%/5% YoY/QoQ to INR62.7b (est. in line), led by sales volume growth of 9% YoY/1% QoQ to ~924KMT. VAP mix stood at 55% in 4QFY26 vs. 58%/57% in 4QFY25/3QFY26.

* Gross profit/MT was up 13% YoY/9% QoQ at INR10,825. EBITDA/MT rose 14% YoY/7% QoQ at INR5,525 (est. INR5,471). EBITDA grew 24%/8% YoY/QoQ to INR5.1b (est. in line).

* For FY26, Revenue/EBITDA/Adj PAT grew 12%/50%/59% YoY to INR231b/ INR18b/INR12b. EBITDA/MT grew 36% YoY to INR5.2b. Further, total sales volume grew 11% YoY to 34,91,244 MT.

* CFO stood at INR21b vs. INR12b as of Mar’25. Gross debt stood at INR4.5b vs INR6.1b as of Mar’25.

Key highlights from the management commentary

* Market share: Market share has increased to ~60%-65% from 55% last year, supported by capacity expansion funded through internal cash flows, particularly in the East (2 plants), along with higher branding spend focused on SKU optimization and brand visibility.

* Capacity utilization: The Dubai plant is currently operating at roughly 40% capacity amid the ongoing crisis. Additionally, the color-coated and galvanized tubes segment is running at 80–85% utilization due to gassupply constraints. Once the situation normalizes, production could increase ~15–20% from the current levels.

* Inventory management: The company has consolidated production of certain SKUs into a single plant instead of spreading them across multiple facilities, which had earlier led to raw material and inventory build-up at different locations. This strategy proved effective, reducing inventory levels by 30–40k tonnes and leading to a decline of about INR2.5b of inventory QoQ, despite an increase in steel prices.

Valuation and view

* We expect APAT to continue its volume growth momentum, led by brand positioning in the premium and value segments, supported by capacity expansion in key markets, higher exports, and increasing industry demand from housing, solar, and infrastructure. Margin is also expected to improve further, driven by cost optimization measures, increased automation, and a rising mix of value-added products (with a better geographical mix).

* We expect a CAGR of 14%/20%/21% in revenue/EBITDA/PAT over FY26-28E. We broadly retain our FY27E/FY28E earnings and value the stock at 35x FY28E EPS to arrive at our TP of INR2,250. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412