Buy Ambuja Cements Ltd For Target Rs.530 by Motilal Oswal Financial Services Ltd

Weak performance; profitability hit by elevated opex/t Weak

industry demand outlook in FY27; expansion plans deferred

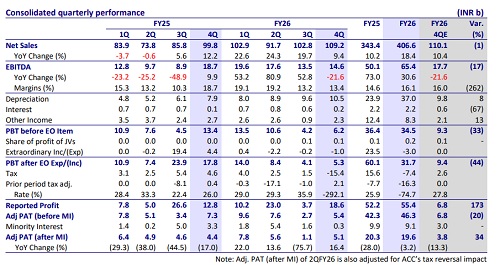

* Ambuja Cements’ (ACEM) 4QFY26 EBITDA was below our estimates due to lower realization and higher opex/t vs. our estimates. Consolidated EBITDA declined ~22% YoY to INR14.6b (-17% miss). Sales volume grew ~9% YoY to 19.9mt (in line). EBITDA/t declined 28% YoY to INR736 (est. INR 884). Profit adjusted for tax reversals and exceptional items (before MI) declined ~26% YoY to INR5.4b (-20% miss).

* Management indicates a cautious near-term outlook, with demand expected to remain soft at ~5.0% growth YoY in FY27. Cost escalation in 4QFY26 was a negative surprise, driven by higher fuel, freight, packing costs, and operating inefficiencies in acquired assets. In 1QFY27, opex/t is estimated to remain flattish QoQ, and management believes this marks the peak of cost/t. The company targets cost reduction of INR250/t p.a. over FY27–FY28 through efficiency and sourcing initiatives. It has adopted a more calibrated and disciplined capex approach, marking a shift from earlier aggressive expansion plans. The capacity targets (140-155 mtpa) are now likely to be deferred by 1-2 years (towards FY30).

* We cut our EBITDA estimates by 13%/3% for FY27/FY28, led by a cut in our volume growth and cost saving estimates. We value the stock at 16x FY28E EV/EBITDA to arrive at our TP of INR530 (earlier INR560). Reiterate BUY.

Opex/t increases ~7% YoY; blended realization/t remains flat YoY

* Consol. revenue/EBITDA/adj. PAT (before MI) stood at INR109.2b/INR14.6b/ INR5.4b (+9%/-22%/-26% YoY, and -1%/-17%/-20% vs. our estimates) in 4QFY26. Consol. volume increased ~9% YoY to 19.9mt. Blended realization/t remained flat YoY to INR5,485 (+1% QoQ; ~1% below estimates).

* Opex/t was up ~7% YoY/1% QoQ (~3% above estimates), led by an increase in other expenses/freight cost/variable cost per ton, rising ~26%/4%/3% YoY. EBITDA/t declined ~28% YoY to INR736, and OPM contracted 5.3pp YoY to ~13%. Depreciation/interest cost increased ~34%/46% YoY, while other income declined ~14% YoY.

* In FY26, revenue/EBITDA/PAT (before MI) stood at INR406.6b/INR65.4b/ INR25.4b (+18%/+31%/+7% YoY). Sales volume grew ~16% YoY, aided by inorganic growth. Realization/t was up ~2% YoY to INR5,457. EBITDA/t grew ~13% YoY to INR878. OCF stood at INR53.6b vs. INR22.4b in FY25. Capex (net of proceeds) stood at INR59.6b vs. INR85.9b. Net cash outflow stood at INR5.9b vs. INR63.5b in FY25.

Highlights from the management commentary

* Pricing remains a key challenge, with the industry witnessing only marginal price improvements INR10/bag (selective geographies seeing INR15–20) in Apr’26. Pricing power remains weak due to subdued demand conditions.

* The company is prioritizing improving utilization of existing assets and stabilizing past acquisitions before committing to the next leg of expansion. Organic growth remains the primary focus, while inorganic opportunities will be evaluated selectively.

* Capex is pegged at INR60b–65b in FY27. A large portion of this relates to projects already under execution, including capacity additions, WHRS, fly ash transportation systems, debottlenecking, and maintenance capex.

Valuation and view

* ACEM’s 4QFY26 performance was below our as well as consensus estimates, mainly due to the cost overhang. It has reported lower profitability vs. peers (so far results announced). While management had indicated in its 3Q earnings concall that opex/t had normalized by end-Dec’25 and was likely to decline in 4QFY26, it instead remained elevated, led by higher branding and packing costs, along with incremental shutdown-related costs, higher lead distance, and additional goods tax in certain states. We estimate near-term performance to remain under pressure amid cost escalation and muted pricing, while, in the long term, various internal cost efficiency measures and a single cement platform will help the company improve overall performance.

* We estimate a CAGR of ~11%/18%/19% in consol. revenue/EBITDA/PAT over FY26-28, led by volume growth of ~9%. We estimate its EBITDA/t at INR856/ INR1,053 in FY27/FY28 vs. INR887 in FY26. ACEM currently trades at 18x/13x FY27E/FY28E EV/EBITDA and USD99/USD93 EV/t. We value the stock at 16x FY28E EV/EBITDA to arrive at our TP of INR530 (earlier INR560). Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)