Buy Ambuja Cement (ACEM IN) Ltd for the Target Rs.640 by PL Capital

Quick Pointer

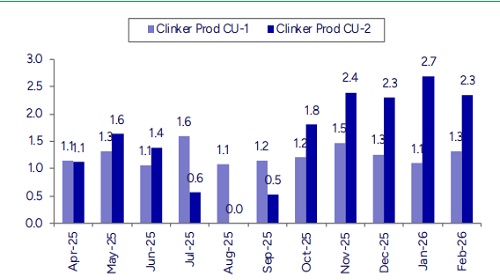

Sanghi’s variable cost is expected to reduce to ~Rs1,500/t from Rs2,000 leading to EBITDA expansion. ACEM’s opex to reduce QoQ for Q4

Two new proposed kilns expansion will be taken up once utilization reaches ~85%. Mgmt is targeting ~15% RoI prior to any further capacity expansion.

We visited Ambuja Cement’s Sanghipuram plant in Kutch (Gujarat), one of the largest integrated cement facilities with cement/clinker capacity of ~6.1mtpa/6.6mtpa (two kilns of 9,000tpd and 10,000tpd) and benefits from ~1Bt of high-quality limestone reserves. Management indicated that current operational cement capacity of ~17,000tpd could increase by ~2,500tpd through debottlenecking, taking capacity to ~20,000tpd (~7mtpa). The company has planned ~Rs6bn capex focused on efficiency improvements including WHRS (~18MW). Sanghipuram also benefits from coastal logistics through its jetty, enabling clinker and cement movement to markets such as Tuticorin, Dahej and Mumbai, with logistics costs of ~Rs700/t Vs pan-India average of ~Rs900/t. The plant also has ~130MW captive power capacity, supporting cost competitiveness. Management reiterated its focus on value over volume-led growth and expects further cost reductions ahead (QoQ).

We believe Sanghipuram represents a strategically important asset within Ambuja’s western India network given its large limestone reserves, coastal logistics advantage and scope for efficiency improvement. While management has set an ambitious target of reducing variable costs by Rs500/t to ~Rs1,500/t at Sanghi resulting an EBITDA/t improvement to ~Rs1,800-2,000/t (from c. ~Rs1,200-1,500/t), we believe timely execution will be the key. Improving Railway connectivity to Kutch, jetty capacity expansion and ongoing transmission augmentation would help ACEM over medium term. We remain constructive on Ambuja’s long-term growth prospects given its initiatives on improving cost efficiencies and ongoing expansion strategy. Maintain BUY with TP of Rs640 valuing the company at 17x EV/Mar’27E EBITDA. At CMP, the stock is trading at 12.5x/10.7x EV on FY27E/28E EBITDA.

Above views are of the author and not of the website kindly read disclaimer