Buy Aditya Birla Capital Ltd for the Target Rs. 430 by Motilal Oswal Financial Services Ltd

Strong execution across business segments

Lending (HFC+NBFC) book grew ~32% YoY; NBFC GS2+G3 down ~40bp QoQ

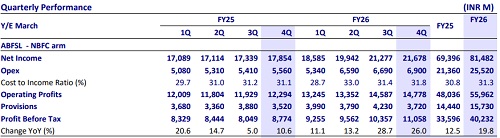

* Aditya Birla Capital’s (ABCAP) 4QFY26 consolidated revenue grew 12% YoY to ~INR159b and consolidated PAT (excl. one-off items) grew ~30% YoY to ~INR11.2b. FY26 PAT grew ~21% YoY to INR38b

* Overall lending book (NBFC and Housing) grew 32% YoY/9% QoQ to ~INR2.08t. Total AUM (AMC, Life insurance and health insurance) grew ~16% YoY to INR5.91t. Mutual fund quarterly average AUM grew 14% YoY to INR4.36t.

* Life Insurance individual FYP grew by ~15% YoY to INR47.2b in FY26 and Health Insurance GWP grew ~39% YoY to INR68.5b in FY26. Udyog plus, a B2B platform for MSMEs, scaled up to AUM of INR58b.

NBFC: AUM up ~27% YoY; NIM declines ~4bp QoQ

* NBFC loan book grew ~27% YoY and 8% QoQ to ~INR1.6t. 4QFY26 disbursements grew ~28% YoY and ~16% QoQ to ~INR250b.

* NIM declined ~4bp QoQ to 6.08%. PBT grew ~26% YoY to INR11b. FY26 PBT grew 20% YoY to INR40b. 4QFY26 RoA stood at ~2.3%.

* The company reported a sequential improvement in asset quality, with GS2 + GS3 assets declining ~40bp QoQ to ~2.4%.

* Management shared that its asset quality remains strong, with continued improvement across product segments, including unsecured business loans and the personal and consumer (P&C) segment. Credit costs stood at ~1.04% (PQ: 1.23%) in 4QFY26. Management highlighted that credit costs are at their lowest levels in the past few years and expects them to remain broadly stable at ~1.1-1.2% in FY27. We estimate credit costs of 1.2%/1.25% in FY27/FY28E.

* Management indicated that the retail and MSME segments will continue to be the primary growth drivers, with sustained emphasis on deepening customer relationships and expanding digital sourcing platforms. With an improving credit environment, the share of unsecured and P&C segments in the loan mix is expected to increase by ~2pp over the next few quarters, which should support NIM expansion of ~25bp.

HFC: Robust growth in HFC AUM; asset quality improves further

* HFC AUM grew 53% YoY/12% QoQ to ~INR475b. 4Q disbursements grew 37% YoY/29% QoQ to ~INR80b. NIM declined ~8bp QoQ to ~4.05%

* PBT grew more than 2x YoY to INR2.55b. 4Q RoA stood at 2.07%. Asset quality improved with GS2+ GS3 declining ~20bp QoQ to ~0.75%. S3 PCR rose ~15bp QoQ to ~59%.

* Management indicated plans to open ~100 branches in FY27, with a focus on Tier 2 and Tier 3 markets to enhance penetration. The company targets AUM of INR1t over the next 24-30 months, indicating strong growth visibility. We model loan book CAGR of ~38% over FY26-FY28E.

Asset Management: QAAUM rose ~14% YoY; Equity QAAUM grew 17% YoY

* Mutual fund Quarterly Average AUM (QAAUM) rose 14% YoY to ~4.36t with equity mix at 45.3%. Individual monthly average AUM grew by 8% YoY to INR1.99t as of Mar’26.

* Equity QAAUM grew ~17% YoY to INR1.97t.

Life Insurance: Individual FYP grew ~15% YoY; 13M persistency at 86%

* Individual FYP grew 15% YoY to ~INR47.2b, while renewal premium grew 17% YoY to INR12.2b in FY26.

* Value of new business (VNB) grew by 29% YoY to INR10.5b in FY26 and Net VNB margin rose 260bp YoY to ~20.6% as of Mar’26. 13M persistency stood at 86% in FY26.

* Management guided for a ~20-22% CAGR in individual FYP over the next three years, with a continued focus on expanding VNB margin to over 18%.

Health Insurance: GWP grew 39% YoY; market share stood at 13.7%

* GWP in the Health insurance segment grew 39% YoY to ~INR68.5b in FY26 and combined ratio stood at 103% in FY26.

* SAHI market share stood at ~13.7% in 4QFY26.

Highlights from the management commentary

* Management shared that there has been no material impact from geopolitical tensions in West Asia on the portfolio so far; however, the company remains cautious and continues to monitor macro developments closely.

* In the housing business, the company expects credit costs to remain stable, and with the benefit of further operating efficiencies, it has guided for RoA to be in the range of 2.0-2.1% in FY27. RoE is likely to remain at ~11.5-12.0% in the near term due to the recent capital infusion; however, it is expected to exceed 15% over the next 12-24 months.

Valuation and view

* ABCAP’s operational metrics continued to strengthen during the quarter, with healthy loan growth across both HFC and NBFC segments. Asset quality improved further across all products, including the unsecured portfolio. While NIM exhibited some pressure during the quarter, management expects a recovery over the next couple of quarters, supported by a higher share of unsecured loans in the loan mix.

* We expect a consolidated PAT CAGR of ~30% over FY26-28. The thrust on crossselling, investments in digital, and leveraging ‘One ABC’ should drive healthy profitability, resulting in RoE of ~16% by FY28E. Reiterate BUY with an SoTP (Mar’28E)-based TP of INR430.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041