Automobiles , Auto Ancillaries Sector Update : Macro headwinds weigh on global demand by Elara Capital

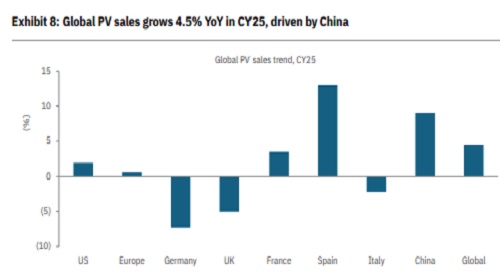

In our global auto volume tracker series, we analyze global sales and results conference calls of key global original equipment manufacturers (OEM), which have released results to date. While CY25 global PV sales grew by ~4.5% YoY (China, the US and Europe up 9.1%, 1.9% & 0.5%, respectively), the start to CY26 has been muted with global growth (provisional) at -1.2% (China, US and Europe down 6.8%, 0.8% & 3.9%, respectively) in January 2026. The decline in China was due to subsidy roll-off, which led to pre-buying in Q4CY25; hence, new energy vehicles (NEV) mix saw a sharp fall to 40.3% in Jan vs 52.3% in December 2025. US sales took a hit from rising vehicle prices and affordability concerns along with the expiration of the USD 7,500 federal EV tax credit. Among key results highlights are: 1) OEM continue to see muted demand in CY26, citing flat to a slight increase in US & Europe and continued challenging environment in China (MB guiding for sales growth of -2% to +2% for themselves globally), 2) tariffs will remain headwinds into CY26, 3) continuing challenges of higher raw materials prices and supply chain issues, with memory chip shortages being the latest, and 4) intensifying EV product-related write-offs. On the other hand, the CV demand (Class 8) outlook from Volvo has seen an upgrade and now expect CY26 growth at 2.9% for Europe and 2.7% for the US. The global PV production is expected to decline by 0.2% in CY26, as per S&P Mobility’s February 2026 forecast. While the MENA region contributes only 3-4% of global demand, the indirect impacts in terms of higher crude/energy price, higher freight rates and supply chain disruptions are key monitorable.

Growth in EV sales in major markets in CY25: China continues to lead BEV sales growth in CY25 (34% YoY growth), followed by Europe at 31%. BEV penetration was ~32%, 18% and 8% in China/Europe/US respectively in CY25, with the US BEV market seeing a sharp contraction in the range of 30-40% post removal of federal tax credit since October 2025. China too saw a sharp contraction in BEV penetration in January to 26.8% post subsidy rolloff in December 2025. In the EU, Germany has reintroduced a new EV (applicable for BEV, PHEV and EREVs) subsidy program with effect from January, allocating ~EUR 3bn, which would support 800,000 new EVs. In CY25, the overall share of China’s brands in the EU reached ~6% vs 3% in CY24. In CY25, ex-China brands, Europe sales contracted by 1% YoY.

Focus on multi-energy powertrain gain traction: Global OEM have taken huge write-offs related to EV programs and are rethinking their BEV strategy: 1) Stellantis has taken a onetime adjustment of EUR 25.4bn - platform impairment charges of ~EUR 6.6bn, program cancellations of EUR 9bn and warranty reassessment of ~EUR 4.1bn, 2) Ford will take USD 7bn in charges during CY26-27 to shift toward multi-energy platforms, including the disposition of BOSK (JV of Ford and SK On, the battery arm of the SK Group) (total charges of USD 19.5bn), and 3) GM’s USD 7.6bn total charges in H2CY25 for rightsizing capacity and discounting its BrightDrop subsidiary that develops EV vans.

Read-through for India-listed companies under our coverage: Slowing global PV growth as well as shrinking profit pool of global OEM in China, and market share pressures of legacy OEM in the EU are cause for concern for SAMIL (with limited organic growth potential; we reiterate Sell). Some US OEM have started to focus on ICE and hybrid models (albeit removal of the federal credit on BEV), which means the ICE and hybrid product segment (starter motor) for SONACOMS could see growth in the medium term vs a structural decline expected earlier. However, growth pressures for Tesla remain an overhang for SONACOMS. For JLR, China is a structural concern (as is case for legacy OEM) along with higher exposure to MENA regions (7-8%) (retain REDUCE on TMPV). The CV space has started to see some upgrades recently (from Volvo), which implies bottoming of demand and recovery underway -- likely positive for TTMT and BHFC.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...