Oil and Gas Sector Update : Big boost for OMCs; RIL profitability lower than what GRMs suggest by Motilal Oswal Financial Services Ltd

* On 27th Mar’26, the central government cut excise duty on HSD/MS by INR10/ltr and imposed a tax of INR21.5/INR29.5 per ltr on the export of HSD/ATF. Key implications for Reliance Industries (RIL) and oil marketing companies (OMCs) are as follows:

* Govt steps in to help OMCs as challenges continue: While the excise duty cut of INR10/ltr on MS/HSD should lower under-recovery for OMCs, current underrecoveries on MS/HSD (pre-excise adjustment) remain highly volatile at INR20- 30/ltr. As such, even after these measures, OMCs continue to incur significant losses on auto-fuel retail sales. In addition, we estimate a further ~INR4/ltr benefit for HPCL/BPCL/IOCL due to the export tax on high-sulfur diesel (HSD), which lowers the refinery transfer price (net benefit will accrue only on external volumes). Lastly, we see scope for a retail price increase of INR2-4/ltr if a lowto-moderate intensity conflict continues to simmer over the coming months.

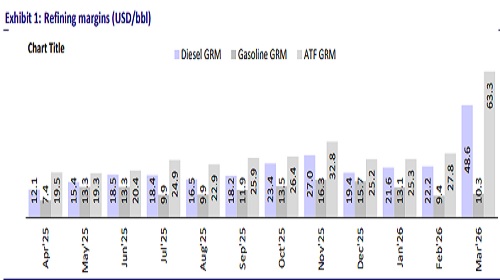

* RIL – HSD/ATF export tax crimps overall GRM by ~USD2/bbl: The government on 27th Mar’26 announced the imposition of a windfall tax of INR21.5/INR29.5 per ltr on HSD/ATF exports. Assuming the tax is not applicable on RIL’s SEZ volumes (was applicable only for initial fortnight post Russia-Ukraine war), we estimate an impact of ~USD2/bbl on overall gross refining margin (GRM).

* Actual refiner profitability likely to be lower than what headline GRMs suggest: While recent HSD GRMs have been in the USD50-60/bbl range and refiners, including RIL, are making higher profits vs. before the Israel-Iran war, actual refining profitability may be lower than what headline GRMs suggest due to: (1) higher fuel loss at complex refineries (2-3%), translating into ~USD2- 3/bbl impact; (2) a sharp rise in VLCC freight costs (~USD2/bbl impact); and (3) export tax calculations are likely based on GRMs over Brent, whereas crude sourcing currently often involves paying a premium (thus overstating GRMs).

* Propane diversion, lower profitability at Jio-BP are additional challenges: In addition, RIL has diverted propane toward LPG production, given the domestic LPG shortage and this is likely to weigh on profitability. RIL has also not implemented any retail fuel price hikes despite a sharp rise in crude prices.

Valuation and View

* We have a BUY rating on HPCL and Neutral on BPCL and IOCL. Our earnings estimates for OMCs have not been revised to account for the recent underrecoveries on auto-fuels.

* We reiterate our BUY rating on RIL with a TP of INR1,750. Using the SoTP method, we value the O2C/E&P segments at 7.5x/5.0x FY28E EV/EBITDA to arrive at an enterprise value of INR5.7t (or ~INR420/sh) for the standalone business. We ascribe an equity valuation of INR590/sh and INR560/sh to RIL’s stake in JPL and RRVL, respectively. We assign INR174/sh to the New Energy business, INR30/share equity value to RCPL, and INR26/sh to RIL’s stake in JioStar.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Industrials ? Solar Pumps Sector Update : Q1FY27 Preview: Policy Catalyst to Drive Earnings ...