MCX Silver September is expected to slip towards Rs 210,000 as long as it trades under Rs 220,000 - ICICI Direct

Metal’s Outlook

Bullion Outlook

• Spot gold is likely to face a hurdle near the $4,060–$4,100 zone and may trade lower toward $3,950. Escalating Middle East tensions are raising inflation concerns, which could lead to tighter monetary policy. U.S. launched multiple strikes against Iran this week, and President Donald Trump warned that U.S. forces could target the country's infrastructure next week without a diplomatic breakthrough. Additionally, ongoing ETF outflows are expected to pressure prices. Moving forward, investors will closely monitor key U.S. economic data and speeches from Fed officials to gauge the central bank's next policy moves

• MCX Gold Aug is expected to face hurdle near Rs 142,000 level and likely to slip towards Rs 140,000 level. Only a move below Rs 140,000, it would turn lower towards Rs 137,500.

• MCX Silver September is expected to slip towards Rs 210,000 as long as it trades under Rs 220,000.

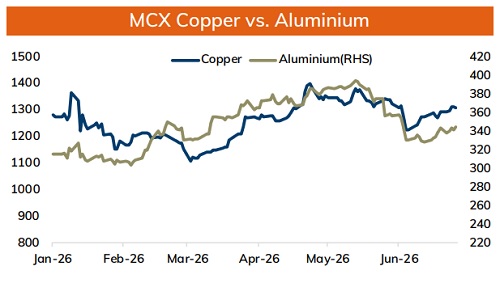

Base Metal Outlook

• Copper prices are expected to trade lower pressured by soft demand and mixed economic indicators from China, alongside heightened geopolitical risks. The prospect of tight monetary policy from the U.S. Federal Reserve is also weighing on the metal. However, the downside remains limited amid tightening physical market conditions. Depleting LME stockpiles and falling treatment and refining charges point to a severe shortage of raw materials. Furthermore, supply disruptions in South America and accelerated stockpiling ahead of potential U.S. Section 232 tariffs would continue to provide underlying support.

• MCX Copper July is expected to slip towards Rs 1300 - Rs 1305 as long as it trades under Rs 1320 level.

• MCX Aluminum July is expected to move higher towards Rs 345 - Rs 346, as long as it stays above Rs 339. MCX Zinc July is likely to hold above Rs 373 and rise towards Rs 378 -Rs 380 level. Only a move below Rs 373, it would slip towards Rs 368- Rs 370 zone.

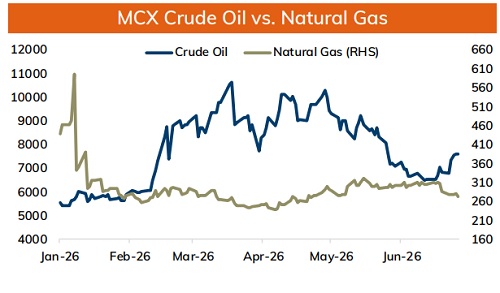

Energy Outlook

• NYMEX crude is likely to hold above $78 and move toward $81.50 per barrel amid escalating geopolitical tensions in the Middle East. Following U.S. naval blockade of Tehran’s maritime routes through the Strait of Hormuz, the conflict risks an unprecedented shock to the global energy supply chain. If both the Strait of Hormuz and the Bab el-Mandeb Strait are compromised, it could cause an immediate spike in global crude prices and severely restrict Middle Eastern export corridors.

• On the data front, fresh OI addition seen across ATM and OTM Put strikes, with highest OI concentration at $75 and $78 strike, which would likely to act as major support. On the other hand, call unwinding was also observed. Immediate call base exist at $80. Any sign of further unwinding would push prices towards the next major call base at $85. MCX Crude oil August is likely to move towards Rs 7850 - Rs 7900 as long as it holds above Rs 7500.

• MCX Natural gas July is expected to hold above Rs 272 - Rs 274 level and rise towards Rs 285 level.

Please refer disclaimer at https://secure.icicidirect.com/Content/StaticData/Disclaimer.html

SEBI Registration number INZ000183631