MCX Silver July is expected to dip towards Rs 229,000 - Rs 225,000 level as long as it stays below Rs 239,000 level - ICICI Direct

Metal’s Outlook

Bullion Outlook

• Spot Gold is likely to remain under pressure amid firm dollar and rise in US treasury yields. Further, prices may slip on anticipation that US Federal Reserve may maintain hawkish stance and hike interest rate by the end of the year. According to CME FedWatch tool markets are now pricing 89% chance of a rate hike in December, up from 61% before the Federal Reserve's meeting last week. Additionally, investors will remain cautious ahead of slew of economic data from US to gauge economic health and get more clarity on interest rate trajectory. If data comes on stronger note then it would signal resilience in the economy, adding to rate hike expectations. Meanwhile, sharp downside may be cushioned on early signs of progress in ongoing peace talks between the US and Iran

• MCX Gold Aug is expected to slip further towards Rs 146,000- Rs 145,000 level as long as it stays below 149,500 level

• MCX Silver July is expected to dip towards Rs 229,000 - Rs 225,000 level as long as it stays below Rs 239,000 level.

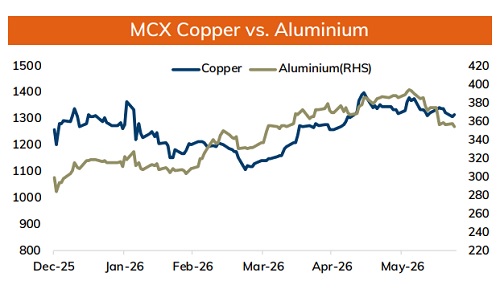

Base Metal Outlook

• Copper prices are expected to trade with positive bias amid rise in risk appetite in the global markets. Further, prices may move higher on growing optimism that US-Iran talks could pave the way for a deal to end the war in Middle East. Additionally, prices may get further support from ongoing concerns about US import tariffs and persistent decline in inventory at LME registered warehouses. Meanwhile, sharp upside may be capped as investors will remain vigilant ahead of Manufacturing PMI data from major economies, to gauge the economic health and demand outlook

• MCX Copper June is expected to rise towards Rs 1325 level as long as it stays above Rs 1295 level. Only break below Rs 1295 level prices may be pushed towards Rs 1290 - Rs 1285 level

• MCX Aluminum June is expected to slip towards Rs 349 - Rs 346 level as long as its stays below Rs 359 level. MCX Zinc June is likely to face stiff resistance near Rs 372 level and slip towards Rs 362 - Rs 359 level.

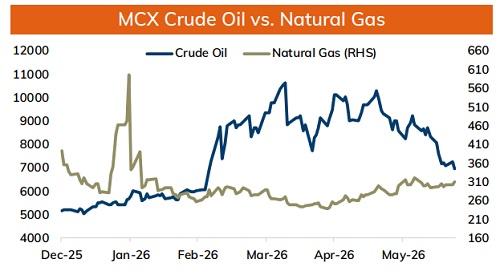

Energy Outlook

• NYMEX Crude oil is likely to trade with negative bias amid ease in supply concerns as US and Iran negotiations made headway. Further, prices may slip as US issued a 60-day license allowing Iran to sell oil on the international market, adding more oil in market. Iran may ramp up its oil exports amid removal of US blockade of Iranian port as a part of ceasefire extension agreement. Moreover, prices may slip as traffic through the Strait of Hormuz has picked up, with producers including Kuwait and the United Arab Emirates finding alternative routes to export energy. Additionally, Iraq plans to restore crude production gradually to between 4.2 million and 4.3 million barrels per day.

• MCX Crude oil July is likely to slip towards Rs 6800 - Rs 6700 level as long as it stays below Rs 7300

• MCX Natural gas July is expected to slip towards Rs 305 - Rs 300 level as long as it stays below Rs 320 level.

Please refer disclaimer at https://secure.icicidirect.com/Content/StaticData/Disclaimer.html

SEBI Registration number INZ000183631