The Economy Observer : 4QFY26 GDP: Services and fixed investments drive growth by Motilal Oswal Financial Services Ltd

Services and investments drive growth in FY26; moderation ahead

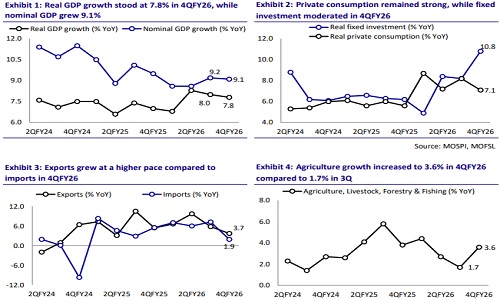

* Real GDP growth moderated marginally to 7.8% in 4QFY26 from 8.0% in 3QFY26, but remained stronger than 7.0% in 4QFY25 and was 30bp above our expectation of 7.5%. The slight sequential moderation was driven by a sharp slowdown in manufacturing activity and softer external demand, partly offset by continued strength in services, improving agricultural growth, and accelerating investment spending.

* At current prices, GDP expanded by 9.1% in 4QFY26 versus 9.2% in 3QFY26.

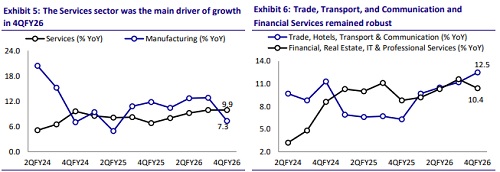

* Services remained the key growth driver, with services GVA growing 9.9% YoY in 4Q, supported by strong momentum in trade, transport, and hospitality services (12.5% YoY) and robust financial services (10.4% YoY). On the other hand, manufacturing growth slowed sharply to 7.3% YoY in 4QFY26, contributing to the moderation in overall GDP growth, while construction activity and agriculture improved sequentially.

* Investments emerged as the strongest demand-side support, with fixed investment growth accelerating to 10.8% in 4QFY26 vs. 8.2% in 3Q. Private consumption remained healthy, although growth softened slightly to 7.1% YoY in 4Q from 8.2% in 3Q, indicating resilient household demand despite rising uncertainties. External demand weakened, with export growth slowing amid a softer global environment and the early effects of geopolitical tensions and commodity price volatility following the conflict’s escalation in late February.

FY26 real GDP growth accelerated to 7.7% in FY26

* India's GDP growth accelerated to 7.7% YoY in FY26, exceeding our expectations (7.5% YoY) and improving from 7.1% in FY25. The Services segment was the primary growth engine, with strong performance delivered across trade, financial services, real estate, IT, and professional services.

* Nominal GDP growth moderated to 8.9% in FY26, lower compared with a growth of 9.7% in FY25.

* Industrial activity remained robust, led by double-digit manufacturing growth and sustained strength in construction.

* Domestic demand strengthened significantly, with both private consumption and investment growth accelerating during the year.

* Growth remained strong through most of FY26, peaking at 8.3% in 2QFY26 before moderating slightly in 4QFY26.

Outlook: Expect real GDP growth at 6.5% in FY27

* Several headwinds are likely to weigh on India's growth outlook in FY27, prompting us to forecast GDP growth at 6.5%, broadly in line with the RBI's revised estimate of 6.6%, down from 6.9% earlier. Weather-related risks have intensified, with concerns around the possible development of a Super El Niño event and the IMD forecasting monsoon rainfall at around 90% of the Long Period Average (LPA), which could affect crop output, rural incomes, and food inflation. However, the impact on aggregate GDP is likely to be less severe than in the past, given the declining share of crop production in the economy and the broader composition of agricultural GVA.

* Industrial growth is expected to moderate as higher crude oil and commodity prices stemming from geopolitical tensions compress corporate margins and profitability. However, electricity and utility sector growth could remain relatively strong, supported by rising power demand amid persistent heatwave conditions and increasing cooling requirements. Within services, financial, real estate, and professional services are likely to continue performing well, supported by strong credit growth, financialization, and formalization of the economy. In contrast, trade, hotels, transport, and tourism-related services could witness some moderation from the exceptionally strong growth recorded in FY26 amid weaker discretionary spending and a softer global environment.

* On the demand side, private consumption could soften, particularly in rural India, where food has a higher weight in the CPI basket, making households more vulnerable to weather-driven food inflation. Investment growth is also likely to moderate in FY27, with central government capex potentially lower by around INR1t due to fiscal pressures, although spending is still expected to remain at a sizeable INR11.2t, while state government capex could remain robust at INR9– 10t. Private capex is likely to stay subdued amid elevated uncertainty. Exports are expected to remain weak, led by merchandise trade, while services exports, though resilient so far, face emerging medium-term risks from the rapid adoption of AI and automation, particularly in lower-value IT and business-process service segments.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412