Structural reset in UK gilts by CareEdge Ratings

Executive summary

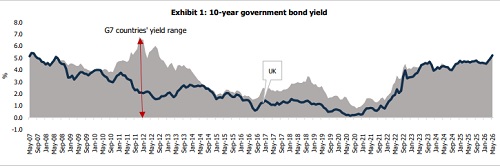

The UK now faces the highest borrowing costs amid the G7 countries following a sharp rise in government bond yields (see Exhibit 1). This spike is driven by three key catalysts:

1. Macroeconomic challenges such as sluggish growth and constrained fiscal space: In 2026, the UK is expected to post low growth rate at 0.8%, high fiscal deficit at 3.1% of GDP, and high debt at 103.1% of GDP.

2. Elevated policy rate: Despite moderating food and energy prices, persistent services inflation and strong wage growth keep the UK’s headline inflation above the Bank of England's (BoE) 2% target. Consequently, prolonged high policy rates continue to raise borrowing costs and bond yields.

3. Bond ownership shifts towards price-sensitive investors such as private and overseas participants: The investor base has moved away from traditional, stable holders such as pension funds and insurers towards more price?sensitive and globally-oriented participants. The BoE has transitioned from being a major buyer of bonds to actively reducing its holdings through quantitative tightening. Consequently, the market risk premium has increased.

UK bond yields reflect a new market-driven equilibrium

Higher UK bond yields reflect a new, market-driven equilibrium than a deterioration in macroeconomic fundamentals compared with G7 peers. Notably, the UK’s credit profile is supported by the following factors:

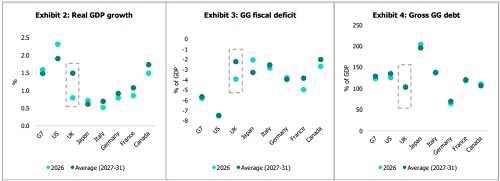

a) It is not an outlier on macroeconomic factors among the G7. Moreover, these factors are projected to improve at a better pace over the next five years, as per IMF WEO projections (see Exhibits 2-4).

b) The UK benefits from important structural strengths such as reserve currency, global financial centre status, and strong institutions & governance framework.

c) Market indicators have shown continued investor confidence, with strong demand for gilts and stable market credit risk measures.

UK is not an outlier among G7; its macroeconomic indicators are improving

According to the IMF WEO, despite growing at 0.8% in 2026, the UK is expected to perform better than Italy, Japan, and Germany. Its growth rate is projected to nearly double over 2027-31 due to higher productivity, while other G7 peers are expected to see limited improvement (see Exhibit 2).

According to the IMF Article IV report, the UK will face increasing spending pressures over the coming years. These pressures could add about 3% of GDP to public spending by 2031. The main reasons are ageing population, rising healthcare and pension costs, higher defence spending, and the need for climate change-related investment.

At the same time, the UK has limited flexibility in its public finances. Taxes are already rising and are expected to reach around 38% of GDP by 2031, which would be one of the highest levels in recent history. Economic growth is also expected to remain modest, averaging 1.4% per year, which will make it difficult to expand the government’s revenue base further.

Despite these fiscal challenges, the UK’s debt ratio will remain the lowest among G7 countries except Germany

Looking ahead, the UK’s fiscal metrics are expected to improve. Its fiscal deficit (as % of GDP) is expected to narrow significantly, by about 2.3 percentage points (pp), while improvements in G7 economies are likely to be much smaller, by average of 0.3pp (see Exhibit 3).

Similarly, the UK’s debt-to-GDP ratio is expected to slightly improve, by about 1pp vs a deterioration of average of 9pp for other countries (see Exhibit 4). This suggests that fiscal fundamentals alone do not fully explain why UK government bond yields are relatively high and volatile. Instead, there are deeper structural factors at play.

Structural changes in UK government bond market

While the UK faces rising spending pressures and tight fiscal flexibility, its position is not weakest among G7 peers, as detailed above. To understand why the UK government’s borrowing costs are relatively high, it is helpful to break them into two components: the central bank’s interest rate and the extra return (or premium) that investors demand to hold UK government bonds.

a) Stubborn inflation keeps the BoE cautious and policy rates higher for longer The UK’s headline inflation has remained above the BoE’s 2% target since the Russia-Ukraine energy shock. Although energy and food pressures have eased over time, core inflation has stayed higher than in the Euro area. One major reason is the initial energy shock, which hit the UK harder because of its limited gas storage capacity and higher exposure to global energy markets (see Exhibit 5).

Over time, the drivers of inflation have changed-from external factors such as energy prices to domestic factors. In particular, services inflation, such as rents and labour-intensive sectors, has remained high due to tight labour markets and supply constraints.

Additionally, the increase in “administered” prices-those influenced or partly controlled by the government, such as water bills, public transport fares, and some housing costs-has widened the inflation gap between the UK and the Euro area. These have risen faster in the UK than in peer economies, driving the international divergence.

Persistent inflation has constrained the BoE’s capacity to cut interest rates. Consequently, the BoE has cut interest rates more cautiously than the European Central Bank (ECB). This has led to a “higher for longer” interest rate environment. Resultantly, borrowing costs in the gilt market have remained high, as investors price in prolonged high interest rates and demand extra returns for holding UK government bonds (see Exhibit 6).

Above views are of the author and not of the website kindly read disclaimer