Silver to witness an upside of 20% in its price per oz in the next one year: Emkay Wealth Management

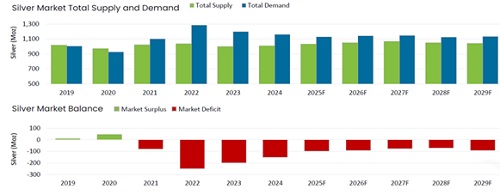

Emkay Wealth Management, the wealth management and advisory arm of Emkay Global Financial Services in its latest research cited that, the price of Silver is expected to touch USD 60 per ounce in the next one year, a potential of 20% YoY from the current price level owing to growing industrial demand. The current supply deficit to demand is currently recorded at 20%, and is expected to be in deficit for the foreseeable future.

Gold returns have been on par with equities and above bonds since the end of the gold standard. In the year to date terms, till 8th October, gold has made a return of 61.82% whereas other asset classes such as Indian equities, bonds have registered a return of 4.2% (Nifty 500 TRI) and 8.4% (Crisil Short Term Bond Index) respectively. Prices of precious metals closely intertwined with US Dollar currency movements. The expected rate cuts in US may lead to some decline in the dollar further providing support to price growth in gold.

Mr. Ashish Ranawade, Head of Products, Emkay Wealth Management said “Increased preference for gold as against US Dollar by institutional investors and central banks at the heart of appreciation in precious metals. Demand-supply dynamics are favorable to bring upward mobility in silver prices and technically near a break out zone for all time prices.”

Indian equity markets continue to be in the expensive zone relative to growth. Nifty 100 is valued at 21.8, Nifty Midcap 150 at 33.6, Nifty Smallcap 250 at 30.43 and Nifty Microcap 250 at 28.88.

Domestic Investors continue to pour money into Indian Equities.

Dr. Joseph Thomas, Head of Research, Emkay Wealth Management said “Structurally, India is expected to be an outlier in global economic landscape.A spate of IPOs has made India a much wider market than what the indices indicate. Stock specific opportunities remain prevalent for Indian investors. We expect PMS and AIF and active fund managers should do well.”

According to Emkay Wealth, attributes such as high growth-large market, digital leadership, infra push, reform momentum, China+1 strategy, sectoral strengthens and most importantly geopolitical balanced strategic partnerships will further usher the compelling growth story of India.

The United States, one of the largest consumer markets in the world, has imposed wide-ranging tariffs across multiple countries — creating massive disruptions in global supply chains. A stark example is the U.S. auto industry, which has been significantly impacted due to tariffs on Mexico and Canada. Traditionally, automobile components would cross the U.S.-Mexico-Canada borders nearly five to six times during the manufacturing and assembly process. The introduction of tariffs has severely disrupted this cross-border flow, amplifying costs and delays across the ecosystem.

This disruption is not limited to North America. India, too, has borne the brunt, facing some of the highest tariffs — as steep as 50% — on its exports to the U.S.

Adding to these trade frictions are the ongoing geopolitical conflicts — particularly the wars in Ukraine and the Middle East — which have deepened global polarization and forced countries to take sides. These conflicts have further strained global trade flows and supply lines that were steadily strengthening over the past two decades.

Such global-scale disruptions are unprecedented. While technological or product disruptions have often been viewed positively for fostering innovation, this time the world is witnessing a macro-level disruption that is reshaping global trade and growth dynamics.

Despite these challenges, the International Monetary Fund (IMF) has maintained that the overall impact on global growth in calendar year 2025 will be moderate — approximately 0.5 percentage points. This relative resilience is attributed to strong domestic demand in key economies like China, India, and Saudi Arabia.

For India, growth is projected at 6.2–6.3% for 2025 and 2026, supported by a robust domestic economy. While growth could have been stronger without the imposition of steep tariffs, several factors continue to bolster India’s momentum:

* Supportive Budget Measures: The government has injected additional spending capacity into the hands of consumers.

* GST Rationalization: Recent GST cuts have made goods more affordable, spurring higher consumption volumes.

* Easing Interest Rates: With global interest rates expected to trend lower, borrowing and investment activity are likely to improve.

India’s growth trajectory has been steady, averaging between 6.5% and 8.5% post-FY22, and remains underpinned by healthy macro fundamentals. A favorablemonsoon and improved water reserves also point towards a stronger second half of the financial year, particularly during the festive and busy season.

The resilience of the Indian economy is further reflected in its Manufacturing and Services PMI, which touched a 15–17-year high in August 2025 — signaling sustained expansion in both industrial and service sectors.

Above views are of the author and not of the website kindly read disclaimer