Power Sector Update : A good quarter led by power demand uptick by Prabhudas Liladhar Capital

Power sector performance improved in Q1FY27, with underlying demand witnessing a healthy recovery. Peak power demand increased ~12% YoY to 271GW, while energy consumption grew ~8% YoY to 484BU. Short-term prices remained soft, with DAM prices declining ~5% YoY to INR3.9/kWh, supported by higher renewable generation and comfortable coal availability. Operational performance was mixed across players: NTPC reported ~6% YoY increase in generation (after many quarters of decline), aided by higher PLF, while TPWR’s Mundra plant witnessed a marginal decline. Torrent Power (gas plant), JSW and SJVN reported weaker generation due to lower PLFs from hydro. CESC maintained stable operational performance with ~4% YoY growth in generation. On the financial front, the coverage universe (ex-Coal India) is expected to report ~7.4% YoY PAT growth, with CESC likely to deliver double-digit earnings growth, while NTPC and PWGR are expected to post stable 6–7% YoY PAT growth. Top Picks PWGR, NTPC and CESC

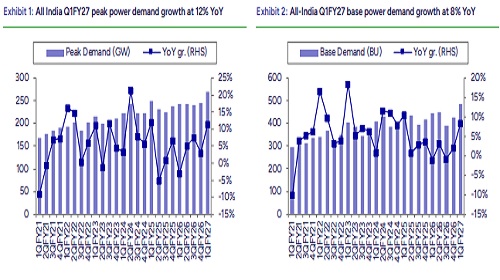

Power demand rebounds:

In Q1FY27, underlying power demand saw an uptick, with peak demand rising ~12% YoY to 271GW, indicating stronger residential activity due to the heatwave and delayed monsoon. Further, energy consumption (base demand) grew at ~8% YoY to 484BU. Power market prices continued to soften, with DAM prices declining ~5% YoY to INR3.9/kWh, driven by higher renewable generation and comfortable coal availability, which kept supply conditions benign.

Mixed operational performance:

As per CEA data for Q1FY27, NTPC reported healthy increase of ~6% YoY in generation, despite moderation in monitored capacity (~3% YoY), supported by PLF improving to 71% (vs. 65% in Q1FY26). In contrast, Tata Power Mundra reported ~1% YoY decline in generation, while Torrent Power, JSW Energy, and SJVN witnessed weaker generation, declining ~43%, ~17%, and ~41% YoY, respectively, due to lower PLF. Meanwhile, the renewables segment continued to exhibit strong momentum, with NGEL reporting ~57% YoY surge in monitored capacity, while ACME recorded ~7% YoY growth in monitored capacity. CESC maintained stable operational performance, with generation increasing ~4% YoY.

Financial performance:

We expect our coverage universe (ex-Coal India) to report 7.4% YoY increase in PAT for Q1FY27, with performance diverging across companies. On the positive side, CESC is likely to deliver double-digit PAT growth, supported by the Chandrapur plant PPA, while NTPC and PWGR are expected to report steady PAT growth of 6–7% YoY. Coal India could report ~11% increase in EBITDA led by higher offtake in the e-auction segment. Meanwhile, TPWR’s profitability is expected to be 6% YoY.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

More News

Automobiles Sector Update : Auto Sales Soar as Rain Pours by PL Capital