Pharma Sector Update : Domestic formulations to help mitigate US decline YoY by Prabhudas Lilladher Ltd

Quick Pointers

* Healthy domestic formulations, while US business declines YoY on a high base

* Strong YoY growth expected for LPC, Anthem and TRP

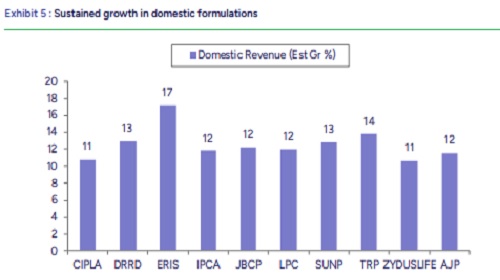

Pharmaceutical companies under our coverage are expected to see muted EBITDA growth of ~1% YoY (down ~9% QoQ) in Q4FY26. The primary drag continues to be the elevated base in the US business. However, ex gRevlimid, the core US portfolio should still post growth, suggesting that the underlying base business remains stable. From a profitability standpoint, tailwinds from currency movements will be partly offset by higher freight cost toward the end of quarter, given the Middle East conflict. The relatively benign raw material prices will continue to aid GMs in Q4. The domestic formulations business is expected to remain on a healthier side on the back of improving acute demand and continued traction in chronic therapies. Further, Q4 witnessed the launch of generic semaglutide, providing tailwind in Mar’26, and is set to accelerate growth in FY27E. Our top picks are: SUNP, AJP, IPCA and ANTHEM.

Strong EBITDA growth expected for LPC, ANTHEM and TRP: We expect these companies to report robust YoY EBITDA growth of 49%, 18% and 17%, respectively. LPC should benefit from continued traction in the US generics market, supported by niche products such as gTolvaptan, gSpiriva and gMirabegron. ANTHEM is likely to see growth driven by ramp-up of its key commercial molecules, while TRP should deliver steady performance across major markets. SUNP may report ~10% YoY revenue growth, backed by its specialty and branded formulation segments, with specialty sales likely to grow 13-15% YoY.

Healthy profitability for ERIS, JBCP and IPCA: We estimate EBITDA growth of 20%, 19% and 12% YoY, respectively. ERIS should benefit from strong domestic performance aided by market share gain in the insulin segment, while JBCP is expected to sustain steady growth in the domestic market. IPCA’s performance is likely to improve on the back of recovery in its core business. UNICHEM may continue to see subdued profitability, whereas AJP’s EBITDA growth is expected to remain muted at 9% YoY given the Middle East conflict. Overall, AJP could see Rs300-400mn revenue impact in Q4 given the delay in shipments to the Middle East.

Weak Q4FY26 anticipated for CIPLA, ZYDUS and DRRD: We expect a significant YoY decline in EBITDA for these companies, due to a high US base and margin pressure from an unfavorable product mix.

Margins on upward trajectory across LPC, JBCP and IPCA: These companies are likely to witness YoY margin expansion driven by improved product mix and consolidation of new businesses. In contrast, CIPLA, ZYDUS and DRRD may face margin pressure due to erosion in gRevlimid sales, while SUNP’s margins could remain steady YoY.

US sales display mixed trend: US revenue for our coverage universe is expected to decline QoQ in constant currency terms, largely due to a higher base of gRevlimid sales. Excluding gRevlimid, the underlying business is likely to show growth. LPC should outperform with strong gTolvaptan traction, while AJP’s US revenue is expected to decline QoQ given lower Tamiflu sales. Meanwhile, CIPLA and DRRD may report US sales decline of 22% and 29% YoY, respectively, due to lower gRevlimid contribution. CIPLA is also facing issues in gLanreotide supply.

Healthcare Index outperforms Sensex; favorable outlook: During Jan–Mar’26, the Healthcare Index outperformed the Sensex by ~12%, given investor sentiment was influenced by the Middle East conflict. Fundamentally, the sector continues to benefit from stable pricing dynamics, resilient domestic demand, currency tailwinds from INR depreciation, and relatively benign input costs. The near-term profitability may be impacted due to rising oil prices and freight cost. However, earnings growth should gradually improve, supported by strong traction in domestic formulations, increasing contribution from US specialty and differentiated products, and better operating leverage. Overall, we remain constructive on the sector, with a preference for companies having strong India franchises and clearer visibility in the US market. Our top picks are: SUNP, AJP, IPCA and ANTHEM.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Consumer Durables Sector Update : GST rate cuts a booster dose By JM Financial Service Ltd