Non-Life Premium Growth Remains Lacklustre in July 2025 by CareEdge Ratings

Overview

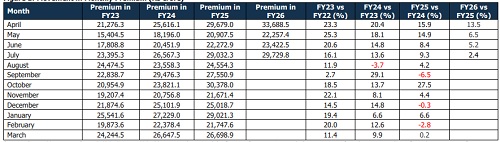

In July 2025, the non-life insurance sector experienced a slowdown in premium growth, with collections totalling Rs 29,729.8 crore- a mere 2.4% increase yearon-year (y-o-y), compared to a 9.3% rise in July 2024. The transition to the 1/n rule weighed on overall performance, coupled with a slowdown in health insurance growth to single digits and reduced momentum in the passenger vehicle (PV) segment. Nonetheless, renewals in commercial lines have provided some cushion.

Figure 1: Movement in Monthly Premium (Rs crore)

Figure 2: Movement in Gross Direct Premium Underwritten (Rs crore)

* In July 2025, public sector general insurers sustained their faster growth rate for the tenth month in a row, mainly fueled by renewals in fire, engineering, health, and motor TP segments. Nonetheless, the shift to the 1/n rule has impacted overall headline growth. Meanwhile, private non-life insurers still hold half of the market share.

* Specialised insurers recorded a rise of 49.2% y-o-y in premiums in July 2025, slightly elevated compared to July 2024’s 48.3% increase. The segment has returned to growth for the year-to-date (YTD) period, rising by 27.5% compared to 13.5% in YTDFY25.

* Standalone Health Insurers (SAHIs) experienced a notable slowdown in growth, with premiums increasing by 10.4% year-over-year in July 2025- less than half the growth rate from the previous year. This deceleration may be due to various factors, such as rising premiums, normalisation of retail health demand, a shift towards group health insurance, and the influence of IRDAI’s Bima Trinity initiative. Despite this, SAHIs continue to gain market share, mainly at the expense of private general insurers.

Figure 3: Movement in Health Premiums (Rs crore)

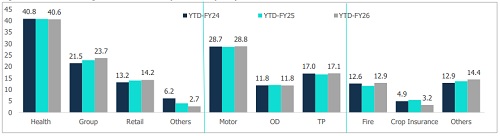

* Health insurance continues to be the largest segment within the non-life insurance industry, though overall growth has moderated due to the 1/n rule and affordability issues from higher premiums. Within the segment, SAHIs have consistently outperformed, while public sector health insurers continue to trail their private counterparts.

* The group health segment grew the fastest in YTDFY26, driven by policy renewals and premium hikes amid rising medical inflation. However, growth moderated to 11.4%, down from a robust 19.0% in the same period last year.

* Retail health insurance growth moderated to 9.1% in YTDFY26, down from the pace seen in YTDFY25. The deceleration is partly linked to the 1/n rule and further exacerbated by rising medical inflation, which has pushed premiums higher and weighed on affordability.

* SAHIs remain concentrated in the retail segment, whereas general insurers continue to dominate the group business. With new SAHIs set to enter the market, competitive intensity is expected to rise over the medium term.

* Others, which include government schemes and overseas medical, recorded a 42.5% y-o-y decline in July 2025, primarily due to the lumpiness in premium booking under government schemes and weaker demand for overseas medical policies. A high base effect further accentuated the fall.

Figure 4: Movement in Non-Life Premiums excluding Health Premiums (Rs crore)

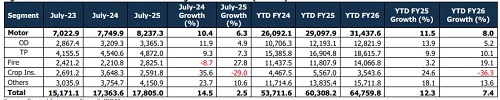

* The growth of the non-life insurance industry, excluding health, stood at 2.5% as of July 25, compared to the 2.8% level if health is included in the analysis. Furthermore, a sizable proportion of this 2.5% growth was attributed to the motor and fire segments, which accounted for over 70% of the non-life insurance excluding health.

* Motor OD grew by 5.2% in YTDFY26 (vs. 13.9% for YTDFY25), and motor TP rose by 10.1% (vs. 9.9% for YTDFY25). Muted PV sales have contributed to lukewarm motor OD growth, whereas the motor TP segment has grown at a better rate. Additionally, the Ministry of Road Transport and Highways (MoRTH) is evaluating a proposed upward revision in motor TP insurance premiums, following a recommendation from IRDAI, which could support the growth in the motor TP segment while aiding insurers in improving profitability.

* The fire insurance segment continued to grow, increasing by 19.1% YTDFY26, a sharp rise from 3.2% in the same period last year. Meanwhile, the engineering segment grew by 16.8%, up from 4.8% in YTDFY25. Conversely, crop insurance saw a major decline of 29.0%, contrasted with a 35.6% growth previously YTDFY25.

* The other segment recorded a growth of 10.6% in YTDFY26, propelled by a significant 25.9% rise in personal accident premiums, reflecting heightened awareness of individual risk protection and higher group policy issuances. Steady gains were also observed in engineering and credit guarantee premiums, supported by infrastructure expansion and increased MSME credit risk coverage, respectively.

Figure 5: Movement in Segment Market Share by Premiums (In %)

CareEdge Ratings View

“In July 2025, the non-life insurance industry reported premiums of Rs 29,729.8 crore, reflecting a muted 2.4% year-on-year growth, significantly lower than the 9.3% recorded in July 2024. The transition to the 1/n rule, a slowdown in health, and muted PV growth weighed on overall performance. However, renewals in the fire and engineering segments provided some support,” said Saurabh Bhalerao, Associate Director, CareEdge Ratings.

“Non-life insurance premiums surpassed the Rs 3 lakh crore milestone in FY25, supported by enabling regulations, rapid Insurtech adoption, accelerating digitalisation, and a growing middle class. The government’s Bima Trinity initiative is poised to catalyse the next phase of sectoral expansion. Standalone health insurers are expected to retain their leadership in the retail health space, underpinned by consumer demand and deep distribution reach. In contrast, the trajectory of motor insurance will remain intrinsically linked to trends in vehicle sales and the anticipated revisions in third-party tariffs. Meanwhile, the proposed rollout of composite licences carries the potential to significantly reshape the competitive dynamics of the industry over the medium term. Nonetheless, intensifying competition and evolving global geopolitical risks will be key factors to monitor,” said Priyesh Ruparelia, Director, CareEdge Ratings.

Above views are of the author and not of the website kindly read disclaimer