Neutral Tata Motors Ltd for the Target Rs. 687 by Motilal Oswal Financial Services Ltd

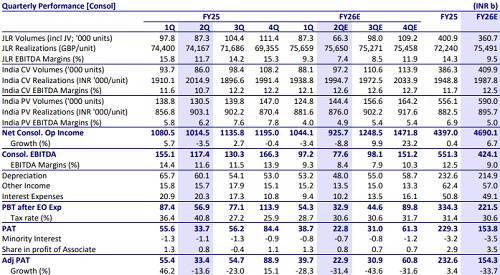

* India PV volumes rose 10.5% YoY. India CV volumes grew 12% YoY for 2Q.

* India PV margins are likely to pick up QoQ due to improved volumes partially offset by high discounts. We expect margins at 4.9% (-130bp YoY). India CV margins to improve 50bp QoQ and 190bp YoY to 12.6%.

* JLR volumes to be impacted by the cyberattack that led to production shutdown in Sep. While retails unlikely to be hit materially, wholesale volumes may fall 24% YoY.

* EBITDA margin is likely to contract ~190bp QoQ to 7.4%.

* The record date for demerger for PV (India + JLR) business is 14th Oct’25.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412