Neutral Sun TV Network Ltd for the Target Rs 575 by Motilal Oswal Financial Services Ltd

Subdued end to FY26; ad revenue likely to remain muted

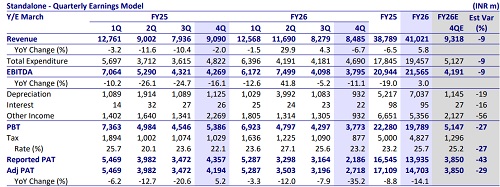

* SUN TV reported a weak 4QFY26, with ad revenue declining 10% YoY, amid cuts in ad spends on linear TV from the FMCG players. This resulted in ~11%/9%/38% YoY decline in EBITDA/EBIT/PAT for the quarter.

* For FY26, SUN TV reported ~11% YoY decline in ad revenue, which was partly offset by ~10% YoY growth in domestic subscription revenue and higher collection from Movie (Coolie). However, profitability moderated with ~11%/19% YoY dip in EBIT/PAT.

* The recent transactions for IPL teams (RCB and RR) are sentimentally positive for SUN TV. However, we believe IPL teams' valuations are stretched and could correct meaningfully with the lack of competition for media rights in the upcoming renewals (applicable from FY29).

* We tweak our estimates for FY26 actuals. We expect SUN TV to deliver a CAGR of 4%/3%/9% in revenue/EBITDA/adj. PAT over FY26-28E, as weaker ad revenue continues to weigh.

* At ~12.6x one-year forward P/E and with a significant cash cushion (of ~INR62b), valuations are undemanding; however, improvement in ad revenue in the core business remains key for re-rating.

* We value SUN TV on an SoTP basis: 9x FY28 EV/sales for SunRisers Hyderabad, ~4x EV/EBITDA for the core TV business, 0.5x investments for Northern Superchargers, and 1x for cash/dividends (~INR 81b), to arrive at our revised TP of INR575 (implying ~13x FY28E P/E). Reiterate Neutral.

Valuation and view

* Shift in FMCG ad spending towards digital platforms remains a key structural headwind for linear TV broadcasters such as Sun TV Network over the medium term. A sustained recovery in ad revenues remains the key trigger for any meaningful re-rating.

* The recent transactions for IPL teams (RCB and RR) are sentimentally positive for SUN TV. However, we believe IPL teams' valuations are stretched and could correct meaningfully with the lack of competition for media rights in the upcoming renewals (applicable from FY29 onwards).

* We tweak our estimates for FY26 actuals. We expect SUN TV to deliver a CAGR of 4%/3%/9% in revenue/EBITDA/adj. PAT over FY26-28E, as weaker ad revenue continues to weigh.

* At ~12.6x one-year forward P/E, and significant cash cushion (~INR62b), valuations are undemanding; however, improvement in ad revenue in the core business remains key for re-rating.

* We value SUN TV on an SoTP basis: 9x FY28 EV/sales for SunRisers Hyderabad, ~4x EV/EBITDA for the core TV business, 0.5x investments for Northern Superchargers, and 1x for cash/dividends (~INR 81b), to arrive at our revised TP of INR575 (implying ~13x FY28E P/E). We reiterate our Neutral rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412