Neutral Siemens Ltd For Target Rs.3,500 Motilal Oswal Financial services Ltd

Forex and RM volatility play spoilsport

Siemens’ results for the quarter and full year stood largely in line with our estimates, adjusted for the sale of the LVM business. Margin performance was hit by a steep RM price inflation and rupee depreciation, and with the short cycle nature of the contracts, these could not be passed on to the end users despite price hikes taken twice during the year by the company in select segments. Order inflow has ramped up in the last two quarters, and the overall order book grew 9% for 18MFY26. This is also supported by a large order from the parent for the mobility division. The company is experiencing a strong demand outlook across segments, particularly data centers, electrification, and private capex. Going ahead, we expect Siemens to benefit from 1) improvement in order inflows for smart infra and digital industries and 2) locomotive delivery ramp-up in the mobility segment, thereby driving operating leverage. However, we expect forex and currency volatility to affect its margin performance for a few more quarters despite likely improvement in the smart infrastructure segment over the medium to long term. We revise our estimates by -1%/+4% for FY27/28 and revise our TP to INR3500 based on 45x P/E two-year forward earnings. Reiterate Neutral.

In-line revenue/PAT, a miss on EBITDA

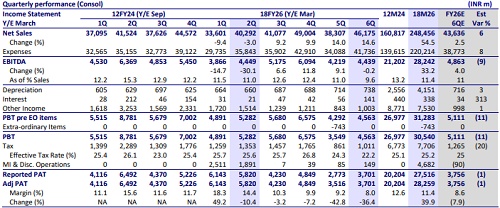

Siemens reported 6QFY26 results with revenue and PAT broadly in line with our estimates, while EBITDA came in below expectations. Revenue grew 15% YoY to INR46b (excluding the LVM business). Gross margin came in at 26.2% (vs. our est. of 28.8%), resulting in a dip in EBITDA margin to 9.6% (vs. our est. of 11.1%) due to higher commodity costs, INR depreciation, and elevated other expenses. Despite margin pressure, PAT remained broadly in line with estimates, aided by a lower tax rate, though it declined 9% YoY to INR3.7b. Order inflow remained strong, rising 33% YoY to INR67b, resulting in a 9% increase in the order book to INR450b. For 18MFY26, revenue/EBITDA/PAT stood at INR248b/INR28b/INR28b vs. INR161b/INR21b/INR20b for 12MFY24, while OCF/FCF saw an outflow of INR5b/INR11b compared to an inflow of INR17b/INR16b in 12MFY24.

Smart infra outlook strong; margins affected

Smart infra continued to deliver strong momentum, with order inflow rising 18% YoY to INR30b in 6QFY26, driven by power utilities, renewables, and data centers, while revenue grew 15% YoY to INR26b, led by electrification, automation, and electrical products. EBIT margin contracted 410bp to 11.1% in 6QFY26 due to elevated commodity prices, particularly copper, silver, and aluminum, while forex impact was relatively lower given ~70-75% localization in the business. The company has undertaken two rounds of price hikes across low-voltage products, while medium-voltage and project businesses continue to negotiate pricing on an order-by-order basis to offset input cost inflation. We expect growth momentum to remain healthy, supported by continued investments and healthy ordering activity

Financial outlook and valuation

We revise our estimates by -1%/+4% for FY27/28 to factor in 6QFY26 performance and now expect a CAGR of 16%/25%/26% in revenue/EBITDA/PAT over 12MFY26-FY28. The stock is currently trading at 66.6x/53.6x P/E on FY27/28E earnings. We reiterate our Neutral rating on the stock with a revised TP of INR3,500 (vs. INR3,150 earlier), based on 45x two-year forward earnings.

Key risks and concerns Key risks:

1) A slowdown in order inflows from key government-focused segments,

2) Aggression in bids to procure large-sized projects would adversely impact margins

3) Related-party transactions with parent group entities at lower-than-market valuations would weigh on the stock performance

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041