Neutral Ramco Cements Ltd for the Target Rs 950 by Motilal Oswal Financial Services Ltd

EBITDA below estimate due to higher opex/t Demand outlook healthy; cost pressure to weigh on margin

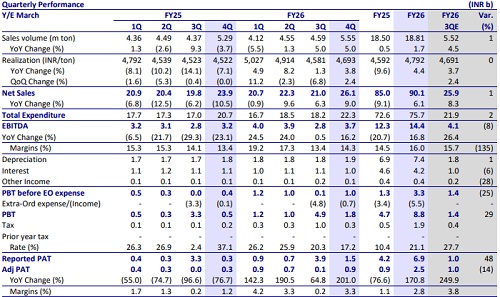

* The Ramco Cements’ (TRCL) 4QFY26 EBITDA grew 16% YoY to INR3.7b (8% miss due to higher-than-estimated opex/t). EBITDA/t was up ~11% YoY at INR671 (est. INR734). OPM surged 90bp YoY to ~14% (vs. our est. of ~16%). PAT (adj. for profit on sale of non-core assets and impact of labor code) jumped 3x YoY to INR850m (~14% miss).

* Cement demand is estimated to grow 6-7% YoY in FY27. Though prices have increased in Apr’26, it expects pricing to remain under pressure amid rising capacity and competitive intensity. High prices of pet coke, gypsum, polymer, and diesel are likely to increase opex/t materially, with partial impact visible from 1QFY27 and full impact from 2QFY27 onward, which could weigh on margin. Over the past two years, the company monetized non-core assets worth INR11.0b. It is expected to monetize the remaining identified non-core assets worth INR1.5b in the near term.

* We cut our EBITDA estimates by ~6% for FY27 (due to cost pressure) while maintaining FY28 estimates. The stock is currently trading at 15x/13x FY27E/FY28E EV/EBITDA. We value the stock at 13x FY28E EV/EBITDA to arrive at a TP of INR950. Reiterate Neutral.

Total volume rises ~5% YoY; realization/t up 4% YoY/2% QoQ (in line)

* Revenue/EBITDA/adj. PAT stood at INR26.1b/INR3.7b/INR1.5b (+9%/+16%/ +3x YoY and +1%/-8%/-14% vs. our estimates) in 4Q. Sales volume grew ~5% YoY to 5.6mt (in line). Realization/t was up 4% YoY/2% QoQ at INR4,693/t.

* Opex/t was up 3% YoY (2% above our estimate), led by 5%/1% increase in variable/freight, while other expenses/t fell ~6% YoY. OPM rose 90bp YoY to ~14% and EBITDA/t grew ~11% YoY to INR671. Depreciation increased ~3% YoY, while interest costs declined 16% YoY. Other income was down ~6% YoY.

* In FY26, revenue/EBITDA/adj. PAT stood at INR90.1b/INR14.4b/INR2.5b (up ~6%/17%/2.7x YoY). OPM surged 1.5pp YoY to ~16%. Sales volume grew 2% YoY and realization/t rose ~4% YoY. EBITDA/t grew ~15% YoY to INR765. CFO stood at INR16.1b vs. INR14.0b in FY25. Capex stood at INR10.0b vs. INR10.2b in FY25. FCF stood at INR6.1b vs. INR3.8b in FY25.

View and valuation

* TRCL’s operating performance was below our estimates due to higher-thanestimated opex/t. The company’s variable cost/t has increased significantly, partly offset by lower other expenses/t. The lagged impact of higher input costs is estimated to compress margins over the next few quarters. Recent price hikes offer some support, but sustained improvement remains contingent on better pricing in the longer term.

* We estimate a CAGR of ~8%/15%/57% in revenue/EBITDA/PAT over FY26-28. Net debt declined to INR36.6b in FY26 from INR44.8b in FY25. The net debt-toEBITDA ratio improved to 2.5x in FY26 from 3.5x in FY25. We estimate its net debt to further decline to INR26.4b by FY28E (net debt-to-EBITDA ratio at 1.4x), led by further non-core asset monetization and disciplined capex.

* The stock is currently trading fairly at 15x/13x FY27E/FY28E EV/EBITDA. We value the stock at 13x FY28E EV/EBITDA to arrive at our TP of INR950. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412