Neutral Dabur Ltd for the Target Rs. 475 by Motilal Oswal Financial Services Ltd

Steady show; HPC outperformance sustains

* Dabur’s (DABUR) consolidated revenue grew ~7% YoY (flat base), with India business revenue up 10% YoY. Demand recovery was noted in steady double-digit growth in HPC in 2HFY26. India volume grew 6% (est: 4%, 3% in 3Q). Demand condition in India remained steady; however, unseasonal rains in March impacted its summer portfolio (glucose, nectars etc.). Rural markets continued to outpace urban consumption by ~350bp. Going ahead, management expects 4Q growth momentum to continue in HPC and healthcare (excl. glucose).

* Home & personal care continued to drive growth, with revenue up 17%, backed by hair care and home care. The healthcare portfolio posted ~4% growth. F&B grew 3% YoY. Management has revised its India business revenue guidance from high single digits to low double digits, anticipating growth from both volume and pricing (largely equal split) for FY27.

* GM expanded 160bp YoY to 48.3% (est: 47.1%), while EBITDA margin remained flat YoY at 15.2% (in line). Amid geopolitical tensions, Dabur is seeing cost inflation of ~10%, and to offset this, the company has taken ~4% price hike. Management remains open to further pricing action depending on RM prices. Dabur aspires to improve operating margins by mitigating inflation through price increases, premiumization, and costsaving initiatives. We build in a modest margin expansion and expect EBITDA margin to be ~19% for FY27/FY28E.

* Dabur expects double-digit growth across its business verticals in FY27, along with margin improvement. Management expects a healthy mix of volume and value going ahead. Dabur’s performance is quite sensitive to macro recovery, particularly rural demand. General macro inflation and monsoon will be key monitorable for its FY27 performance. We reiterate our Neutral rating on the stock with a TP of INR475 (based on 35x Mar’28E EPS).

In-line EBITDA; HPC continues to lead growth

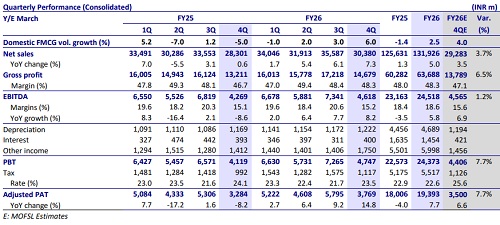

* Improved India growth; positive commentary for FY27: 4Q consolidated sales grew 7% (est:3.5%) to INR30.4b (est. INR29.3b). India business revenue grew 10% YoY. India business volume grew 6%. (est. 4%).

* HPC business up ~17% YoY on negative 3% base: HPC continued its healthy performance trajectory in 4Q, aided by broad-based performance across categories and a favorable base (-3% in 4QFY25). Hair Care portfolio grew by ~27% (-5% in base) during the quarter, led by 28% growth in Hair Oils business. Home care grew in mid-twenties, backed by strong growth in Odonil. The toothpaste category was up ~7% YoY, leading to oral care growth of mid-single digit. Skin & Salon business grew by over 12%.

* Healthcare portfolio up ~4% YoY: Health supplements grew 2.2% YoY (3.6% - excl. the impact of discontinued brands – Baby Super Pants and Vedic Tea). Dabur honey grew in twenties, while Dabur Glucose sales were impacted by unseasonal rains in Mar’26. This led to health supplements revenue declining in mid-single digits. Digestives business grew 15% YoY and OTC & Ethicals grew in double digits.

* Foods and beverages grew ~3% YoY: The Culinary portfolio accelerated its growth momentum during the quarter and reported growth in twenties with broad-based growth across brands. Beverage portfolio witnessed a sequential recovery in 4Q. In beverages, Real active and coconut water are doing exceedingly well, while nectar was impacted by rains. Premium beverage portfolio continued to outperform the category. Badshah business performed well, with domestic growth in double digits (+12%).

* Despite facing headwinds in the Middle East, international business grew by 2.5% (INR terms) during the quarter, led by Sub-Saharan Africa (20%), UK & EU {10%); Namaste US (6.2%) and Bangladesh (22%).

* Flat EBITDA margin: Gross margin expanded 160bp YoY (flat QoQ) to 48.3% (est. 47.1%). Employee expenses rose 15% (-7% in base), ad spends grew 22% and other expenses rose 7% YoY. EBITDA margin expanded 10bp YoY to 15% (est. 15.6%).

* High other income leads to profitability beat: EBITDA grew 8% (on 8% decline in base) to INR4.6b (est. INR4.6b) and APAT grew by 15% YoY (on 8% decline in base) to INR3.8b (est. INR3.5b). Beat on APAT was on account of higher-thanexpected other income.

* In FY26, net sales, EBITDA, and APAT grew 5%, 6% and 8%, respectively.

Highlights from the management commentary

* Demand condition in India remained steady, though unseasonal rains in Mar’26 impacted summer portfolio business. Dabur’s India business grew 9.5% YoY, while the FMCG sector saw 9.2% growth as per Dabur.

* Dabur is seeing inflation of ~10%, and to offset this, Dabur has taken ~4% price hike at company level. Packaging material constitutes one-third of the raw material basket, and its costs have increased due to rising crude prices.

* Management revised India business revenue guidance from high single-digits to low double-digits, anticipating growth from both volume and pricing (largely equal split) for FY27.

Valuation and view

* We largely maintain our EPS estimates for FY27E and FY28E.

* The company has been witnessing muted sales growth over the past two years. After delivering 1.3% growth in FY25, revenue growth improved modestly to 5% in FY26. Management has revised India business revenue guidance from high single-digit to low double-digit, anticipating growth from both volume and pricing (largely equal split) for FY27.

* While we remain positive on India consumption, DABUR’s historical weak execution remains concerning to us. General macro inflation and monsoon will be key monitorable for its FY27 performance. We reiterate our Neutral rating on the stock with a TP of INR475 (based on 35x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041