Neutral Axis Bank Ltd for the Target Rs. 1,475 by Motilal Oswal Financial Services Ltd

Core performance healthy; Tax reversals utilized to strengthen provisioning buffer; Asset quality ratio improves

Slippages dip, and the asset quality ratio improves

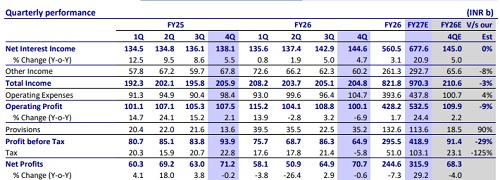

* Axis Bank (AXSB) reported a 4QFY26 net profit of INR70.7b (flat YoY, up 9% QoQ; in line), as the bank utilized one-off gains from tax reversals to strengthen its standard asset provisioning buffer.

* NII grew 4.7% YoY/1.2% QoQ to INR144.6b (in line). NIM dipped 2bp QoQ to 3.62% (vs. our est. of 3.58%).

* AXSB has made standard asset provisions of INR20b against the tax reversal of INR21.9b and now holds INR154b of total standard provisioning.

* The loan book grew at a healthy rate of 18.5% YoY/6.4% QoQ, amid robust growth in corporate (up 10% QoQ) and steady growth in SME (up 5.6% QoQ) and retail (up 4.5% QoQ).

* Fresh slippages declined to INR47.1b (down 2% YoY/22% QoQ), of which the technical impact was INR12.4b. Net slippages were INR20.1b vs. INR31.4b in 3QFY26. GNPA/NNPA ratios dipped 17bp/5bp QoQ to 1.23%/0.37%. PCR thus stood flat at 70.2%.

* We raise our FY27/28E earnings by ~4% each and estimate FY27E RoA/RoE at 1.6%/14.6%. Reiterate Neutral with a TP of INR1,475 (based on 1.7x Sep’27E ABV).

Business growth robust; the through-cycle NIM guidance at 3.8%

* AXSB’s 4Q PAT was INR70.7b (up 9% QoQ; in line). NII grew 1.2% QoQ (up 4.7% YoY) to INR144.6b (in line). NIM contracted 2bp QoQ to 3.62% (vs. MOFSLe: 3.58%).

* Other income fell 3% QoQ to INR60.2b (8% miss), as AXSB incurred a treasury loss of INR6.1b. Thus, total revenue was INR205b (down 0.5% YoY/flat QoQ).

* Opex grew 6.4% YoY (up 8.6% QoQ, 4% ahead of MOFSLe), amid INR1.2b impact due to rate movement. PPoP declined 7% YoY/down 8% QoQ to INR100.1b (9% miss, amid lower other income and higher opex). The C/I ratio thus inched up to 51% (up 413bp QoQ).

* The loan book surged 18.5% YoY/6.4% QoQ, with retail loans growing 8.1% YoY/4.5% QoQ. The corporate book jumped 37.9% YoY/10.1% QoQ, and SME rose 24% YoY/5.6% QoQ.

* Deposits grew 13.9% YoY/6% QoQ. As a result, the C/D ratio inched up to 92.3% (up 41bp QoQ). CASA mix thus improved to 40%.

* Fresh slippages declined to INR47.1b (down 2% YoY/22% QoQ), of which the technical impact stood at INR12.4b. Net slippages were INR20.1b vs. INR31.4b in 3QFY26. GNPA/NNPA ratios dipped 17bp/5bp QoQ to 1.23%/0.37%. PCR thus stood flat at 70.2%.

* With slippages declining and the technical impact easing, the MFI and unsecured segments have also witnessed some growth. The bank expects momentum in high-yielding assets to sustain, supporting its through-cycle NIM guidance of ~3.8%, while credit costs are also expected to moderate as operating conditions improve.

* The CAR/CET-1 stood at 16.42%/14.4%. The average LCR was 117%. The increase in RWA was lower than the loan growth in 4QFY26.

Highlights from the management commentary

* From a product mix perspective, the bank expects 70% of retail book and 30% of wholesale. AXSB has a 3.8% NIM target and will not shy away from the same.

* Technical slippages are expected to decline through the year, with no anticipated economic loss from the portfolio.

* The repo rate cut of 25bp and 61% of the book have been fully repriced. 4Q had the full impact of the repo rate cut. The MCLR and EBLR will be passed on as per their timeliness.

* AXSB maintains a through-cycle NIM of 3.8% and is 15-18 months away from the last rate cut.

* The bank holds identified stressed exposures and has built provisions that can be utilized in case of adverse developments.

Valuation and view

AXSB reported an inline quarter, with standard asset provisions of INR20b largely offset by a tax reversal of INR21.9b. NIM declined marginally by 2bp QoQ to 3.62% (vs. MOFSLe of 3.58%), with the bank reiterating its through-cycle NIM guidance of ~3.8%. Credit costs declined, supported by easing stress in the unsecured portfolio, which also drove improved traction in higher-yielding assets along with lower interest reversals. Business growth remained robust, aided by a pickup in deposits, resulting in a moderation in the CD ratio. The bank continues to target medium-term loan growth of ~300bp above industry levels. Asset quality improved sequentially, with a dip in both GNPA and NNPA ratios. However, the evolving West Asia situation remains a key near-term monitorable, for which the bank has prudently created standard asset provisions of INR20b. We raise our FY27/28E earnings by ~4% each and estimate FY27E RoA/RoE of 1.6%/14.6%. Retain Neutral with a TP of INR1,475 (1.7x Sep’27E ABV + STOP of INR148).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412