Neutral Asian Paints Ltd For Target Rs. 2,750 by Motilal Oswal Financial Services Ltd

Beat on performance; watchful of FY27 margins

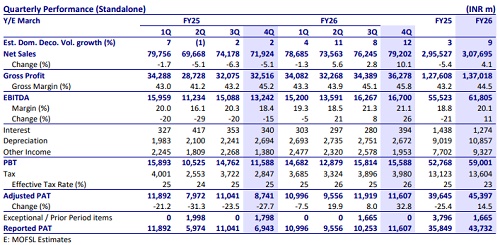

* Asian Paints (APNT) reported 11% YoY consolidated revenue growth in 4QFY26 (base: -4%, FY26 at 5%), while standalone revenue grew 10% YoY. Domestic decorative volumes rose 12% YoY (est. 9%), supported by healthy double-digit demand across Jan-Mar’26. Management indicated that Mar’26 growth benefited by 3–4% due to channel up-stocking ahead of price hikes. Higher revenue growth led to an overall profitability beat. Some inventory build-up is expected in 1QFY27 as well. International business grew 11% YoY (+8.2% CC growth).

* Gross margin expanded 90bp YoY to 44.8% (est. 44.3%), aided by sourcing efficiencies and lower raw material costs. Management highlighted that cumulative inflation, including INR depreciation, stands at ~20%, against which the company has taken a 10–11% price hike so far. Further calibrated price hikes are likely. EBITDA margin expanded 210bp YoY to 19.3% (est. 18.5%, 18.8% in FY26), resulting in EBITDA growth of 24% YoY to INR17.9b (est. INR16.2b).

* Management expects high single-digit volume growth in FY27 despite steep pricing, driven by a favorable base, El Nino resulting in more painting days, and the extended festive season. We model 7% volume and 16% standalone revenue growth for FY27. Management maintains EBITDA margin guidance of 18-20%, supported by premiumization, cost efficiencies, and backward integration benefits. We model 19.1%/19.5% for standalone and 18.2%/18.6% for consolidated EBITDA margin for FY27 and FY28.

* Given the volatile geopolitical backdrop, inflationary pressures are likely to remain elevated and could weigh on overall demand conditions. Price hikes are changing the P&L structure, and revenue growth print is likely to remain strong with a double-digit price hike. However, input cost inflation and stiff competition are expected to weigh on the operating margin. Paint demand has been muted over the last two years, and recent price hikes are expected to further delay demand recovery in FY27. The company is focusing on product innovation, brand salience, regionalization, and execution excellence to negate competitive pressure. We value the company at 45x FY28E EPS to derive a TP of INR2,750. We reiterate a Neutral rating.

Superior growth print; domestic volume rises 12%

* Double-digit revenue growth: APNT reported consolidated net sales growth of 10.6% YoY to INR92.5b (est. INR87.5b). The Decorative business (India) clocked volume growth of 12% (est. 9%, 8% in 3QFY26) and revenue growth of 10%. The Industrial segment clocked high-teen growth (+18% YoY). The Bath business rose 4%, and the Kitchen business revenue grew 17%. The White Teak business witnessed 16% revenue growth, while Weather Seal revenue rose 25%.

* International saw healthy growth: International business registered a value growth of 11% (8.2% growth in CC terms), backed by steady performance in key markets of Sri Lanka, Egypt, and the UAE. Despite impact from the West Asia conflict, Middle East operations delivered resilient performance.

* Better margin delivery: Gross margins expanded 90bp YoY to 44.8% (est. 44.3%). GP grew 13% YoY to INR41.4b (est. INR38.7b). Employee expenses rose 14% YoY, while other expenses increased by a mere 2% YoY. EBITDA margin expanded 210bp YoY to 19.3% (est. 18.5%).

* Robust growth in profitability: EBITDA grew 24% YoY to INR17.9b (est. INR16.2b). PBT grew 34% YoY to INR15.9b (est. INR14.6b). Adj. PAT grew 34% YoY to INR11.7b (est. INR10.8b).

* Revenue/EBITDA/APAT grew 5%/11%/11% YoY in FY26.

Key highlights from the management commentary

* Management guided for high single-digit volume growth in FY27, supported by stable demand conditions, festive season tailwinds, and healthy rural recovery.

* Management indicated that the total inflationary impact, including rupee depreciation, is significantly higher at ~20%, while the company has so far undertaken cumulative price hikes of 10.5–11%.

* Management indicated that competitive intensity in the Paints industry remains elevated and is expected to continue its momentum going forward. Competitive activity continues to be driven primarily by higher dealer discounts, contractor incentives, and channel schemes rather than headline pricing differences.

* The company remains focused on maintaining its long-term EBITDA margin guidance of 18–20% through a combination of calibrated pricing, premiumization, cost efficiencies, and backward integration benefits.

Valuation and view

* We increase our EPS estimates by 3%-4% for FY27 and FY28 on the better delivery of revenue.

* Given the volatile geopolitical backdrop, inflationary pressures are likely to remain elevated and could weigh on overall demand conditions. Management expects high single-digit volume growth in FY27 despite steep pricing, driven by a favorable base, El Nino resulting in more painting days, and the extended festive season. We model 7% volume and 16% standalone revenue growth for FY27. Management maintains EBITDA margin guidance of 18-20%, supported by premiumization, cost efficiencies, and backward integration benefits. We model 19.1%/19.5% for standalone and 18.2%/18.6% for consolidated EBITDA margin for FY27 and FY28.

* Paint demand has remained muted over the last two years, and recent price hikes are expected to further delay demand recovery in FY27. The company is focusing on product innovation, brand salience, regionalization, and execution excellence to negate competitive pressure. We value the company at 45x FY28E EPS to derive a TP of INR2,750. We reiterate our Neutral rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

2.jpg)