Neutral Amara Raja Ltd for the Target Rs 878 by Motilal Oswal Financial Services Ltd

Cost pressures to hurt near-term margins Earmarks fresh investments for the BESS opportunity

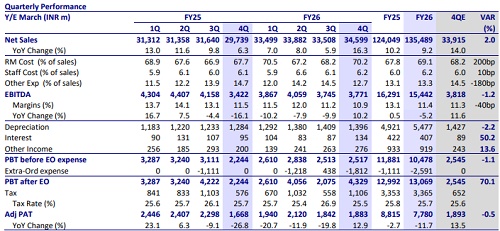

* Amara Raja’s (AMRJ) 4QFY26 Adj PAT at INR1.8b came in line with our estimates. The company has recently taken a 5-6% price hike in the lead acid business to pass on input cost pressure.

* The lead acid business is expected to witness near-term margin pressure given the sharp surge in input costs. Further, while the market is optimistic about AMRJ’s Li-ion initiative, we are cautious about its potential returns. We believe the stock, trading at around 20.9x FY27E/17x FY28E EPS, appears fairly valued. We reiterate our Neutral rating with a TP of INR878, based on 15x standalone FY28E EPS and INR92/sh value of the investment in the New Energy business.

Valuation and view

* AMRJ’s venture into the lithium-ion business appears strategically sound, given the opportunities in the segment and the evolving risks in its core business. However, there are notable challenges:

1) Market opportunities are limited by existing OEM partnerships

2) The low-margin nature of the lithium-ion business is likely to dilute returns

3) The long-term viability of the technology remains uncertain despite the large capital investment.

* The lead acid business is expected to witness near-term margin pressure, given the sharp surge in input costs. Further, while the market is optimistic about AMRJ’s Li-ion initiative, we are cautious about its potential returns. We believe the stock, trading at around 20.9x FY27E/17x FY28E EPS, appears fairly valued. We reiterate our Neutral rating with a TP of INR878, based on 15x standalone FY28E EPS and INR92/sh value of the investment in the New Energy business.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412