2025-10-15 05:50:29 pm | Source: Motilal Oswal Financial Services Ltd

Neutral Amara Raja Energy Mobility Ltd for the Target Rs. 1,039 by Motilal Oswal Financial Services Ltd

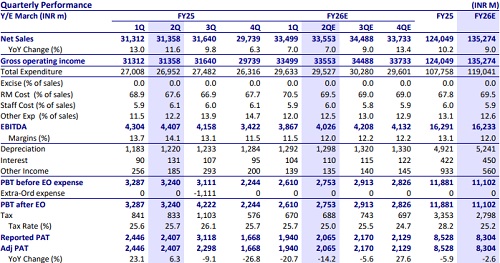

* We expect battery demand to largely remain stable QoQ both in OE and replacement segments, and hence expect Amara to post 7% YoY growth in revenue (flat QoQ).

* Lead prices are largely stable QoQ. However, elevated power costs are likely to keep margins under pressure for at least 2Q.

* EBITDA margins to improve 50bp QoQ (down 210bp YoY) to 12%.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

FASTag annual pass crosses 25 lakh users with over 5...

Employment rate rises to 5-month high in September

IMF`s GDP upgrade reaffirms India?s robust growth st...

CII, Gati Shakti Vishwavidyalaya sign MoU to develop...

Axis Bank`s Q2 net profit falls 25 pc to Rs 5,557.5 ...

Buy Tube Investments Ltd for the Target Rs. 3,716 by...

Brazil VP Geraldo Alckmin arrives in India for trade...

Esha Deol remembers late Pankaj Dheer, calls him "wo...

Buy Samvardhana Motherson Sumi Ltd for the Target Rs...

Buy Motherson Wiring India Ltd for the Target Rs. 53...