MPC Preview : Policy Status Quo Expected ; External Risks in Focus by CareEdge Ratings

The previous monetary policy announced in February was set against the backdrop of a benign inflation outlook, healthy domestic economic growth momentum, and improving external prospects, following the announcement of India’s trade deals with several major partners. However, the global economic landscape has changed dramatically since the last policy meeting, with the ongoing conflict in West Asia posing a threat to the global energy trade. International energy prices have jumped drastically, with prices of Brent crude oil and Liquefied Natural Gas (JapanKorea Marker) having shot up by 55% and 90%, respectively, since the beginning of the conflict. Furthermore, the repercussions of the worsening geopolitical situation are being felt across global commodity prices, currency movements, and the broader financial markets. Overall, the conflict has raised concerns not just about rising global energy prices but also about supply chain disruptions, with potential spillovers to growth and inflation.

Amid a highly volatile global environment, we expect the RBI to maintain the status quo on the policy repo rate and the stance, while remaining vigilant of the evolving geopolitical scenario. The ‘wait and watch’ strategy will enable the RBI to preserve flexibility to gauge the emerging risks to growth and inflation dynamics and take a calibrated call on future rate actions. The upcoming policy will also be closely watched for the RBI’s growth and inflation outlook for FY27, especially against the current backdrop of heightened external risks.

Global Tensions to Weigh on Domestic Growth & Inflation Outlook

The Indian economy is estimated to have held up relatively well in FY26, with the real GDP growth being pegged at 7.6% (Second Advance Estimate). This growth performance was supported by improved consumption and healthy momentum in investments. Policy support from income tax reductions, GST rate cuts, and continued thrust on capex-led growth bolstered the domestic consumption and investment scenario.

While domestic fundamentals remained relatively resilient in FY26, the escalation of conflict in West Asia has weakened the growth outlook, with the Indian economy likely to be affected through multiple channels. As per our baseline scenario for FY27, if the global crude oil prices average at USD 90/bbl for the full year, we estimate India’s GDP growth to moderate to 6.7%. This represents a downward revision from our pre - conflict growth forecast of 7.2% (assuming crude oil averaging between USD 60-70/bbl). Downside risks to India’s growth outlook persist, given the possibility of a prolonged war situation and higher energy prices. Looking ahead, the overall duration of the conflict and the extent of its repercussions on the global supply chains are critical monitorables.

CPI inflation edged up to 3.2% in February (Vs 2.7% in January) amid an increase in food inflation and elevated prices of precious metals. The rise in food inflation was largely anticipated as the favourable base effect from last year faded. Core inflation remained steady at 3.4% in February. Additionally, core inflation excluding precious metals was even lower at 1.9%. However, it is important to note that the February inflation print does not yet reflect the potential impact of the ongoing conflict in West Asia.

Global energy prices have jumped drastically, with prices of Brent crude oil and Liquefied Natural Gas (Japan-Korea Marker) having shot up by 55% and 90%, respectively, since the beginning of the conflict. India is dependent on imports to meet about 88% of its total oil requirement and 51% of its gas requirement. In this context, it is important to note that India’s CPI inflation has become more sensitive to retail energy prices under the new series, with the combined weight of diesel, petrol, and LNG rising to 4.8% from 2.4% earlier. Assuming a full pass-through, a USD 10 increase in crude oil prices can lead to an estimated 55 - 60 bps rise in headline inflation, with around 45 bps stemming from the direct effects and 10–15 bps from the indirect effects. However, indirect inflationary pressures could be higher, given the risks of potential supply disruptions.

We expect the direct effects of higher global crude oil prices on inflation to remain somewhat contained, assuming the price increase burden is shared by households, OMCs, and the government. The OMCs so far have enjoyed high gross refining margins, and as per our estimate, they may be able to absorb an increase in Brent crude oil prices up to USD 106/bbl. This estimate takes into account the recent cut in special additional excise duty on petrol and diesel by the government. Apart from higher crude oil prices, the inflationary scenario also faces upside risks from disruptions to the global gas supplies.

Beyond the direct impact of higher energy prices, concerns are rising over second-round effects stemming from elevated input costs and the possibility of widespread supply disruptions. India sources over a quarter of its fertiliser imports from West Asian countries. Moreover, around one-third of the global seaborne fertiliser trade (about 16 million tonnes) passes through the Strait, raising concerns about access to fertiliser. Also, more than 60% of India’s urea production relies on imported LNG as a feedstock. Supply disruptions could pose problems for the upcoming Kharif season, particularly amid the rising probability of the El Niño phenomenon.

Overall, assuming global crude oil prices average at USD 90/bbl in FY27, India’s CPI inflation is projected to average between 4.5 - 4.7%. We have revised our projection upward from the earlier 4.3%, which factored global crude oil prices ranging between USD 60-70/bbl. Our revised inflation projection assumes that a large burden of the higher global crude oil prices will be borne by the government and OMCs. We have based our projection on the expectation that the OMCs may be able to absorb an increase in Brent crude oil prices up to USD 106/bbl. Furthermore, our projection also factors in government support, as reflected in the recent cut in the special additional excise duty on petrol and diesel.

External Sector Pressures Intensify

India’s current account deficit is expected to face challenges amid the ongoing global turmoil, given its high energy dependence. India is dependent on imports to meet about 88% of its total oil requirement and 51% of its gas requirement. India has diversified its crude oil import sources, but West Asian countries still account for about 51% of total petroleum crude and product imports. Over the past five years, India has expanded its supply from the US and Russia. India imports 5.5–6 million barrels of crude oil per day. A USD 10 increase in crude prices could raise India’s import bill is around USD 20 billion. Given that India also exports a significant share of refined petroleum products, a USD 10 rise in crude prices could increase the current account deficit (CAD) by 30 - 40 basis points. Apart from crude oil's impact, there are two additional risks stemming from the exposure of exports and remittances to West Asian economies. India’s merchandise exports to West Asia were USD 64 billion (14.7% of total exports) in FY25. Furthermore, India’s remittances remain vulnerable to shocks from the West Asia conflict, as the Gulf Cooperation Council (GCC) countries account for nearly 38% of India’s inward remittances, totalling more than USD 130 billion. Overall, factoring in global crude oil prices averaging at USD 90/bbl for the full year, along with some pressure on exports and remittances, we estimate India’s CAD to widen to 2.1% of GDP (Vs our pre-conflict projection of ~1%).

At a time when India’s current account is facing renewed pressure, driven by its high dependence on energy imports and challenges to exports, it is important to note that India’s capital flows have also come under pressure amid volatile FPI flows and moderating net FDI. India’s FPI outflows further intensified following the West Asia conflict, reaching USD 13.6 billion in March, the highest monthly outflow in the last six years. With this, FPI outflows for FY26 were recorded at USD 16.6 billion, as against inflows of USD 2.7 billion in FY25. Looking ahead, persistent global uncertainties, elevated crude oil prices, and rupee weakness are likely to keep investor sentiment cautious, weighing on the FPI flows. Furthermore, net FDI inflows (Gross inflows – Repatriation – FDI by India) have consistently been negative over the past six months. Higher repatriations and FDI outflows have been weighing on India’s net FDI inflows. During 10M FY26, India’s net FDI inflows were recorded at USD 1.7 billion, compared to USD 1 billion in FY25.

Weakness in foreign investment flows, pressures on the current account deficit and global risk-off sentiment have kept the rupee under pressure. The rupee has depreciated by 4.3% (30th Mar-26) against the dollar since the beginning of the conflict in West Asia. However, the rupee remains significantly undervalued as at the end of February 2026 in REER terms. This suggests that when global conditions improve, the rupee has scope to appreciate. If the conflict ends soon and crude oil averages USD 90/bbl in FY27, we project the rupee to average around 92-93. However, if the conflict intensifies, the weakening pressure on the rupee may persist.

10Y G-Sec Yields Climb

Elevated oil and gas prices are stoking fears of increased fiscal and inflationary pressures, thereby pushing up Gsec yields across tenors. The 10Y G-sec yield has risen 37 bps in March, crossing 7%, a level last seen in July 2024. Looking ahead, G-sec yields are expected to face upward pressure due to heightened global uncertainties, inflationary pressures, and rising fiscal challenges. We estimate the fiscal burden from the excise duty cut on petroleum products, along with the possibility of an increase in subsidy burden and lower tax revenue collections, to be around 0.5% of GDP in FY27. As per our baseline scenario, if the price of crude oil averages USD 90/bbl in FY27, we expect G-sec yields to average 6.8 – 6.9% over the year.

RBI to Support Liquidity Conditions

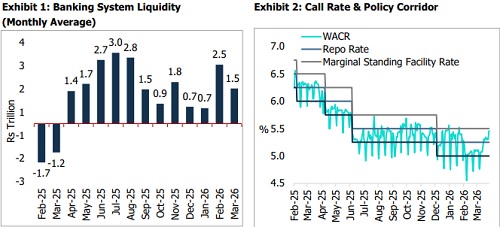

Banking system liquidity has averaged a surplus of Rs 1.5 trillion in March so far (up to 27 March), lower than Rs 2.5 trillion in February. The tightening of liquidity conditions, largely driven by tax outflows, has also led to a spike in the weighted average call rate (WACR). Thus, the RBI has been conducting VRR auctions and OMOs to ease the liquidity pressures. Going forward, we believe the RBI will continue OMO purchases to keep liquidity conditions comfortable.

Way Forward

The first monetary policy meeting of FY27 comes at a critical juncture, as the global economy faces turbulent times amid the intensification of the West Asia conflict. The duration of the conflict, along with its impact on the global energy prices and supply chains, will be the key factors to monitor going forward. Any escalation in the conflict poses material risks to the fundamentals of the global and domestic economies. There are heightened concerns not just about the global energy price trajectory but also about risks from global supply chain disruptions, which could have severe repercussions across many industries. In the current environment, the RBI is expected to adopt a calibrated strategy, opting for a pause in its forthcoming policy. Going forward, the RBI’s policy path will be highly dependent on the evolving external conditions and their implications for the domestic growth and inflation dynamics. Overall, the moderation in domestic growth prospects and heightened inflation risks amid the highly volatile global landscape have complicated the RBI's policy trade - offs, warranting a careful balance between supporting growth impulses and containing inflation pressures. The immediate effects of higher global crude oil prices on inflation are expected to remain somewhat contained, with the price increase burden being shared by the OMCs and the government. This provides some cushion to the RBI to hold the rates steady for now.

Above views are of the author and not of the website kindly read disclaimer