Life Insurance New Business Premium Maintains Steady Growth Momentum in May 2025, Led by Group Premiums by CareEdge Ratings

Overview

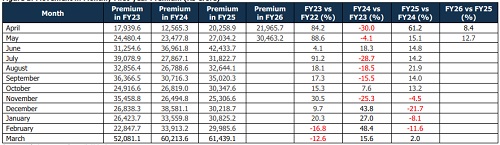

The Indian life insurance industry reported moderate year-on-year (y-o-y) growth of 12.7% in May 2025, reaching Rs 30,463.2 crore, following an 8.4% growth in April 2025 and lower than the 15.1% growth in May 2024. The slightly slower annual growth can be attributed to the effects of the surrender value regulations still playing out in the system. The month also witnessed a 10.4% fall in life insurance policies sold. The private players reported a growth in individual non-single premiums, while LIC experienced a 7.8% decline. Annual Premium Equivalent (APE) rose by 14.4% in May 2025, marginally higher compared to the growth of 12.0% in the same period last year. In APE terms, the industry grew at a 13.2% compounded annual growth rate (CAGR) between May 2023 and May 2025. During this period, private insurers grew at 13.8%, outpacing LIC’s growth of 12.4%

Figure 1: Movement in Monthly First-year Premium (Rs Crore)

Figure 2: First-year Premium Growth of Life Insurance Companies (Rs Crore)

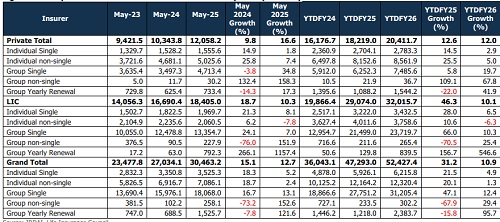

In May 2025, private players’ new business premiums increased by 16.6%, outpacing the growth of 10.3% reported by LIC. The overall industry expansion was driven by all segments except for a decline in LIC’s non-single premium segment. While there was a drop in the number of individual non-single policies sold, the impact was partially offset by higher average premiums per policy. Growth continues to be influenced by structural changes in policy design, particularly adjustments to sum assured and commission structures following the revised surrender value guidelines, effective October 1, 2024. At the same time, market volatility has dampened demand for ULIP products, affecting overall sales momentum.

Figure 3: Movement in Premium Type of Life Insurance Companies (Rs Crore)

In May 2025, non-single premiums grew by 15.1%, higher than the 10.8% growth in May 2024. Largely driven by LIC and private players, single premiums saw an 11.7% rise, a slowdown compared to 17.0% in May 2024. Single premiums continue to be approximately 2.5x larger than the non-single premiums in absolute terms. The private sector holds a larger share in the non-single sub-segment (individual premiums), while LIC continues to dominate the single premium subsegment, particularly in group business.

Figure 4: Movement in Premium Type of Life Insurance Companies (Rs crore)

In May 2025, group premiums rose by 18.4% compared to 13.1% in May 2024. Individual premiums, however, grew by a muted 3.3%, significantly slower than the 18.6% gain the previous year. The private sector continued to lead the individual segment, while LIC retained its dominance in the group segment.

Figure 5: Movement in Individual Non-Single Policies of Life Insurance Companies (in Lakhs)

In May 2025, individual non-single policy sales declined by 10.5%, in contrast to a 13.8% growth recorded in the same period last year, marking a sharp reversal in trend, primarily attributed to LIC, and this decline was exacerbated by the decrease in private insurers. The significant decline in the number of policies sold can be attributed to the implementation of new surrender value norms, which took effect in October 2024. Private players seem to have adapted to the revised surrender value regulations as they have increased the value of individual non-single policies. Meanwhile, insurers have focused on selling higher-value policies, which has helped mitigate the impact on premium income; however, the policy mix will impact margins.

Figure 6: Movement in APE of life insurance companies (Rs Crore)

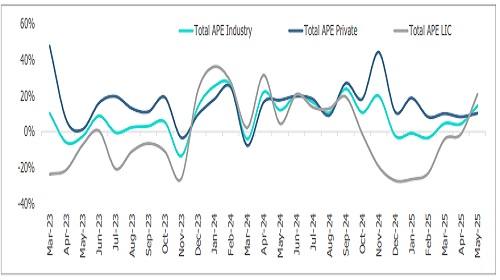

Figure 7: Total APE growth (on y-o-y basis, in %) – Non-Single Premiums driving Private Growth

Figure 8: Individual APE growth (on y-o-y basis, in %) – Private players coming to terms with the changes

Figure 9: Group APE growth (on y-o-y basis, in %)

CareEdge Ratings View

“Typically, the first quarter is the weak season for the life insurance segment as it immediately comes after the fiscal end, where most retail customers rush to buy policies. In May, the YoY growth has come down compared to 15.1% in the same month a year ago, mainly because of the impact of revised surrender value guidelines, effective October 1, 2024. May also saw a fall in the volume of policies sold, especially individual non-single premiums, which are regular premiums paid by retail customers. Both LIC and private insurers reported a fall. However, private insurers reported a premium growth despite this, indicating that they have moved to higher value policies amid changes in surrender value regulations. Individual non-single policies fell by 10.5% y-o-y to 16.7 lakhs,” said Saurabh Bhalerao, Associate Director, CareEdge Ratings

According to Sanjay Agarwal, Senior Director, CareEdge Ratings, “The growth of ULIPs has been muted due to market volatility. Meanwhile, group business has driven growth for the month. There is likely to be an increased emphasis on the agency channel, spurred by banks' focus on deposit gathering. Furthermore, the proposed Insurance Amendment Act aims to enhance market penetration by encouraging new companies to enter the market. A gradual recovery is expected in FY26, driven partly by private insurers expanding their reach through deeper geographical penetration, in conjunction with the launch of the Bima Trinity. CareEdge expects the life insurance industry to continue growing at 10%-12% over a three-to-five-year horizon, driven by product innovation, supportive regulations, rapid digitalisation, effective distribution, and improving customer services.”

Above views are of the author and not of the website kindly read disclaimer