Internet Sector Update : Eternal & Swiggy : Steady on food, stormy on quick commerce by Motilal Oswal Financial Services Ltd

Our channel checks ahead of the 4QFY26 earnings season suggest a divergent quarter for the two listed internet platforms, Eternal (Zomato) and Swiggy. Food delivery (FD) should post an improved quarter, with both players likely to report 18-20% YoY growth in gross order value (GOV), aided by a benign base and limited disruption from the recent gas shortage on actual order volumes, for now. For quick commerce (QC), competitive intensity, particularly from Zepto, which continues to operate at lower minimum order values and higher discounts, is beginning to weigh on volume growth for both Blinkit and Swiggy Instamart. We have cut our near-term growth estimates for both platforms to reflect this deceleration. However, following a meaningful correction (Eternal down 32% and Swiggy down 50% from peak), we believe valuations have turned attractive. Despite a reduction, our new TPs imply ~37x FY28E EV/EBITDA for Blinkit and 0.4x FY28E EV/GMV for Swiggy. We maintain BUY on both names.

Food delivery: Benign base, resilient growth, and a fee-fueled margin lever

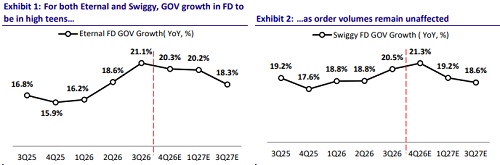

* Our channel checks indicate FD order volumes were largely unaffected by the gas shortage in the quarter. We expect both Eternal and Swiggy to report GOV growth of 20-21% YoY in 4QFY26E, an improvement from the ~15-18% range seen in the previous few quarters.

* This is largely also due to a benign base. We still expect sequential weakness – QoQ decline of 2% for Eternal and 1% for Swiggy in FD.

* The more interesting development is the persistent hike in platform fees, now at ~INR14.9 (excl. GST) per order for both Eternal and Swiggy. At 3-4% of AOV, this is eye-watering, in our view, and we suspect both players are leaving some demand on the table. Yet, it is notable that growth rates continue to hold in the 15-20% range despite this implicit demand tax.

* FD continues to serve as the primary cash flow lever for quick commerce ambitions. Platform fee hikes, combined with improving unit economics, are generating the incremental EBITDA needed to absorb losses in Blinkit and Instamart (Exhibit 9-10).

* We view the growth-profitability trade-off as deliberate — management teams appear comfortable sacrificing some revenue growth for margin accretion, a rational choice given the QC funding requirement.

Quick commerce: Competition is real, but the pie is still expanding

* The standout datapoint this quarter is the continued deceleration in QC volume metrics. Growth in orders per day and net order value (NOV), which was trending at 25%+ QoQ and 125%+ YoY, respectively, as recently as 2-3 quarters ago, should slow in 4Q as it did in 3Q. We estimate 9-12% QoQ growth in orders per day and 6-10% QoQ growth in NOV for both Blinkit and Instamart

* While part of this deceleration reflects a higher base, we believe the competitive impact is real. Zepto’s aggressive positioning — lower minimum order values and steeper discounts — is clearly eating into the market share of the listed players.

* That said, we believe the overall QC pie continues to expand. The slowdown is more a function of share redistribution than demand destruction right now.

Near-term estimates cut: Competitive intensity likely to stay elevated

* We have cut our near-term QC estimates for both Blinkit and Swiggy Instamart. We now expect NOV CAGR of 42%/36% for Blinkit/Instamart over FY26-28 vs. 51%/38% earlier. The revision is driven primarily by lower volume growth assumptions, partially offset by stable-to-improving AOVs.

* We expect competitive intensity to remain elevated through FY27; the key monitorable over the next 2-3 quarters is whether the listed players choose to increase discounts.

* We expect short-term volatility in share prices as the market adjusts to slower growth prints. However, we view this as time-value erosion rather than a fundamental de-rating, given that the underlying category growth story remains intact.

Valuation and view: Correction creates opportunity; maintain BUY on both

* The recent correction has compressed valuations meaningfully. Eternal is down 32% and Swiggy is down 50% from the peak, creating what we view as an attractive entry point for medium-term investors.

* We continue to view FD as a stable duopoly with balanced market shares between Eternal and Swiggy. We maintain 35x FY27E EV/EBITDA for FD business of Eternal and Swiggy.

* Eternal: Our revised TP of INR340 implies ~37x EV/EBITDA on FY28 Blinkit estimates, with a potential upside of 44% from the current levels.

* Swiggy: Our revised TP of INR390 implies ~0.4x FY28E EV/GMV for QC business, still a discount of 50-60% to Eternal’s multiple and we believe it offers a better upside from hereon.

* Despite our TP cuts, we maintain BUY on both names. The competitive concerns are real but priced in, in our view. We prefer Eternal for its execution track record and Blinkit’s category leadership, though we believe Swiggy offers greater upside from the current levels given the steeper discount.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

More News

Consumer Sector Update : Q4FY26 Quarterly Results Review by Choice Institutional Equities Ltd