Initiating coverage & stock picks for Q2FY27 by Monarch Networth Capital

Pricol Ltd.

BUY - TP – Rs 724|Upside- 17%

What we like in the company

• Pricol is a leader in 2W domestic cluster industry with a 40% market share. It also enjoys a market leadership in clusters for CV. The other two divisions which form ~50% of the total revenue consists of pumps, switches and 2W plastic component.

• Pricol is diversifying and enjoying the value growth from premiumization (shift to LCD and TFT from analog) in cluster business with addition of new customers and programs in PV segment reducing the high 2W dependency.

• Pricol is undertaking a large Rs 4.5bn capex to expand the capacities at the P3L plastic components business which is expected to grow swiftly.

Near-term triggers

• With new programs from Tata Motors like the Sierra and Punch and several more platform launches for Tata Motors, we expect revenue growth to continue exceeding underlying industry growth.

• We expect sharp growth for the P3L business due to new orders from non-TVS customers and capacity expansion, with a target to double the revenue for this segment over FY25-FY28E.

• The announced demerger should help unlock much more value for the DIS segment which enjoys very high barriers to new entrants due to its technology excellence.

Earnings Outlook

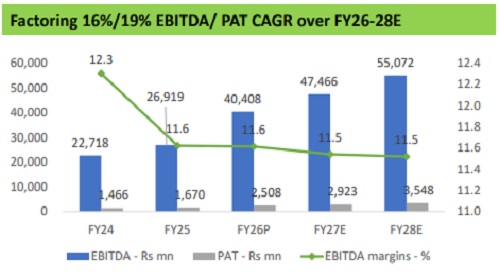

• We expect the company to deliver 17%/16%/19% Revenue/EBITDA/PAT CAGR over FY26-28E due to the compounding of revenue in DIS business and robust growth in the P3L business.

• The near-term pressure on margins will iron out from 2QFY27E, once the price pass on comes into effect, thereby protecting margins for FY27E.

Valuation and view

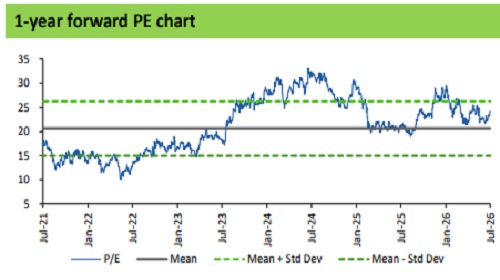

• We value Pricol at 25x FY28E PE to arrive at a TP of Rs 724 and a BUY rating.

• At CMP, Pricol trades at a very attractive valuation of ~21x FY28E P/E.

• Key Risks: Deep downcycle in 2W, weakness in exports, margin pressure due to cost inflation.

Redington Ltd

BUY - TP – Rs 340|Upside- 24%

What we like in the company

• Leading technology distributor with diversified presence across IT, Mobility, Cloud and Lifestyle products across India, Middle East, Africa and Turkey.

• Strong OEM partnerships and an extensive channel network provide scale, vendor access and execution advantages.

• Increasing focus on cloud, software and value-added solutions is improving business quality and margin profile.

• Asset-light business with disciplined working capital management, healthy cash generation and consistently strong return ratios.

Near-term triggers

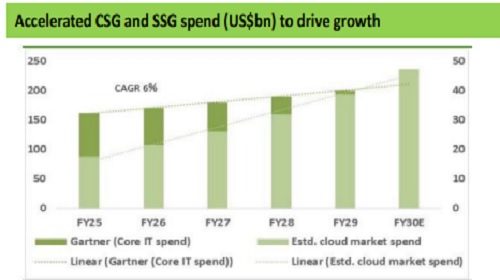

• Recovery in enterprise IT spending and the upcoming PC/server refresh cycle should support growth.

• Rising adoption of cloud, AI infrastructure and cybersecurity solutions will drive higher-margin technology solutions revenue.

• Improving product mix towards cloud and software, along with premium mobility demand, should aid margin expansion.

Earnings Outlook

• We We factor in Revenue/EBITDA/PAT CAGR of 15.7%/16.9%/7.3% over FY25-FY28E

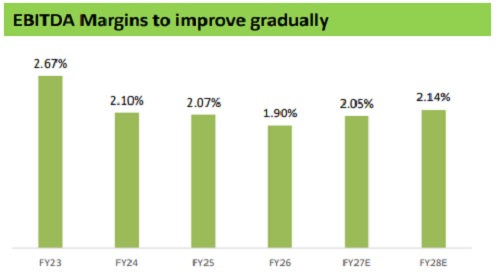

• EBITDA margins are expected to improve gradually, driven by an increasing contribution from higher-margin cloud, technology solutions and services. We value the company at 12x FY28E EPS, arriving at a Target Price of Rs 340

Valuation and view

• We ascribe 12x multiple to FY28 EPS and arrive at a target price of Rs 340 an upside of 21.8%

• At CMP of Rs 279 stock trades at 11.9x Mar’28E P/E.

Please refer disclaimer at https://www.mnclgroup.com/disclaimer

SEBI Registration Number is INZ000043833