Indian Transmission Sector: Capex Acceleration Critical for Energy Transition by CareEdge Ratings

Synopsis

* The Indian power transmission sector is poised for a significant scale-up in capital expenditure over the medium term.

* This is driven by rising peak power demand, rapid renewable energy additions and the requirements under the National Electricity Plan (NEP) 2022–32.

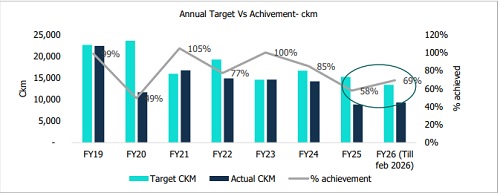

* From a credit perspective, the execution-related risks remain elevated during the construction phase due to right-of-way (RoW) and approval-related challenges corroborated from the execution target achieved for FY25.

* The overall outlook for the sector remains ‘Stable’, anchored by the inherent resilience of commissioned assets and sustained policy support, notwithstanding the near-term execution intensity.

Demand Outlook and Transmission Requirements

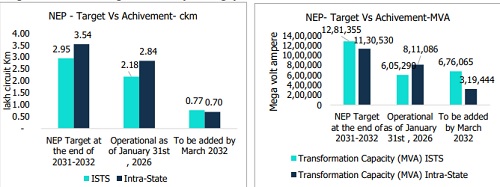

India’s peak power demand is projected to increase to 458 GW by FY32, from approximately 275 GW as of mid FY25, reflecting strong underlying growth in electricity consumption and accelerated renewable capacity deployment, with a target of about 500 GW by 2030. To meet this demand trajectory, the Government of India (GoI) has finalised a transmission expansion plan under the National Electricity Policy (NEP) 2022–32, entailing a total capital outlay of Rs 9.16 lakh crore, of which Rs 6.60 lakh crore pertains to the Inter-State Transmission System (ISTS), with the balance allocated to intra-state networks.

The plan envisages adding over 6.00 lakh circuit-kilometres (ckm) of transmission lines and more than 24.00 lakh MVA of transformation capacity by FY32.

As of January 2026, approximately three-fourths of the targeted ISTS transmission line length has been commissioned, with the balance to be added over the remaining plan period, while Intra-state transmission lines exhibit slightly higher completion levels. However, the transmission expansion continues to miss NEP targets, with annual transmission line additions lower than the targets for the last three years till Feb 2026. During FY25, the addition to the transmission line was 8,830 ckm, 42% below the target of 15,253 ckm.

The relatively slower pace of transmission line additions reflects recurring challenges related to RoW acquisition, forest clearances and land acquisition for substations. As of January 2026, 76 projects under the tariff-based competitive bidding (TBCB) framework, having an aggregate cost of above Rs 93,000 crore were operational, of which a limited portion were commissioned within the originally scheduled timelines, while the majority experienced time overruns, largely ranging between 3 and 18 months. Recent regulatory and policy interventions are expected to mitigate execution risks for RoW-related delays partially; however, their full impact will unfold over the next few years.

ISTS Network Expansion up to FY30-FY31

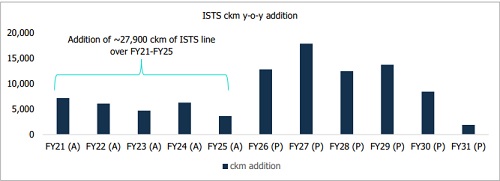

To achieve NEP targets for ISTS, Central Transmission Utility of India Limited (CTUIL), as per the master rolling plan for September 2025, has identified the addition of 67,263 ckm of transmission lines and a transformation capacity of 6.30 lakh MVA up to FY31.

The planned addition under CTUIL entails an approximate capital outlay of Rs 4.86 lakh crore, of which projects of 31,919 ckm and 3.35 lakh MVA, with a capital outlay of Rs 2.22 lakh crore, are under implementation, while the balance projects of Rs 2.64 lakh crore are either under planning, approval, or bidding stages. The target achievement shall entail an average capex of ~Rs 81,000 crore every year from FY26-FY31, as against the average industry capex of ~Rs 45,000-Rs 48,000 crore over the past three years ended March 31, 2026. As of January 2026, 82 TBCB projects aggregating approximately Rs 2.22 lakh crore are currently under implementation. Among these, 35 projects are progressing as per schedule, while the remaining projects are facing delays. Encouragingly, for 36 out of 47, the delays are up to 12 months, suggesting manageable execution risks within the ongoing project pipeline

CareEdge Ratings’ View

“The opportunity pipeline in the transmission sector is substantial, with a capex outlay of ~Rs 4.86 lakh crore from FY26-FY32; however, execution challenges—largely stemming from right-of-way issues, forest clearances and coordination delays leading to time overrun up to 12 months. Challenges involved in scaling up resources are also a constraint. The achievement of the target appears ambitious, considering the annual industry average of ~Rs 45,000 crore every year over the last three years, ending FY26. That said, the stable cash flow profile of operational assets backed by healthy collection efficiency, maintenance of normative line availability and long concession periods lends resilience to credit quality,” said Palak Vyas, Associate Director, CareEdge Ratings.

Above views are of the author and not of the website kindly read disclaimer