India Strategy : Peace dividend – Expect a sharp bounce by Emkay Global Financial Services Ltd

Global markets rallied (SPX: +1.6%) and crude collapsed (Brent: -12%), led by the US suspension of air strikes on Iran. There is still some uncertainty and the Strait of Hormuz is still closed, though peace looks highly likely now and is our base case assumption. We see it as a strong positive for India and expect the Nifty to rebound after a 5% collapse in the last three trading sessions. OMCs, private banks, NBFCs, and autos are the best ways to play the recovery.

End of war in sight

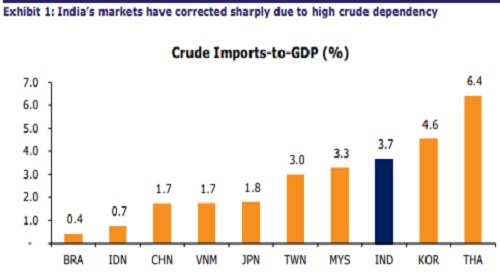

The US today suspended airstrikes on Iran’s energy infrastructure, citing ongoing talks and potential peace. Iran is yet to officially confirm, with the Speaker of the Iran Parliament denying the talks. Markets turned cautiously optimistic, with Brent dropping ~12% and the SPX rallying 1.6% on the back of this news. We acknowledge that this is not a done deal yet, with the re-opening of the Strait of Hormuz the critical milestone in the process. However, the probability of peace is significantly elevated and we think markets will aggressively price that in. India, obviously, is a bigger beneficiary relative to other global markets because of its high exposure to imported crude. We expect Brent to retrace to USD75-80/bbl, once clarity emerges.

Smart recovery in markets likely

The Nifty fell 5% in the last three trading sessions, primarily owing to sustained FPI selling (USD2.5bn). We expect this trend to reverse, and India could emerge as one of the better investment opportunities in the region. The key catalysts are the crude price overhang waning and P/E premium contracting. The optimism should spill over into other asset classes too. The currency should bounce back to pre-war levels (~Rs91/USD) while the 10Y bond should also drop, to ~6.65% from 6.83% currently. It may take 2-3M for the economy to normalize, but asset markets will discount the peace dividend immediately.

Some scars to remain

We expect some impact on 4QFY26 earnings, with a spillover to 1QFY27. Supply chains are likely to take 1-2M to normalize after the Strait of Hormuz reopens. Moreover, the damage to some of the energy infrastructure in the Middle East could delay the full normalization of oil markets. We estimate the earnings impact on the Nifty at 1-2% (FY27E). SMID companies may see a larger downgrade, but it would mainly be restricted to 1-2 quarters, with a smaller impact on FY27 estimates. Notably, the street is yet to react to the war, with both Nifty and broader market estimates unchanged in Mar-26.

Top trades

We see this as the bottom for the markets and maintain Dec-26E Nifty target of 29,000, based on +1sd PER of 20x. The short episode is unlikely to derail India’s consumption-led recovery, and we see FY27E Nifty EPSg on track at ~15%.

Our top ideas to play the market recovery are picked from a basket of the worst performers since 26-Feb-26:

1) OMCs (short war duration = manageable earnings impact, all trading at LTA on PBV ).

2) L&T (-22%, with low damage to its Middle-East projects)

3) HDFC Bank (-16%, trading at ~1.5x PBV and over-reacted to the Chair resignation)

4) BJFIN (-16%, with minimal damage to earnings)

5) SHFL (-19%, beaten down on fears of a fuel price hike)

6) Indigo (-18%, ATF prices should correct + schedule normalization in 2-3M)

7) Ashok Leyland (-23%, beaten down on worries around diesel price hikes; now moot)

Meanwhile, we expect some of the “protection” trades to reverse – Tech, Reliance, and ONGC now look vulnerable, at least relatively

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

.jpg)

India VIX decreased by 0.13% to close at 11.21 touching an intraday high of 11.37 - Nirmal B...