India amid the West Asia conflict Caught in a squeeze by Emkay Global Financial Services Ltd

Elevated risks of wider energy supply disruptions from a prolonged Iran conflict prompt a reset of India’s macro realities. We shift our baseline FY27E forecast around a more realistic, yet manageable, Brent average of USD80/bbl, with higher pressure in 1Q. Accordingly, we trim FY27E GDP growth by 0.4pp to 6.6% and raise inflation and CAD/GDP to 4.3% and 1.7%, respectively. A more adverse terms-of-trade shock, with Brent above USD100/bbl, could push CAD/GDP beyond 2.5% and drive a BoP deficit of ~USD85bn. The eventual growth, inflation, and fiscal hit will largely hinge on how a sustained crude shock is distributed between OMCs, the government, and end consumers. With OMC underrecoveries (GRM-adjusted) already exceeding ~Rs3trn at current prices, the burden is likely to fall disproportionately on the government, implying a minimum fiscal cost of ~0.5% of GDP. The RBI is likely to allow calibrated INR depreciation while keeping a check on rates through market interventions. The trade-offs are not easy, nonetheless. USD/INR is set to reach 96, while the 10Y yield could drift higher and touch 6.95%.

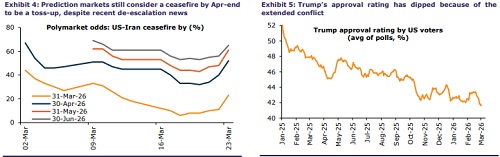

Revising macro forecasts as geopolitical risk premium keeps oil market hot The West Asia conflict is entering a more precarious phase, despite recent news around potential deescalation. Recent attacks on energy infrastructure have heightened the risk of broader and persistent supply disruptions. India faces an adverse terms-of-trade shock from rising energy prices, with ~45%/55% of crude oil/gas imports from the region and limited domestic strategic reserves. Besides, a protracted conflict implies a broader supply shock, global stagflationary tail risks and heightened volatility, impacting India’s exports, remittances (~40% from ME) and capital flows. Early signs of strain in domestic gas supply are visible, while short-term inelastic oil demand constitutes a direct macro shock. We revise our baseline macro forecasts, basis Brent averaging ~USD80/bbl, up 15% from earlier. We reckon that while oil and natural gas prices have edged higher, they remain well below levels that would typically reflect a shock of this scale and duration. Brent at USD80-85/bbl will be mostly manageable, while the macro impact will be more acute and non-linear if prices average north of USD100/bbl. With the revised oil forecast, we lower baseline FY27E real GDP growth by 0.4pp to 6.6%, and raise headline inflation and CAD/GDP by 0.3pp to 4.3% and by 0.4pp to 1.7%, respectively. Our dynamic scenario analysis suggests that with average Brent at USD100/bbl for FY27E, CAD/GDP could widen to >2.4% while the BoP deficit could worsen to >USD85bn.

Burden sharing, uneven distributional effects and associated trade-offs The eventual growth, inflation, and fiscal hit will largely depend on how the crude price shock —if sustained—is distributed between OMCs, the government, and end consumers (households and firms). OMCs’ price shock absorption, while entailing a smaller pass-through to retail inflation, effectively also carries a mild fiscal cost, as it reduces the dividend/corporate taxes transferred to the government. Our estimates suggest at the current Brent prices, retail pump prices of diesel and petrol need to rise by 43% and 19%, respectively, for OMCs to earn normalized gross marketing margins. OMCs’ annualized deficit on auto fuels at current prices are tracking a massive Rs3.0trn (adjusted for super-normal gross refining margin gains). Our model simulation suggests that at current oil prices, the government will need to cut excise taxes by ~Rs19.5/ltr avg blended for diesel and petrol and absorb extra subsidy on LPG (estimated Rs1trn) to fully bear the OMC losses. This could entail a fiscal cost of nearly 1.1% of GDP. The best fit in our view, in a sustained pain scenario, is equal passthrough among all economic agents, which still effectively imposes the highest cost on the government. However, this could imply inflation hit to be sub-35bps, and OMC burden falling to 0.35% of GDP. However, the effective fiscal hit of ~0.5% of GDP would crowd out other policy spending.

RBI’s battle unlikely to be easy: FX and rates trade-offs There is no simple playbook for a monetary policy response to energy price shock. Amid benign inflation, the pre-war policy focus was on monetary policy transmission—especially in the bond market—via ample liquidity that kept overnight rates below the policy rate. While direct oil passthrough remains limited under managed pump prices, second-round effects via inflation expectations, growth shocks, and tighter financial conditions now shape the RBI’s trade-offs. The bar for any conventional rate hike remains high in the face of a supply shock; however, it needs to be seen if the RBI remains comfortable injecting abundant liquidity and sub-repo overnight rates. With INR under steady strain despite consistent FX intervention (largely via forwards), the associated liquidity drain is being deferred, while rates have been kept in check through the RBI’s bond purchases. A sharp policy response in the form of interest rate defense—raising overnight rates to curb FX arbitrage— appears unlikely at this stage. USD/INR now looks poised to touch 96, while the 10-year yield may edge higher and touch 6.95%.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354