Hold Tata Elxsi Ltd for the Target Rs.5,500 by PL Capital

Transportation drives strong performance, Broader recovery still away

Quick Pointers:

* Top client business normalization & accelerated ramp-up of previously won deals within Transportation aids strong performance

* Robust execution drives margin expansion despite wage hike impact

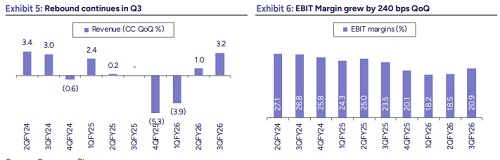

The revenue performance (+3.2% QoQ CC) exceeded our estimates (+2.5% QoQ CC), aided by robust growth in Transportation vertical (+7.3% QoQ CC). The sharp uptick in Transportation is a combination of ramp up in anchor account along with a spending recovery in strategic top accounts, ex-top 10 accounts declined 7.5% in USD. The OEMs’ participation is inclined towards costs savings instead of focusing on the innovation and growth areas. The M&C and H&L performance was discouraging and reported third consecutive quarters of decline. We believe the underlying spending pattern within M&C and H&L is sporadic, attributed to the structural issues, and would require couple of more quarters to achieve a steady state. The management was confident of reviving growth within these two verticals on the back of new logo additions and few closures that concluded in Q3. On margin, it exceeded our estimate by 140bps QoQ. At the current margin, the utilization stood at ~75%, it aspires to achieve 85% utilization with a combination of deploying automation and AI. Additionally, we believe the decoupling of revenue growth and talent hiring would provide incremental margins levers. We are revising our margins up by 70bps/40bps/20bps for FY26E/FY27E/FY28E due to beat in Q3. We expect CC revenue to decline by 4.8% (-5.1% QoQ earlier) in FY26E and grow by 9.8%/11.6% YoY in FY27E/FY28E. We are assigning 33x PE to FY28 EPS, translating a TP of 5,500. Valuations capped, retain HOLD.

Revenue: TELX delivered strong revenue growth, led by the Transportation segment, supported by normalization at its top client and accelerated ramp-up of previously won deals. This strength offset sluggishness in the Media & Communications and Life Sciences & Healthcare segments. Overall revenue grew 3.2% QoQ in CC, exceeding our expectation of 2.5% QoQ CC growth, driven by robust Transportation segment growth of 7.3% QoQ CC.

Operating Margin: Strong execution drove margin expansion, with EBIT margin improving by 240 bps QoQ to 20.9%. The margin expansion was led by operational efficiency gains, including higher utilization (+200 bps), cost optimization initiatives (~85 bps), and currency tailwinds (~45 bps), partly offset by headwinds from wage hikes for junior staff (~110 bps). Reported PAT was impacted by a onetime provision of Rs. 957 mn related to changes in labour laws.

Hiring & Utilization: Net employee count declined for 4 th consecutive quarter, with a reduction of 357 employees in Q3, taking the total workforce to 11.6k. Utilization improved to ~75% in Q3, driven by strong execution, and management expects further improvement. TELX indicated a comfort utilization band of ~80%, with potential to scale utilization up to ~85% through increased adoption of AI and automation.

Valuations and outlook: We estimate USD revenue/earnings CAGR of 9.9%/23.4% over FY26E-FY28E. The stock is currently trading at35x FY28E earnings, we are assigning P/E of 33x to FY28E earnings with a target price of INR 5,500. We maintain our HOLD rating.

Strong Beat in Result, Top Clients Drive Strong Performance

* Reported revenue growth of 3.2% QoQ CC above our estimate of 2.5% QoQ CC

? Segment-wise within the SDS business, growth was led by Transportation, which expanded 7.3% QoQ in CC terms. Media & Comms and Healthcare were laggards, declining 1.3% and 4.3% QoQ CC, respectively, marking 3rd consecutive quarter of decline in healthcare

* Region wise in USD terms, growth was driven by Europe which grew by 10% QoQ while America grew by 2.4%. India & RoW regions were laggards declining by 11.1% & 12.1% QoQ respectively

* Reported EBIT margin of 20.9% (up 240bp QoQ) above our estimates of 19.5% & consensus estimates of 18.5% largely due to gross margin expansion

* Growth was driven by the top five clients, which reported strong growth of 10.5% QoQ in USD terms, while clients ranked 6–10 and those beyond the top 10 declined by 3.7% and 7.5% QoQ, respectively

* Net employees declined by 357 to 11.6k during the quarter (4th consecutive quarter of decline), LTM Attrition was up by 20 bps QoQ to 15.6%

* Adj. PAT excluding one-off came at Rs. 2.05 bn, above our estimates of Rs. 1.78 bn

Conference Call Highlights

* Macro environment remains volatile and clients decision-making continues to be slow; however, management indicated that clients are increasingly moving ahead with value-proposition–based projects.

* Transportation momentum is expected to remain strong and sustainable through Q4FY26 and FY27, driven by adjacency creation in off-road segments, further ramp-up potential in existing deals, and traction across SDV, EV/hybrids, ADAS, and connected platforms.

* Anchor client normalization still underway, with performance yet to return to normalized levels; management expects this to play out over the next 1–2 quarters, providing additional growth runway once recovery is complete.

* M&C declined due to seasonal furloughs and delays in deal closure; however, ramp-up of select large deals is underway, with management expecting a return to growth from Q4.

* Management mentioned that the Healthcare segment has bottomed out after several weak quarters. They further indicated that a turnaround is expected from Q4 itself, with growth in FY27 supported by new client additions, deal wins, and a robust pipeline.

* Wage hike for senior employees will be implemented in Q4, and management expects a margin impact of ~70–80 bps.

* Management mentioned that hiring will remain calibrated and focused on niche skills in the near term; large-scale hiring is unlikely for next few quarters.

* Provision for the new labour code has been fully recognized in Q3; the ongoing impact is expected to be limited to 15–20 bps on margins and should be offset by other levers, subject to final regulatory clarity.

* TELX secured multiple large, multi-year deal wins across Healthcare, Transportation, and Communications, reinforcing its diversified growth engine. These wins underscore strong traction for differentiated, platformand IP-led offerings and collectively enhance revenue visibility.

Above views are of the author and not of the website kindly read disclaimer

600-400.jpg)