Hold InterGlobe Aviation Ltd For Target Rs.4,724 by Prabhudas Liladhar Capital Ltd

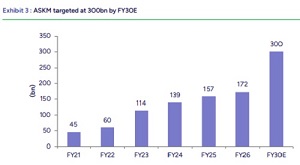

Encouraging long-term ASKM guidance

We attended INDIGO IN’s analyst meet wherein the management highlighted plans to

1) Reach ASKM of 300bn

2) Increase the share of owned and finance-leased aircraft to 30-40% of fleet mix

3) Increase international ASKM share to 40% by FY30E. In addition, given excessive FX volatility witnessed in recent times, INDIGO IN aims to expand the hedge cover to 33% of net BS exposure by FY27E/FY28E. Despite a modest capacity addition growth guidance of single digit for FY27E, the long-term target to reach ASKM of 300bn by FY30E (15% CAGR over FY26-30E) is encouraging. We believe near-term growth will be price led (PRASK is likely to grow by mid-teens in 1QFY27E) amid sharp repricing given excessive ATF price volatility. We broadly retain our estimates and expect sales/FX-adjusted EBITDAR CAGR of 10%/4% over FY26- 28E. Given multiple headwinds arising from capacity bottlenecks in near term, FX volatility and rising crude prices, we maintain HOLD on the stock with a TP of INR4,724 (9x FY28E EBITDAR; no change in target multiple).

Long-term capacity guidance is encouraging:

While capacity growth is likely to be in single digit during FY27E, INDIGO IN is aiming for ASKM of 300bn by FY30E, translating into 15% CAGR over FY26-30E. Barring near-term aberrations, the long-term capacity guidance is quite encouraging, largely led by plans to expand presence in international markets. Nonetheless, we believe pick-up in growth is largely back-ended and near-term challenges continue to prevail. Consequently, we expect ASKM to grow by 6.1% YoY/10.4% YoY to 182bn/201bn in FY27E/FY28E.

Plans to increase international ASKM share to 40% by FY30E:

INDIGO IN’s international ASKM share has increased from 16% in FY16 to 32% in FY26. From 5 destinations and 12 routes in FY16, the international network has expanded to 44 destinations and 150+ routes in FY26. While the Middle East crisis has put temporary brakes on international expansion, addition of more routes and induction of XLRs/widebodies into the portfolio is expected to increase the share of international ASKM to ~40% by FY30E.

INDIGO IN is strengthening its international footprint through induction of A321-XLRs and widebody aircraft supporting expansion across mid- and long-haul markets, respectively. Notably, the share of XLRs and widebodies in the overall capacity mix is expected to increase from 4% in FY26 to 10-15% by FY30E. A321-XLRs have already been deployed on routes such as Athens, Istanbul, Bali and Seoul, with further expansion planned across select destinations. Delivery of 9 A321-XLR aircraft is expected in FY27E, which should further accelerate international network growth.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

Tag News

IndiGo moves up on signing MoU with CFM International