Economy Update : Oil reality check by Emkay Global Financial Services Ltd

The US-Iran deal and the imminent reopening of SoH has led to Brent plummeting below USD85/bbl; however, there is a material risk of continued physical market imbalances causing prices to move toward and beyond USD90/bbl in coming weeks. Supply normalization delays and especially a return of pent-up demand largely from China could put a floor on oil prices. However, prices should correct meaningfully beyond 1HFY27 and fall to USD70/bbl by end-FY27. With 1HFY27 likely to see elevated oil prices, we retain FY27E Brent forecast at USD90/bbl, with GDP growth at 6.3%, headline inflation at 5.1%, CAD/GDP at 2.3%. BoP should, in our view, move to near-zero on USD70-75bn of estimated flows following GoI and RBI measures, with the rupee appreciating toward 93 by end-2QFY27.

Physical market imbalances a key risk to lower oil prices

The US-Iran peace agreement has arrived, in line with our expected timelines, with oil market pressures building up. We had previously assessed that oil prices would have skyrocketed beyond USD120/bbl if a deal to open SoH was not agreed on by end-Jun, with buffers rapidly being exhausted. While Brent prices have fallen below USD85/bbl postannouncement, we continue to look at the physical oil market to gauge the path ahead for oil prices. With supply normalization via Hormuz (to pre-crisis levels) expected to take weeks, if not months, there is a material risk that oil prices will slowly grind upward, toward and beyond USD90/bbl in coming weeks, if pent-up demand returns quickly. However, prices should correct meaningfully and sustainably beyond 1HFY27, in our view, falling to USD70/bbl by end-FY27. Crucially, this does not move the needle for our baseline forecasts – With 1HFY27 likely to see elevated prices (avg: USD95/bbl; 2HFY27E: USD85/bbl), we retain FY27E Brent forecast at USD90/bbl (Oil imbalances: The price of war and resilience).

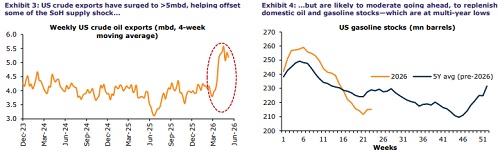

SoH supply normalization to take time, while US oil exports to drop materially

On the supply front, normalization of flows via SoH is likely to take weeks. Operational friction such as tanker availability, insurance costs, war-risk premiums, and clearance of mines/security risks in SoH, etc will linger, while resumption of production from shuttered oil wells will also require time. At the same time, historically high US oil exports, which had provided a substantial buffer for the oil market in the absence of Hormuz flows, are set to meaningfully decline. US oil will be redirected domestically with the start of the US driving season, amid record-low gasoline and domestic crude stocks. The expected oil glut postSoH reopening will only occur post 1HFY27, as flows eventually normalize and global oil production ex-Middle East continues apace.

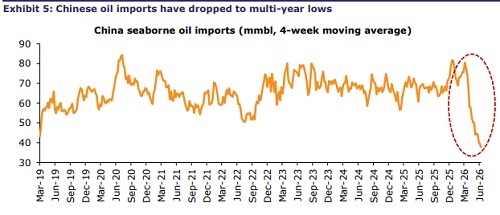

Chinese oil imports to surge substantially, alongside global inventory restocking

The biggest factor behind oil prices remaining relatively contained despite the scale of the supply hit has been China. Chinese oil imports have fallen to multi-year lows (down 50% in Jun vs Feb), as it has drawn down on commercial inventories and restricted refinery production to manage the crisis. With commercial inventories beginning to dry up, China will soon return to the oil market as a buyer, thus adding a significant source of demand that had been absent so far. This will be supplemented by global oil demand rising in response to the deal – OECD commercial stocks are also at multi-year lows, while the US (and others) will also look to refill its strategic reserves. Global oil demand is expected to remain higher than supply in 2026 which will put a floor on prices in the short-term, till supply normalizes to pre-crisis levels.

Domestic macro environment to improve from 2HFY27 onward

We maintain our FY27 macro estimates – real GDP growth at 6.3%, headline CPI inflation at 5.1%, and CAD/GDP at 2.3%. Notably, the macro impact will depend on how the crude price shock (and reversal) is shared between the government, OMCs, and consumers – with a possible partial reversal of the retail fuel price hikes in 4Q as crude oil prices fall below USD75/bbl. Additionally, while the current account will see pressure from higher oil prices (vs FY26), the GoI and RBI measures to attract capital flows should help address the BoP deficit. With USD70-75bn in capital flows expected after these measures, FY27E BoP could move to near-zero deficit or even a minor surplus. This should help INR appreciate toward 93 in the near term (by end-2QFY27), as these flows materialize. However, a heavy net short forward book (USD95bn, with USD45bn maturing by end-FY27) may put depreciation pressure on the currency beyond 2QFY27. Potential inclusion of Indian sovereign bonds in global bond indices could bring in further large passive FPI debt inflows of USD20-25bn; however, these are likely to materialize only in FY28

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354