Digital NBFCs’ Personal Loan Book Set to Cross Rs 3.6 Lakh Cr by FY30 by Nepal by CareEdge Ratings

Synopsis

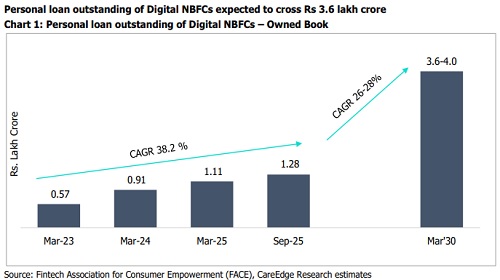

* The personal loan portfolio of digital NBFCs is expected to exceed Rs 3.6 lakh crore by FY30, translating into a CAGR of 26%–28% during FY25–FY30. Growth prospects appear strong, underpinned by increasing digital penetration, expanding borrower segments.

* As per Fintech Association for Consumer Empowerment (FACE) data, as of Sep-25, the outstanding personal loan portfolio of digital NBFCs reached Rs. 1.3 lakh crore compared to Rs. 0.6 lakh crores as of Mar-23, reflecting a twofold over 2.5 years.

* Digital NBFCs witnessed a modest uptick in average ticket size from Rs. 12,967 in FY23 to Rs 15,177 in H1FY26.

* Asset Quality of digital NBFCs is improving, with GNPAs declining from 3.3% in FY23 to 2.1% in H1FY26, led by recoveries, write-offs and stringent underwriting of loans.

* Profitability of major digital NBFCs continues to remain range bound, with return on assets (ROA) ranging between 1%-4%, thereby highlighting the high-risk, high-yield nature of small-ticket, unsecured loan portfolios and efficient digital distribution models. Digital NBFCs have strong capital adequacy, backed by continued funding support from institutional and venture investors.

Digital Lending: Fastest-growing financial ecosystems globally

The rise of digital lenders has expanded access to credit, particularly for under-served segments such as MSMEs, non-salaried individuals including freelancers and new-to-credit customers. Digital lenders, leveraging the India stack comprising of smartphones, Aadhaar-enabled e-KYC, and UPI, are able to offer instant, paperless loans, overcoming traditional barriers to collateral and complex approvals.

Co-lending partnerships between banks and digital NBFCs have further strengthened credit reach and facilitated risk-sharing. Digital lending continues to offer clear advantages in accessibility, speed, customer convenience and driving financial inclusion. However, emerging risks warrant attention data privacy concerns under the Digital Personal Data Protection Act (2025), rising cyber threats and aggressive lending practices have prompted tighter regulatory oversight. RBI’s Digital Lending Directions now mandate explicit consent, Key Fact Statements and prohibit automatic credit limit enhancements to safeguard borrowers. Additionally, while the asset quality has improved risks persist in high-growth unsecured portfolios with retail NPAs increasingly concentrated in personal loans. Balancing innovation with prudent risk management and compliance will be critical for digital NBFCs to sustain growth and credibility in India’s financial ecosystem.

In volume terms, Digital NBFCs increased their share in the personal loan portfolio, indicating a strong growth momentum. Other NBFCs also witnessed a notable uptick in share of personal loan volumes, reflecting growing penetration of NBFCs in the personal loan space.

Digital NBFCs remain volume-heavy, serving riskier customer segments; however, they face higher credit costs and regulatory scrutiny, while traditional NBFCs maintain steadier growth through larger-ticket lending and diversified books. In value terms, banks continue to account for the highest share of the personal loan portfolio, supported by their focus on prime customers and higher ticket sizes. However, their share has been gradually declining, indicating increasing competitive intensity. Other NBFCs follow, with a stable to moderately rising share driven by expansion in mid-ticket segments and diversified lending strategies. Digital NBFCs, although still relatively smaller in value terms compared to banks and traditional NBFCs, have witnessed a steady increase in share, reflecting their growing ability to scale beyond small-ticket, high-volume lending and gradually move up the value chain.

Asset quality of digital NBFCs has shown marked improvement post-pandemic, with GNPA declining from 3.3% in FY23 to 2.7% in FY25, and further to 2.1% by September 2025. This sequential improvement reflects a combination of factors: aggressive recoveries and technical write-offs of delinquent accounts, tighter underwriting standards and enhanced credit monitoring frameworks introduced under RBI’s scale-based regulations. Additionally, colending arrangements with banks have helped distribute risk and stabilize portfolio quality. While these measures have strengthened resilience, GNPA levels remain higher than those of banks underscoring the inherent vulnerability of small-ticket and unsecured lending to credit shocks.

Furthermore, in terms of profitability, based on an analysis of major digital NBFCs, net interest margin is 8%-12%, while ROA is 1%-4% and the balance is mostly credit cost. This highlights the high-risk, high-yield nature of their small-ticket, unsecured loan portfolios and efficient digital distribution models. Digital NBFCs write off their NPAs periodically, leading to high credit cost. However, digital NBFCs have strong capital adequacy, backed by patient capital from institutional investors.

Digital NBFCs' average ticket size reached Rs.15,177 in H1FY26, indicating ease of access to credit for tech-savvy youth, freelancing individuals, and new-to-credit borrowers. At the same time, the average ticket size of Banks and other NBFCs remained high, indicating a focus on high-value loans and moderate-to-low-risk borrowers.

Urban markets remain the primary focus for digital and other NBFCs, accounting for a significant share of loan sanctions in H1FY26. This significant concentration of NBFCs reflects the higher demand from the tech-savvy, credit-aware population in urban centres, supported by higher income visibility, formal employment structures, and deeper penetration of digital infrastructure enabling seamless onboarding and faster credit disbursal.

From a financial literacy perspective, this trend also highlights the relatively higher awareness and acceptance of formal credit products among urban borrowers, particularly in understanding product features, repayment obligations, and digital interfaces. However, it underscores the need to further deepen financial literacy initiatives in semi-urban and rural markets to enable responsible credit adoption.

As indicated by the above chart, personal loans across all lenders are concentrated mainly among the 26-35 age group, suggesting that young individuals and new job entrants remain the primary target customers. In H1FY26, digital NBFCs sanctioned nearly half of their total sanctioned value to the tech-savvy 26-35 age group, reflecting their strong positioning in catering to digitally active, salaried borrowers with higher consumption-driven credit needs and faster adoption of app-based lending platforms. This trend also underscores the need for enhanced financial literacy among younger borrowers to promote responsible credit usage and repayment discipline.

The 36-45 age group holds the second-largest share at 28%, ahead of Other NBFCs and banks, suggesting continued credit demand from more established borrowers with relatively stable income profiles. While this agewise skew supports growth visibility and cross-sell opportunities for lenders, it also necessitates prudent risk management given the higher sensitivity of younger borrowers to income volatility.

Above views are of the author and not of the website kindly read disclaimer

More News

PLI scheme for textiles : Centre extends last date for new applicants till December 31