Cross Sector Analysis - Artificial Intelligence Theme Report - Driver of localized power demand by PL Capital

Installed Data Center capacity is projected to scale from ~1.3GW in FY25 to ~4.5GW by FY30, implying an addition of ~3.1–3.2GW over the next five years. Assuming a PUE of ~1.4x and ~70% utilization, data centre power consumption could rise to ~4.4GW by FY30 from 1.3GW in FY25, accounting for ~4% of India’s incremental peak power over FY25–30. The share of DC in power demand is expected to stay at 1.6% by FY30E (upside possible if country adds more capacity). DC build-out remains highly concentrated, with Mumbai/Navi Mumbai and Chennai together accounting for ~60% of existing capacity, and Mumbai emerging as the single largest power-load hub due to hyperscale clustering and submarine cable connectivity. Reflecting this concentration, data centers could account for ~28% of Mumbai’s peak demand by FY30, significantly higher than other key hubs, underscoring a distinctly localized grid impact. Mumbai/MMR-focused utilities such as Adani Energy Solutions, Tata Power could benefit from rising hyperscale data-centre power demand and associated grid capex

Power intensity driven by DC type:

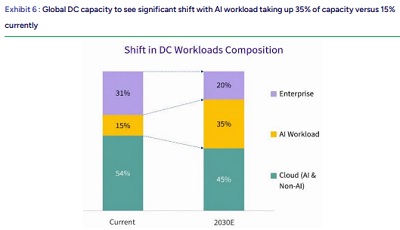

Power consumption varies significantly by data centre (DC) type and utilization, with efficiency largely driven by PUE (Power Usage Effectiveness). Hyperscale and colocation facilities, while more efficient (lower PUEs), consume substantially higher absolute power due to higher utilization levels. IT load (Server, Storage, network) accounts for ~40–50% of electricity use, while cooling (Computer Room Air Conditioners, chillers) contribute ~30–40%.

Concentrated load base with emerging secondary hub:

India’s DC capacity remains heavily concentrated in Mumbai/Navi Mumbai and Chennai, which together account for ~60% of installed capacity. However, Hyderabad, Bengaluru, Pune, and NCR are rapidly emerging as new centres, supported by better infrastructure, land availability. By FY30E, DCs could represent ~28% of Mumbai’s peak demand, compared to ~11% in Chennai and ~5-10% in other hubs, highlighting localized power requirement.

AI demand triggers US utilities re-rating:

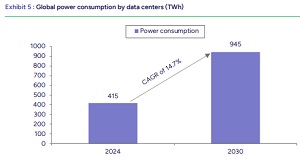

The US utilities sector has seen a re-rating driven by AI-led data centers, electrification and grid upgrades, which are reviving electricity demand after years of stagnation. Since 2024, the S&P 500 Utilities Index has outperformed the broader S&P 500 as markets price in stronger long-term demand visibility. With data centers expected to account for ~12% of US power demand by 2030 (vs ~4.3% in 2024), utilities are increasingly being viewed as structural growth assets rather than defensive yield plays, a trend that could become relevant for India as DC share in power demand rises.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

More News

Consumer Sector Update : Q4FY26 Quarterly Results Review by Choice Institutional Equities Ltd