Consumer Sector Update: Positive trends at last, but FY27 outlook uncertain By Motilal Oswal Financial Services Ltd

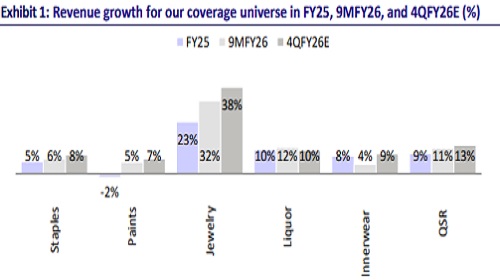

Within our consumer coverage universe, almost all segments are likely to see an increase in revenue/EBITDA growth YoY in 4QFY26: staples +8% each, paints & adhesives +7%/ +14%, liquor +10%/+23%, innerwear +9%/+5%, QSR +13%/+8%, and jewelry +38%/+47%. Demand recovery was visible across categories, and in most of the months in 4Q, we found a trend after a long time. A few categories/companies may see a slight advantage in trade pre-buying at the end of Mar’26 in anticipation of pricing actions in Apr’26.

Staples companies are expected to report improvement in revenue growth YoY for the domestic market. The ongoing geopolitical tension has impacted most staple companies on the international business front (with more impact in the Middle East). Companies such as Dabur and Emami will be more affected at the consolidated level due to issues in the MENA region (6-8% revenue salience). On the India front, abrupt rains in select geographies will weigh on summer-centric products such as talcum powders, beverages, energy drinks, etc. We expect the food category to continue outperforming BPC. Rural demand is expected to remain resilient, while urban demand has also shown an improving trajectory. Most companies took marginal price hikes in March (~2%) and expect more pricing in April to adjust for steep RM inflation. For 4QFY26, margins are expected to remain healthy amidst stable commodity prices, with trends reversing a bit in 1QFY27. We expect Britannia, Nestle, GCPL, Marico, LT Foods, Tata Consumer, and Zydus Wellness to deliver double-digit YoY EBITDA growth. We expect our coverage universe to deliver a sales/ EBITDA/APAT growth of 8%/8%/6% in 4Q.

Paint & Adhesives: Demand has improved steadily over the last five months following a weak demand in Oct’25. Industry demand in value terms is expected to be in the mid to high single digits in 4Q. Given the RM and FG inventory, the recent cost inflation is not likely to impact 4QFY26 performance. That said, most paint companies have announced price hikes in the range of 5-8%, which will be largely effective from Apr. We expect a high-single-to-low-double digit volume growth in 4Q, aided by steady demand and partial benefits of inventory filling ahead of the price hikes. Gross margins are expected to improve, aided by benign raw material prices for most of 4Q, which should also aid EBITDA margin expansion. Pidilite is likely to sustain double-digit growth, aided by margin tailwinds and resilient underlying demand. We model sales/EBITDA/ PAT growth of 7%/ 14%/27% for our coverage universe in 4Q (vs -1%/-8%/-19% in 4QFY25).

Liquor companies are expected to report a mixed performance in 4QFY26. Last year’s heavy base of AP and the full impact of Maharashtra Made Liquor (MML) are anticipated to moderate headline numbers. The recent taxation reforms in Karnataka are a key positive for the industry; however, policy details are still awaited. Ongoing geopolitical tensions have not had much impact on operations. While glass costs (~1/3rd of RM) are expected to see inflation. UNSP is likely to see ~3% volume decline but ~8% revenue growth, impacted by the Maharashtra excise hike and a high base in Andhra Pradesh. The Maharashtra disruption was more severe in 4Q due to full-quarter MML (vs. 45 days in 3Q). In contrast, Radico is expected to post strong double-digit, volume-led growth. The weak summer season and adverse state mix are expected to have affected beer demand for UBBL. We expect sales/EBITDA/PAT growth of 10%/23%/23% for our coverage companies in 4QFY26.

The innerwear sector is witnessing a sequential uptick in demand after a prolonged slowdown in the GT channel, while e-commerce continues to grow well. 4Q is a seasonally strong quarter for the innerwear sector, contributing 35-40% of annual sales. Moreover, we expect Eid in Mar’26 to have added to the 4Q performance. We continue to monitor any pricing action in the space after a zero price hike in the last few years. Trade pre-buying benefits may be visible in 4Q as well. PAGE continues to focus on premiumization by launching new products and investing in marketing and technology. We expect a sales/EBITDA/PAT growth of 9%/5%/1% for the company.

QSR companies in 4QFY26 have shown early signs of sequential improvement, with January witnessing relatively better traction. Early Navratri (last year in Apr) and Ramadan had a partial impact on demand. Still, most companies have seen better SSSG trends than 3Q. The ongoing US-Iran conflict is creating operational challenges, primarily through disruptions in LPG availability and logistics. A large proportion of stores remain dependent on commercial LPG cylinders (Domino’s >70%, KFC/Pizza Hut >60%), making them vulnerable to supply-side constraints. While some players (e.g., McDonald’s) have low dependence (20-25% stores). However, companies have been able to navigate the situation, and most stores across brands were operational during March. Companies have taken multiple initiatives (elective ovens, induction cooking, menu alteration, etc.); however, any supply shortage can still disrupt operations going ahead. Gross margins are expected to remain healthy, while some companies (McD, KFC) have taken value offering/discounting cards during the last six months, which can have an impact on the margin trend. Thus, restaurant margins (ROM) may showcase a divergent trend among brands. We expect sales and EBITDA growth of 13% and 8% for 4QFY26, respectively.

Jewelry: In 4QFY26, gold prices surged, rising ~80% YoY and ~20% QoQ. Despite this steep inflation, consumer demand for top brands remained resilient, supported by a strong festive season and sustained momentum during the wedding period. Demand was further aided by higher old gold exchange-led purchases and attractive promotional offers. Gold coin sales continued to remain elevated amid rising gold prices. SSSG is expected to grow in high double digits, largely driven by value growth. However, margins may witness YoY pressure due to elevated gold prices; studded mix can see improvement due to stable diamond prices. We model a sales/EBITDA/PAT growth of 38%/47%/65% for our coverage jewelry companies in 4QFY26.

Outperformers and underperformers: Among our coverage companies, Titan, Radico, Marico, Britannia, Nestle, and Kalyan Jewelers are expected to be outliers in 4QFY26, whereas Colgate, HUL, Emami, Dabur, and UBBL will likely be the underperformers.

Outlook: 4QFY26 began on an optimistic note across consumption categories, with Jan-Feb witnessing sequential improvement from 3Q. The growth was backed by improving macros, festivities, and stable RM prices. Thus, 4Q is likely to have minimal impact of geopolitical tensions on revenue and margins. Going forward, we expect the inflationary pressure to increase, and this may result in lower spending. We remain watchful of the current RM price volatility, and the levels they set will be a key monitorable. The companies with higher exposure to international markets (MENA) will be more affected than others. Overall, near-term demand growth and margins are likely to remain muted. We cut our estimates as we build inflationary pressure to sustain at least in 1HFY27. Our top picks are Titan, Radico, Zydus Wellness, Britannia, and Marico.

Raw material prices remain stable in 4Q; 1QFY27 to bear the brunt

Commodity prices remained stable for most of the quarter on a YoY basis. We expect a YoY recovery in margins for most consumer companies. Most agricultural commodities and prices of non-agricultural commodities, including wheat, cocoa, maize, TiO2, and VAM, have seen moderation. However, select commodities such as copra and gold continued to see YoY inflationary pressure, while copra has seen a sharp decline from its peak (~35%).

The RM pricing scenario has completely changed since Mar’26 onwards amidst the ongoing geopolitical pressures. Steep crude inflation and INR depreciation will raise RM/PM costs for most staple companies; the effect will be more prominent in 1QFY27. Currently, it is difficult to gauge where the commodity prices will head. We continue to closely monitor key RM prices such as crude and its derivatives, palm oil, etc.

Agricultural commodities: Wheat prices dipped 13% YoY and 3% QoQ. Barley prices declined 6% YoY and 2% QoQ. Maize dipped 23% YoY (-33% QoQ). Cocoa prices declined 60% YoY and 34% QoQ, offering relief to companies like Nestlé and HUL. Coffee prices remained flat YoY, while tea prices were up 3% YoY. Copra prices surged 70% YoY while declining 2% QoQ (down ~35% from the peak levels). Palm oil prices were up 2% YoY and 4% QoQ.

Non-agricultural commodities remain a mixed bag, with a few experiencing moderation in prices, while the rest remain inflationary. Crude oil prices rose 7% YoY and 27% QoQ (at USD126/barrel). Other commodities such as TiO2 and TiO2 (China) continue to show a downward trend. VAM (China) prices rose 6% YoY and 7% QoQ. Gold prices jumped 80% YoY and 20% QoQ, putting pressure on the margins of jewelry companies.

Companies remain focused on maintaining a strategic balance between revenue growth and margin expansion amid evolving market dynamics. We expect no significant adverse impact on 4QFY26 margins; however, 1QFY27 margins may take a hit. Most staple companies have taken a marginal price hike in March and are planning calibrated price hikes in the coming months. This approach aims to navigate cost pressures effectively while maintaining competitive positioning.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

More News

Capital Goods Sector Update : Profitability remains resilient despite softer execution growt...