Capital Market Monthly: Mixed performance across market activities By Motilal Oswal Financial Services Ltd

MAAUM crosses the INR80t mark, while SIP flows remain largely flattish MoM

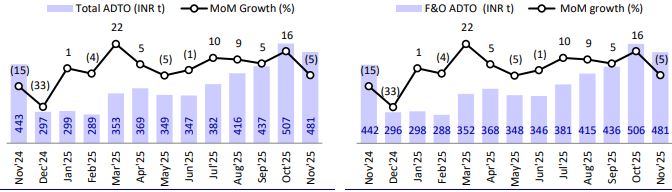

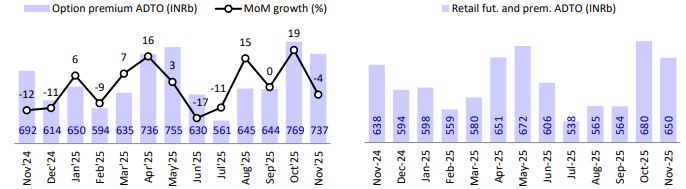

* In Nov’25, total ADTO declined 5% MoM to INR481t, led by a 5% MoM decrease in options notional ADTO. The options premium ADTO declined 4% MoM, while the cash segment ADTO rose 6% MoM.

* Retail participation witnessed a decline in activities across segments, with retail cash ADTO declining 2% MoM to INR399b, while the retail futures and options premium ADTO declined 4% MoM to INR650b.

* The commodity market volumes declined 2% MoM in Nov’25 to INR149.1t from peaks, led by a 31% MoM decline in futures, while options volumes grew 2% MoM. The premium-to-notional turnover ratio declined MoM to 0.96% from ~1.1% in Oct’24.

* Demat additions declined MoM to 2.7m in Nov’25 (3m in Oct’25). IPO activity continued to gain momentum, with 12 IPO offerings raising INR330b in Nov’25.

* MF MAAUM rose 2% MoM in Nov’25 (new highs) to INR81.3t (up 20% YoY), with equity AUM at INR35.4t (up 2% MoM). SIP flows remained flattish MoM to INR294b (INR295b in Oct’25).

* The industry posted an MoM decline in total ADTO, broadly led by a 5% decline in options notional ADTO. MF AAUM also rose sequentially, supported by growth in Equity AAUM. Volumes in the commodities segment declined 2% MoM post scaling to new highs amid rising prices of precious metals. We expect that a stable growth trajectory for volumes and rising retail participation should support the performance of market intermediaries. Stable MF flows and SIP trajectory will bode well for AMCs.

Equity: Cash activity rises, while F&O activity declines MoM

* Total ADTO declined 5% MoM in Nov’25 to INR481t, led by a 5% MoM decline in options notional ADTO.

* Option premium ADTO declined 4% MoM to INR737b, while Cash ADTO rose 6% MoM to INR1.1t in Nov’25.

* Retail futures and premium ADTO witnessed a decline of 4% MoM in Nov’25, with retail cash ADTO declining 2% MoM.

* In the cash segment, NSE maintains its leadership position, with a market share of 93% in Nov’25.

* In the F&O segment, BSE’s notional turnover market share remained stable MoM at 43.5% in Nov’25, (vs 43.8% in Oct’25), while the premium turnover market share declined MoM to 25.9% (from 26.7% in Oct’25).

Commodities: Volumes decline MoM from a higher base

* Total volumes on MCX declined 2% MoM to INR149.1t in Nov’25 (~2.8x YoY), with ADTO crossing the INR7t mark (INR7.5t in Nov’25 vs INR6.9t in Oct’25).

* Option volumes rose 2% MoM to INR135.4t, while futures volumes declined 31% MoM to INR13.7t.

* Growth in options ADTO (12% MoM) was aided by 15%/7% MoM growth in Bullion/Energy segment ADTOs. While base metals ADTO witnessed a decline of 35% MoM. Option premium ADTO declined 14% MoM to INR1.3t, with premium-to-notional turnover ratio declining MoM to ~0.96% from ~1.1% in Oct’24.

* In commodity futures, ADTO declined 24% MoM, mainly due to a 30%/29% MoM decline in bullion/base metals futures ADTO, while energy segment ADTO posted a 30% MoM growth.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)

More News

Daily Market Insight - 7th July 2026 by Motilal Oswal Wealth Mangement Ltd