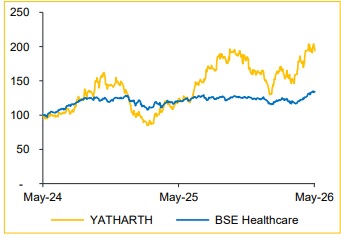

Buy Yatharth Hospitals Ltd for the Target Rs.1,050 by Choice Institutional Equities

NCR-focused expansion enhancing long-term value:

YATHARTH’s focused expansion across Delhi-NCR micro-markets and strong super-specialty portfolio are expected to drive sustained ARPOB growth and margin improvement. Growth will likely be supported by ~8% annual ARPOB growth, improving occupancy, strategic acquisitions, better payer mix, and reduction in government business share from 35% to ~25%, supporting 30%+ revenue growth over the medium term.

View and valuation: We project Revenue/EBITDA/PAT to expand at a CAGR of 32.1%/33.2%/40.3% over FY26–FY29E. Maintaining our valuation multiple to 20x EV/EBITDA on FY28E, we maintain our target price to INR 1,050 and maintain our BUY rating.

Significant growth across all fronts on YoY basis

* Revenue grew significantly by 46.6% YoY and 6.3% QoQ at INR 3,416 Mn (vs CIE estimate of INR 3,316 Mn).

* ARPOB grew 5.3% YoY to INR 33,283, with occupancy at 71%.

* EBITDA grew 37.1% YoY and 6.4% QoQ at INR 799 Mn, with margin contracting 161 bps YoY and flat on QoQ at 23.4% (vs CIE estimate of 24.0%) ? PAT grew 22.7% YoY and 4.8% QoQ to INR 475 Mn (vs CIE of INR 481 Mn).

NCR cluster expansion accelerating premium growth: Yatharth is rapidly building a dominant NCR healthcare franchise through a cluster-led expansion strategy, combining aggressive bed additions with rising premiumization. The company has already scaled to 2,550 beds and expects to surpass its 5,000-bed target by the next 3 years, with ~70% occupancy. Simultaneously, higher-end specialties, medical tourism and better payer mix are driving ARPOB expansion. YATHARTH is well positioned to sustain high-growth expansion while improving margins and realization metrics.

New hospitals scaling faster than expected: The biggest positive surprise in FY26 has been the exceptionally fast ramp-up of newly commissioned hospitals, significantly reducing gestation risk. The Delhi and Faridabad Sector20 hospitals together contributed ~11% of Q4FY26 revenues and are operating with healthy payer mix dominated by cash and TPA patients. Faridabad Sector-20 is expected to achieve EBITDA breakeven within just 10–11 months, while Delhi Model Town is expected to break even within 14–15 months, materially faster than industry averages for greenfield hospital assets.

Medical tourism opportunity becoming structural growth driver: YATHARTH is emerging as a serious medical value travel player in North India, supported by airport connectivity, premium specialties and rising international patient inflows. International patient contribution has already increased meaningfully at Greater Noida and Noida Extension hospitals, helping ARPOB outperform expectations. The upcoming Gurugram facility, strategically located near IGI Airport, is expected to be heavily driven by international patients and private insurance, supporting projected ARPOB above INR 50,000.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131