Buy Sudarshan Chemical Ltd for Target Rs 1,212 by Elara Capital

Heubach improvement starts reflecting

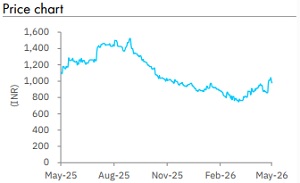

Sudarshan Chemical ’s (SCHI IN) stock price has outperformed in the past three months, rising 12% versus an 8% rise in NSE Small -cap, given that confidence has improved with recovery in the acquired Heubach business, reduction in inventory, drop in net debt and better -than -guided business EBITDA in Q4. The Q4 call also helped rebuild confidence that the Heubach issue was more of a destocking/integration -led rather than a persistent demand loss. We raise our TP to INR 1,212 from INR 1,047 and upgrade SCHI to Buy from Accumulate .

Q4 beat led by recovery in acquired business:

SCHI delivered a strong Q4FY26, with consolidated revenue up 33% QoQ and EBITDA up 500% QoQ, driven by volume -led recovery in the acquired business, lower -than -expected operating cost growth and value -capture benefits. Management highlighted that Q4 recovery was led by customers buying again after destocking. The acquired group delivered EUR 11mn EBITDA in Q4 versus earlier guidance of EUR 9 – 10mn, while inventory reduction was EUR 29mn against the earlier plan of EUR 20mn. Net debt reduced meaningfully from INR 9 .34bn in Dec ’25 to INR 7 .55bn in Mar ’26.

Heubach recovery – Volume-led, and not price-led:

The key positive was turnaround signs at the acquired -group . The management clarified that Q4 improvement was largely volume - led, with no major price increase in Q4 . The recovery was broad -based across regions and end -use segments, with coatings being the key driver for the acquired business. Q3 weakness was driven by destocking, weak demand and high fixed -cost deleverage, while Q4 showed that operating leverage can return quickly when volumes normalize.

FY27 guidance achievable, though we assume gradual ramp-up:

Management expects the acquired group to deliver ~EUR 35mn EBITDA in FY27 and is confident of achieving EUR 90 – 100mn EBITDA in the next 3 -4 years, led by synergies, value -capture initiatives and sales growth. Integration benefits are not fully captured yet and should flow in the next two financial years. We assume a gradual ramp -up , given current geopolitical/RM/logistics volatility. Management highlighted crude -derived RM inflation, energy cost in crease, logistics lead -time pressure and near -term customer caution.

Legacy business steady:

Legacy Sudarshan remained resilient, with Q4 EBITDA margin above 14%. Management expects legacy business to grow 8 -10% in FY27, barring geopolitical disruption, supported by distributor normalization and recovery in key end markets. It also expects to maintain healthy margin by passing cost increases to customers.

Estimates upgraded; TP raised to INR 1,212; upgrade to Buy:

We raise our estimates after improved visibility on Heubach recovery. We raise FY27E/28E revenue 6%/7% and FY28E EPS by 12.3%. We introduce FY29E estimates. We raise our TP to INR 1,212 from INR 1,047 and upgrade SCHI to Buy from Accumulate, driven by better confidence in Heubach turnaround, faster working -capital release, improving balance sheet and rising pro bability of delivery on medium -term EBITDA ambition. Our TP is based on DCF, assuming a 4 % terminal growth rate (unchanged), a 10.9% cost of capital (unchanged) and 28% FY26 -29E EBITDA CAGR (from 21%).

Please refer disclaimer at Report

SEBI Registration number is INH000000933